Whether it’s an expiry day straddle or a monthly straddle, what does it indicate. As far as I know it indicates that there’s a 68% chance of the market closing within that range by expiry.

But another youtube video said that we should multiply the Straddle price by 85% and that is the expected move.

Another youtube video said that the Straddle price should be divided by 2, and that’s the expected move on any side.

So I this has me confused.

Of course I know that the market can move as much as it wants on any side at any time. But what does the Straddle price indicate in theory. Just wanted to clear the confusion. @Sensibull

ATM straddle price indicates the market’s expectation of future price volatility for the underlying asset. If the ATM straddle price is high, it suggests that traders anticipate a significant price movement in either direction, up or down. Conversely, a low ATM straddle price suggests that the market expects relatively low price volatility.

I’m asking about how much it actually indicates. If BN atm straddle is 250 on expiry day then what move does it indicate in number terms. Answer this specific question.

If I asked you what is 500-300 and you write “subtraction is done by reducing the smaller number from bigger number” how would it look? I’m looking for the specific answer which is 200 in this case.

I didn’t ask about put call parity.

I asked in very specific words what the price of a straddle indicates. And yes i know high price indicates high moves and low price indicates low moves.

To know the theory, you need to understand the intrinsic value. Basically the premium of the strike is the hedge it provides (those who already have a position in underlying). Speculators ie traders use it to make money.

Once you understand the intrinsic value, you can derive the variance of the move expected. A higher premium means the underlying is expected to deviate more from the current spot. Put call parity is the basis from which other mathematical models are developed. Its easier to start there.

If you need more information, I can redirect you to the correct author or book or article - just explain what exactly you are looking for?

In theory , ATM straddle of yearly option =VIX ; so if you see oct 2024 or Dec 2024 ATM straddle its around 12% =VIX . what it indicates is the 11% movement from CMP in an year.

How options work is its decays non linearly, follw black sholes model for calc.

Weekly ATM straddle option in theory denotes how much instument can move in one week, but its Implied Vol can be different than realised Vol.

So, make a table and note yearly, quarterly, monthly,forthnightly , weekly, daily atm straddle premium. You will understand blacksholes model.

“I’m asking about how much it actually indicates. If BN atm straddle is 250 on expiry day then what move does it indicate in number terms. Answer this specific question.”

The value of an ATM straddle represents the cost or premium paid for the straddle strategy. It doesn’t provide information about the magnitude or direction of a future market move. The straddle’s value reflects market expectations of future price volatility and serves as a measure of the market’s uncertainty.

If BN atm straddle on expiry day is 270, what expected move does it denote for the day. In exact percentage terms or point terms. Not in general terms like large value denotes large moves and small value denotes small moves.

My understanding was that 270 straddle denotes a 68% chance(1 SD) of the underlying expiring within that range.

But I saw youtube videos saying other stuff and so wanted to clarify sensibull guys or someone who has good knowledge of options theory.

Instead I got people telling about big premium indicating big moves.

It does provide expected move value in exact terms. It’s a probability and market is may exceed the expected move/volatility. But the Straddle does provide a specific value of expected probable move.

So just stop writing this. Next someone asks you for a good stock strategy you will tell them to buy low and sell high and if someone asks you 100*20, you will tell them that “multiplication of two number is always higher than both the number” instead of writing 2000.

Thats correct. 1 SD is 68% probability. But just knowing that will not help you make money - thats because the risk:reward is not linear.

Suppose you bet on each trade with a 68% probability. It means you will win ~ 7 out of 10 times. But the other 3 times you loss will have a combined draw down more than the winnings.

