Tu rehne de bhai, tu 85% hisaab karke straddle laga lol

Bhaiya expentancy ki apni ek alag theory hoti hai, jaise casino me hoti hai, ki house hamesha jitta hai. Jo tum janna chahte ho, wo volatility hai, zyada volatility pe market zyada move karega etc… Straddle me se volatility nikalne ke liye Put Call Parity nahi to aur kya vaproge? Waise to directly IV hi vapar sakte ho, lekin straddle ka istemaal karna hai to fir Put Call Parity ka istemaal karke Black & Scholes ko hi reverse engineer karna padega. Mujhe lagta hai tumge jaisa Fibonacci me hota hai fixed retracements waisa chahiye, lekin jaise Fibonacci me bhi 23% se lekar 78% tak ki range hoti hai, waise hi straddle me bhi range hi ho sakti hai. Fixed value agar koi bataye to bewakoof bana raha hai itna hi samajh lijiye.

P.S. I’m not getting a clear picture though, directly bhi B&S reverse engineer kar hi sakte hai shayad.

1 Like

@emrys11 @Jayadratha I think this article may help you both.

black scholes - Why is the price of an ATM straddle not the same as the “dollar move” from implied volatility? - Quantitative Finance Stack Exchange

@emrys11 Don’t hardcode it 85%, do the math yourself, it does lie within 1SD, but that still shouldn’t be taken as a fixed value since this is deviation which can be violated easily. But as you said you manage risk properly, that’s all that you need.

To tell the essence here, the reason why straddle is priced less than the 1SD is given in the article, and there’s no fixed range like 85% of the straddle, but 1SD can be used if you want. Or you can directly look at the normal distribution chart and decide what probability of success other than 1SD suits you, if that coincides with 85% of the straddle, that should be the happy “coincidence”. If the probabilities is what you’re asking, you literally have the entire normal distribution table to look at.

So to give out my final words, there’s no such thing as 85% of straddle is the expected move, the only thing that is mathematically provable is that 1 standard deviation which is 68% probability of success is the straddle price divided by 0.79788, or multiplied by 1.25332. All else is just a lie, no such thing as a fibonacci ratios exist for option premiums, and in regards with probabilities, you literally have the entire normal distribution table to look at, not just the 1 or 2 standard deviations. That’s my take on it.

1 Like

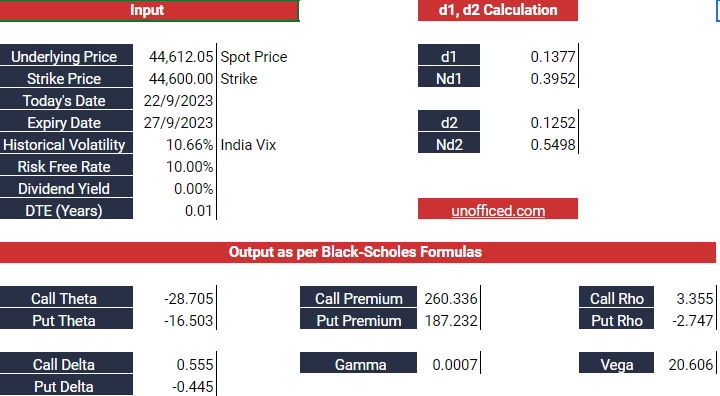

So What Exactly the ATM Options are telling with respect to Standard Deviation ?

Here is a snapshot of NIFTY Bank along with the ATM options in the next expiry -

The IV of CE and The IV of PE are also not the same. That is something that newbie noobs learn.

The IV can be seen in Options Chain which You can find in the NSE website. Or, You can use this dashboard I made.

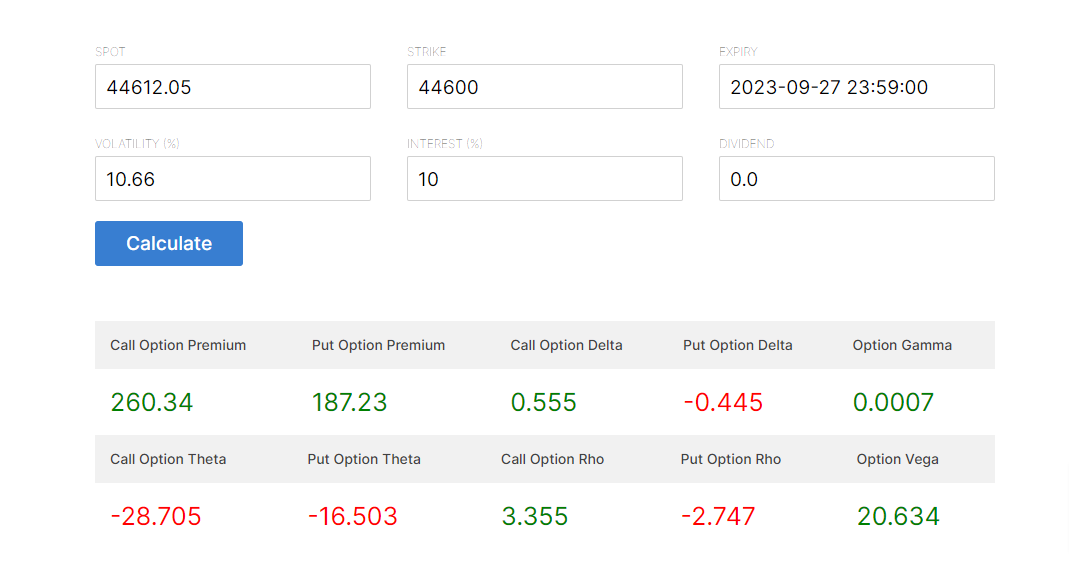

The current price of BankNIFTY is 44612.05

The current strike which is ATM is 44600

First Remember that the values or anything will not match with Sensibull. They use Black 76 Model. You can put the values in the calculator below (I literally made that bare hand).

