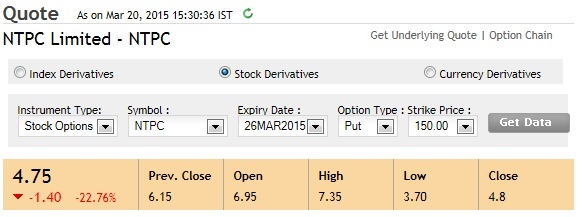

Previous Day Close: 154:75 and Tody Close: 145:50 (-5.98% Down)

On other hand, Puts closed down.

I noticed this even for NIFTY as well. Is there any formula in the last Friday of F&O?

Previous Day Close: 154:75 and Tody Close: 145:50 (-5.98% Down)

On other hand, Puts closed down.

I noticed this even for NIFTY as well. Is there any formula in the last Friday of F&O?

As NTPC issue debantures and there is arbitrage oppurtunity in stock 7 days back , so traders go long on cash and short futures and as you know NTPC has already issue debuntures , so arbitrage came to end last day and traders are reversing their positions , so thats why this all this happens.

This is slightly tricky but let me attempt to explain why this happened (please note, this is just my reasoning and I could be wrong) -

NTPC issued bonus debentures recently to reduce their massive cash pile (nearly 72k Crs). Once cash is paid out, the RoE (return on equity) increases, which is a very important number used in evaluating the profitability of the company. A bonus debenture is an interest bearing instrument, where the interest amount can be treated as an alternative to dividends. So if you have 100 shares of NTPC of Rs.10 each, then as per the company’s resolve you are entitled to receive 100 Bonus debentures of Rs.12.5 each…which obviously is worth Rs.1250/-. Against these debentures each year NTPC is expected to pay an interest (coupon) equivalent of the 'average yield of 10 year GOI security + 50 basis points".

So the average yield on GOI is about 8% add to that another 50bps which is 0.5% you are entitled to get 8.5% interest against the bonus debentures…which means if you have 100 bonus debentures of Rs.12.5 each…at 8.5% you will receive Rs.106.25 as interest amount or Rs.1.06 interest per share.

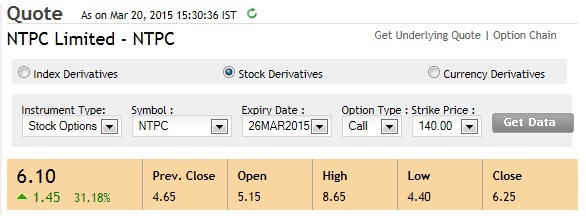

Given this Friday was the record date for the NTPC bonus debenture issue…all the traders who had bought NTPC because for the cash flow of nearly Rs.106.25 (for every 100 shares of NTPC) were now free to sell their shares (as on the books of the registrar they would be registered as shareholders on Friday considering T+2 settlement in India). This explains the fall in the stock. But why did the price of the call option increase?

You are referring to the 140 call option here – which means the minimum intrinsic value of the 140 call option when the spot is at 145.5 is Rs.5.5. Add to it the Rs.1.06 cash flow per share (which is expected this month) the minimum value of the option should be around Rs.6.5/- (please note I’m guessing the GOI yield as 8%…you can plug in the exact value to get more accurate results here. But It should be in the vicinity of 8%). So as far I understand this, there was no way this option could trade lower…hence traders who knew this beforehand were willing to buy the option…hence the price shot up.

Please note, we are not talking about time value at all here!

Even I am intrigued by this. For most of the Scrips and indices yesterady, Futures were trading at discount to spot… Today, for NTPC, even though spot has fallen by 5%, but Futures rose by around 1%. And so as the options. This contradicts the belief that Option price depends on underlying Spot. Experts please advise?

And why the same happened for Nifty and Banknifty?

The definition of derivative is not aligned here. This is special case where derivatives moves towards unexpected direction. Can the experts explain this type of case in detail please?