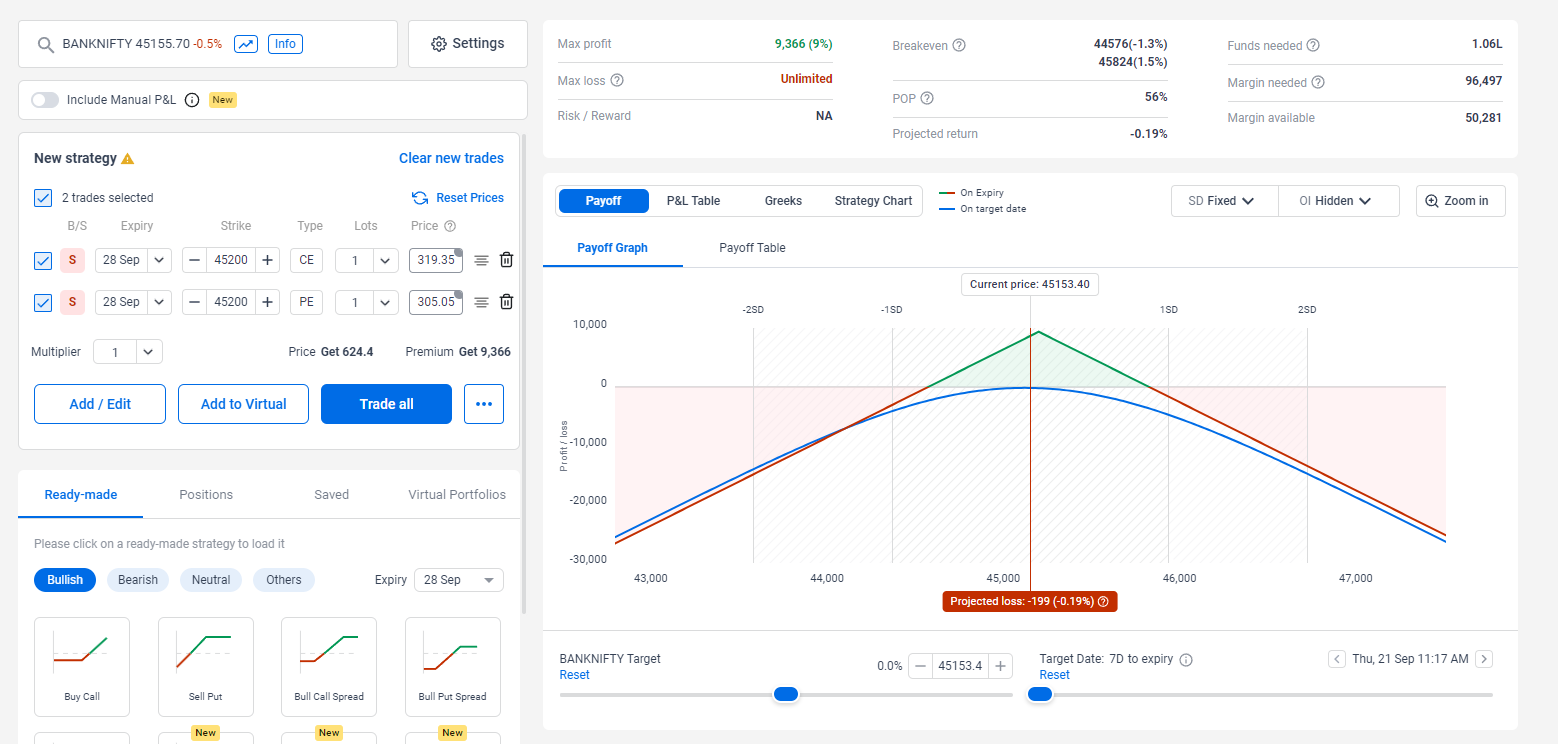

In the straddle above you make 9366 per trade (max). So you will end up making 65562 (max). But do you know how much you could lose on the other 3 trades?

If things were that easy - every one could have taken a short straddle on a Thursdays and wait out. If you are still not convinced do a back test - you will be amazed with the results.

Thanks for the detailed answer.

No I’m not planning to just sell straddle without sl lol. I have been trading since Dec 2020 and been profitable since then.

Just looking to get proper understanding of the theory part. I saw at least two youtube videos that said that 85% of the straddle price is the expected range. While i thought it was 100% of the Straddle price. So that confused me.