Now, the Put IV and Call IV is different. But that difference is small.

The difference is small enough that the value is insignificant if I just use HIstorical volatility i.e. India VIX i.e NIFTY’s ATM’s IV. Now now the difference will be big if it is stock.

Anyways, The goal is, if you know the IV. (You can put the IV from the option chain if you want to be Mr.Perfectionist) -

The goal is to get the delta. (for this discussion)

Call Delta is .555

Put Delta is .445

==========

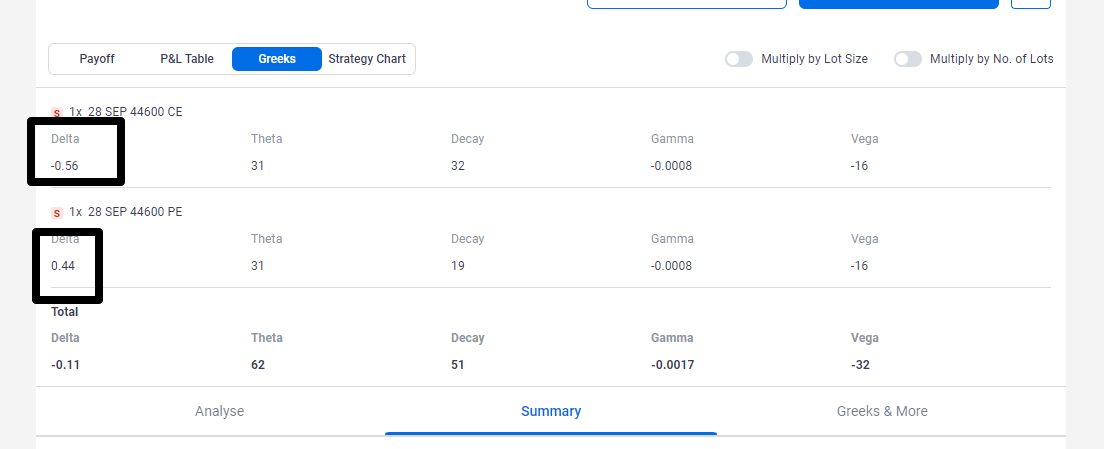

Before I type any more, Let me confuse you more beforehand so that you don’t get confused by yourself later.

Sensibull shows Put option delta as .44 and call option delta as -.56

Zerodha’s calculator matches with mine.

This is exactly why I have trust issues and create everything on my own hand after understanding things.

Sensibull will match if you follow black 76 model. read

So

How you will calculate the probability of profit in atm options.

It depends on what model you choose

And

Relation between implied volatility and standard deviation

A short straddle does not capture 1 standard deviation move!

A short strangle does! Atleast as per Black Scholes model.

Strikes with a probability of 16% ITM / 84% OTM capture a 1 standard deviation range for an OTM option.

Slight more confusion

IV of PE is 11.52%

It means BN will do ± 11.52 % before the end of the year.

read if you want - > Standard Deviation & Options - Unofficed

i write in a messy way but the mess is necessary to make things clearer.

what is the current date to expiry? there are 3 trading days left

black 76 will take 3

black scholes will take 5 after adding 2 non trading day as well

The implied volatility of a stock is synonymous with a one standard deviation range in that stock if there are 365 days to expiry because in that case, Standard Deviation

= Implied Volatility x Square Root of Time

= Implied Volatility x sqrt(365/365)

= Implied Volatility

so It means BN can do ± 11.52 % * sqrt(5/365) = 1.34831402% before the end of this expiry…

at least as per black scholes model

2 Likes

unofficed.com/courses/the-option-greeks/lessons/probability-of-profit-2/#comment-128693

Let me know if i have screwed up anywhere. (there is one error in my site which is on the std. dev article… i will fix that later. but this should be right…)

1 Like

the case become extremely and extremely amazing if you have leg based stop loss because that will make a case where the call and put can both hit sl.

so POP’s definition will change in that case.

- When two events, A and B, are independent, the Probability of both occurring is P(A and B) = P(A) * P(B).

- When two events, A and B, are independent, the Probability of one of them occurring is P(A or B) = P(A) + P(B)

Right now the calculation and metrics is based on if the “NET STRATEGY” of selling the straddle is in loss i.e. we don’t close both legs when it hits sl.

2 Likes

It’s true. But when it is not, it’s false.

If it’s not true then the following statement holds good.

A straddle price, whether weekly or 0dte, DOESN’T indicates a 68% probability(1 SD) of the instrument expiring within that range.

Sorry. This is the only way I thought I would reply. ![]()

1 Like

1 Like

Its a gentle reminder to do the hard-work and be the other 1 out of 10 individual traders…

1 Like

Thanks for the detailed reply @unofficed. I also looked at your site and it has lots of great stuff related to trading. Good work. ![]()

![]()

1 Like

LOL ![]()

Last time when I got any compliment in life… corona came. its so rare in internet. thanks mate ![]()

I found this superb blog explaining SD, MAD and Straddle.