I’ve recently started learning options. How the expected premium is calculated for option writers?

Values

Current Underlying Price @ 100

CALL Option Premium = 5

Delta of the option = + 0.50

Assuming Underlying Price will rise to 108

CALL Option Buyer

Change in Underlying = 108-100 = +8 Points

Change in Premium = 8*(+0.5) = 4

New Premium = 5+4 = 9

CALL Option Seller

Change in Underlying = 108-100 = +8 Points

Change in Premium = 8*(-0.5) = -4

CALL Option seller Delta value taken as negative (-0.5)

New Premium = 5-4 = 1 ???

When underlying increases the CALL premium should increase but in this case it’s not

Can anyone help me with this, I’m confused

Update: As we’ve written the the option the value is negative for option writers.

New Premium = 5-(-4) = 9

Apart from Delta there are 4 other things that also affect the premium

Theta (time), Vega (volatility), Gamma (rate of change of Delta) and Roe (rate of interest)

As the option moves out of the money (OTM) the delta will start reducing

so the rate of Delta wont be 0.5 % throughout

Yet it is an interesting question

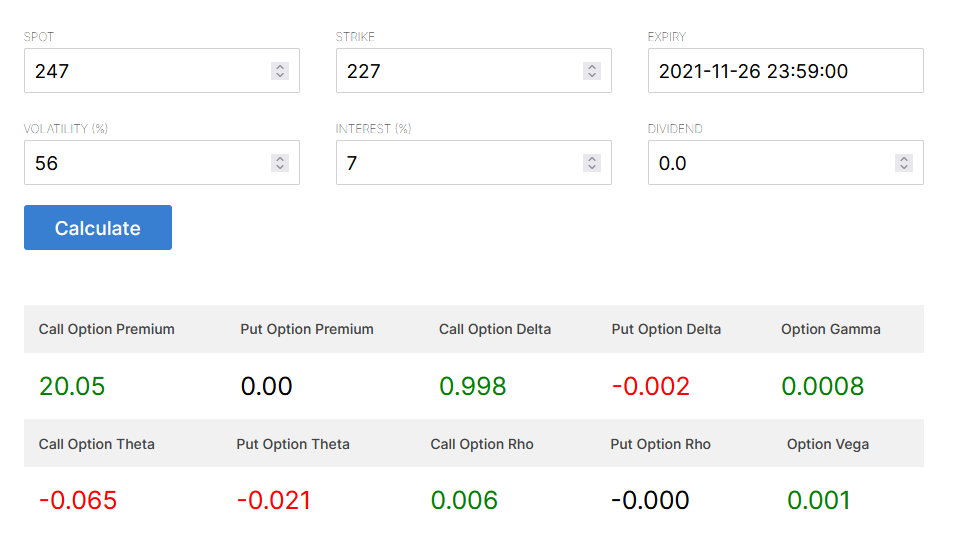

Lets take a real example - say ITC (Share value at Rs 227 at the end of the trading session on 24th Nov 2021)

And the premium value of the ATM Put Option (with Strike Price of Rs 227) is Rs 1.15

What if the value of ITC share price increases by Rs 20 in the first five minutes of trade the next day , then what happens to the value of the Put option ?

Even if Delta value falls rapidly, say it becomes 0.02 by the time ITC share price reaches 247 and the average change in Delta is 0.25, that would still mean that it would reduce the Option price by Rs 20 X 0.25 (Average Delta) - which is Rs 5 .

So the new value of the Put Option should be

Rs 1.15 - Rs 5 = (-) Rs 3.85

But we cant have Premium values in the negative

So what am I missing ?

The premium and delta remain the same for both call option buyer and seller. What changes is the algebraic sign associated with the position. It’s +ve for long and -ve for short (option writers).

In your example -

Change in underlying = 8 points

Delta = 0.5

Old premium = 5

Change in Premium = 0.5*8 = 4

New Premium = old premium + new premium

= 5+4

=9

For Option buyer, assuming the trader is long, say 1 lot (50)

= +50 * 4

=200 is the notional profit

For option seller, assuming the trader is short, say 1 lot (50)