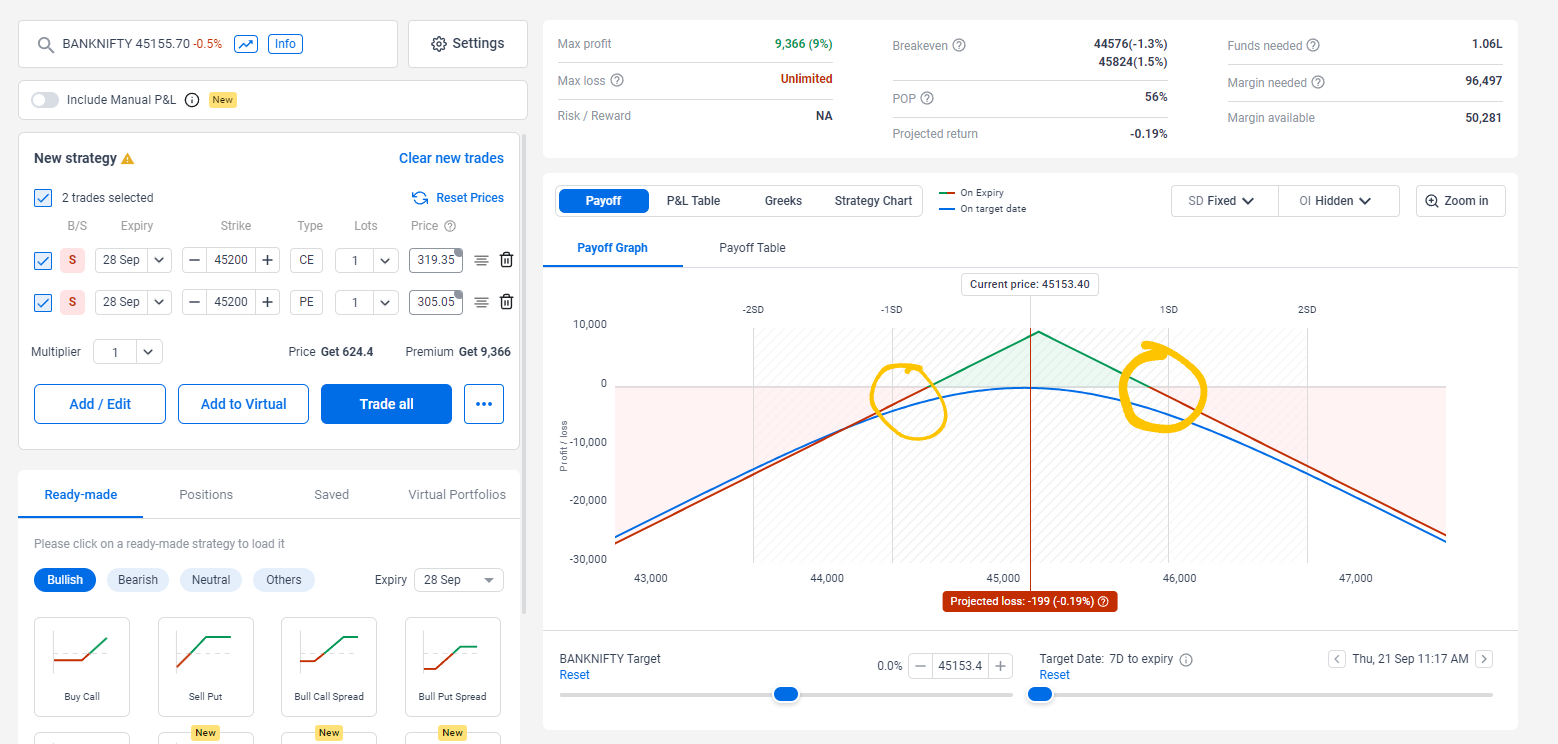

Even the image you have quoted, it shows 1sd range exceeding the Straddle range by a little bit on both sides. I went to sensibull myself and added banknifty straddle. Sure enough, there’s a little bit of range on both sides where the 1sd column is present but straddle price doesn’t extend. That leads me to think that 85% was correct. The full straddle price is not covering the full 1sd range.