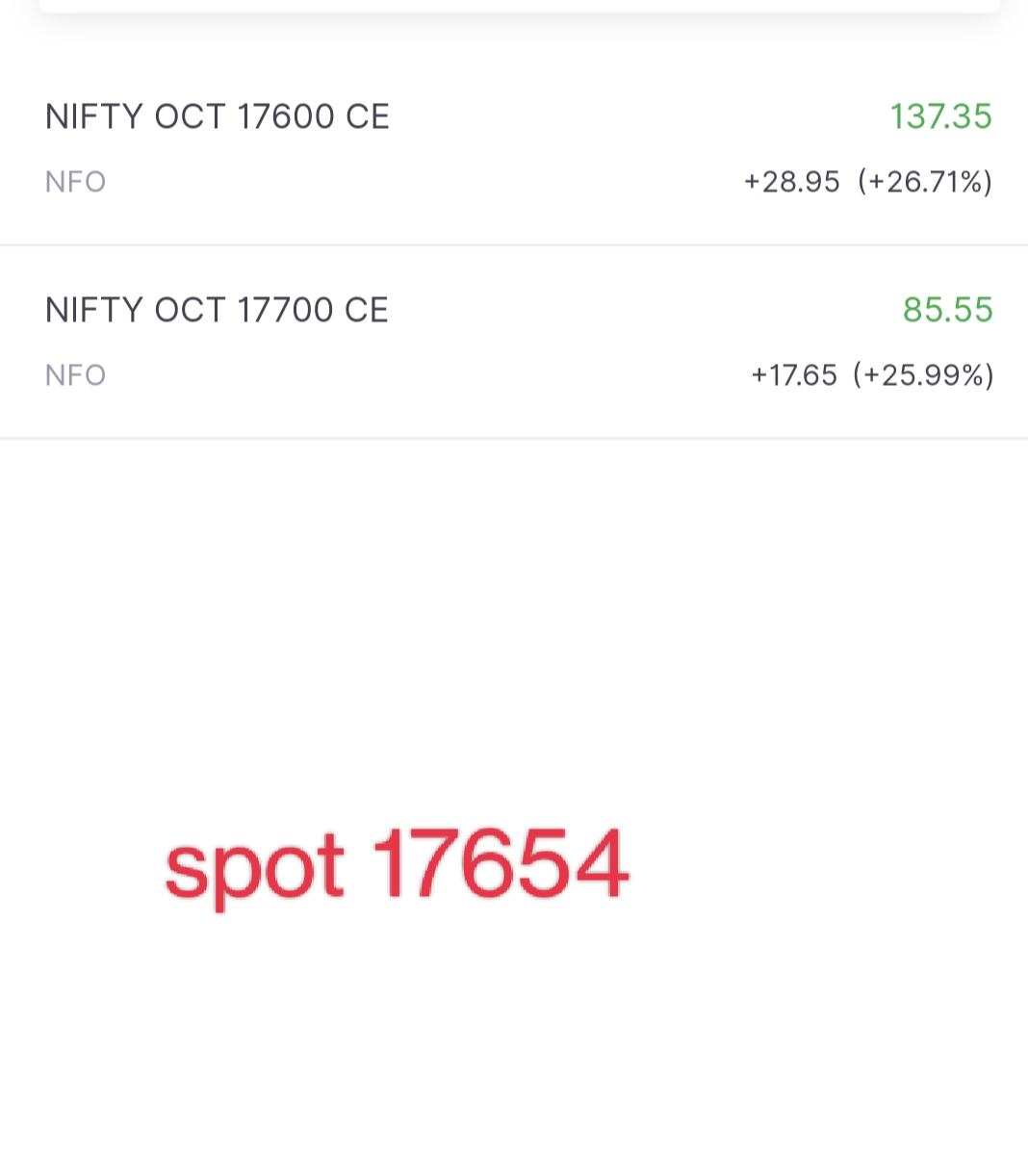

This question is when nifty is around 12:19 pm date 20 oct the spot is around 17654.

Ques - The premium calculation is dependent on delta my understanding here is the deeper the itm the greater the delta meaning movement in comparison to spit is greater on the premiums.

However here i see that 17700 is deeper itm than 17600 however percentage change is greater for 17600 how can this be possible as delta will be higher for 17700

Probably i am skipping something here please help in making it clear

If Spot is at 17654 then 17700 CE becomes OTM(Out of the Money). There are other factors as well like Theta(Time Decay) and also check for IV(Implied Volatility).

thank you for sharing

so my understanding on how the strike price moves per delta is correct right it’s just that here i am comparing the itm to otm that is why there is a difference