It doesn’t end there, I found a vague explanation of what might be happening here. But not entirely sure, if this is how market behaviour works.

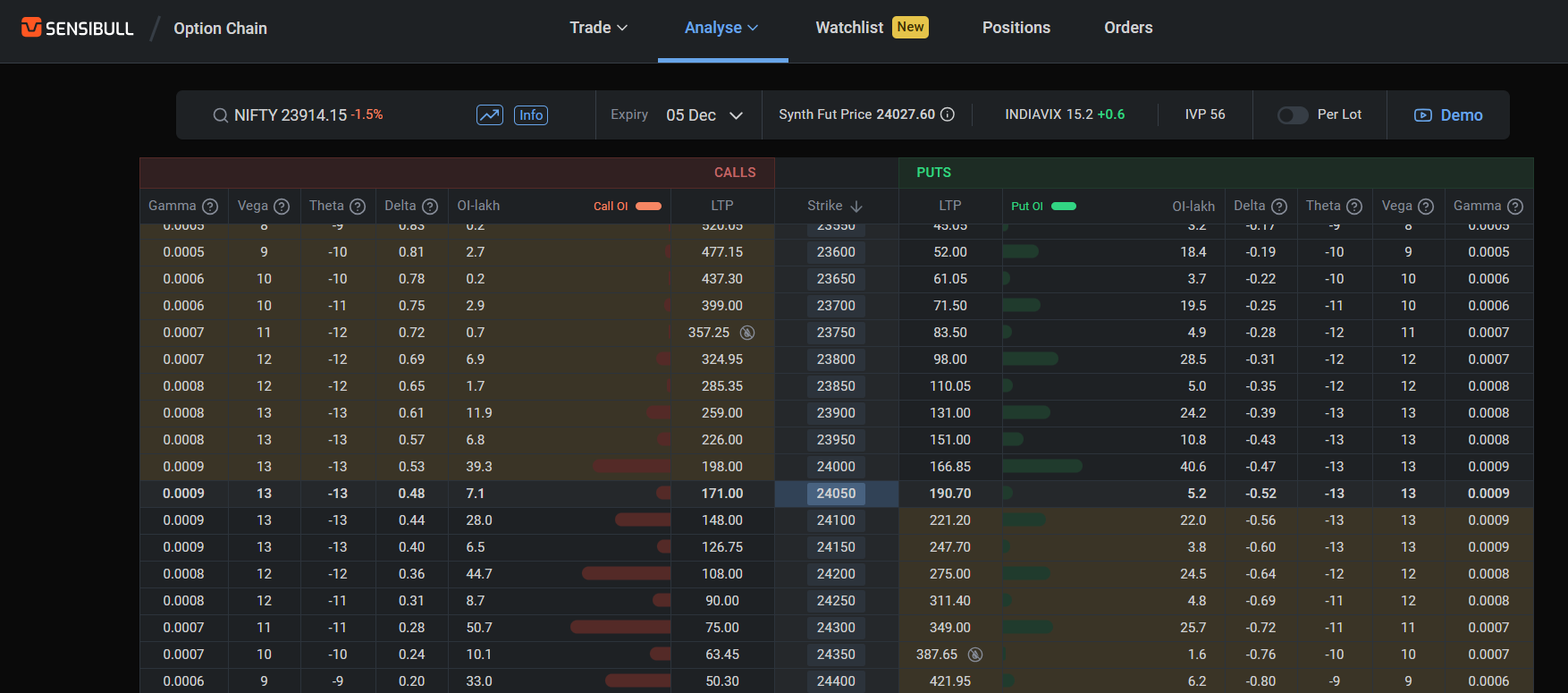

The snapshot was taken at the end of November futures expiry day (28th Nov 2024), it shows the option chain for weekly expiry (Dec 5).

On expiry day (28th Nov), the Nov futures must converge with the spot, so it also has the same value as the spot. That means Nov futures is useless for the analysis. So,

Nov Futures Actual = Nov Futures Theoretical = Spot price = 23914.5

But, the december month futures was trading around 24137, which is far higher (100+ points) than the theoretical december month futures price of 24034. So,

Dec Futures Actual = 24137

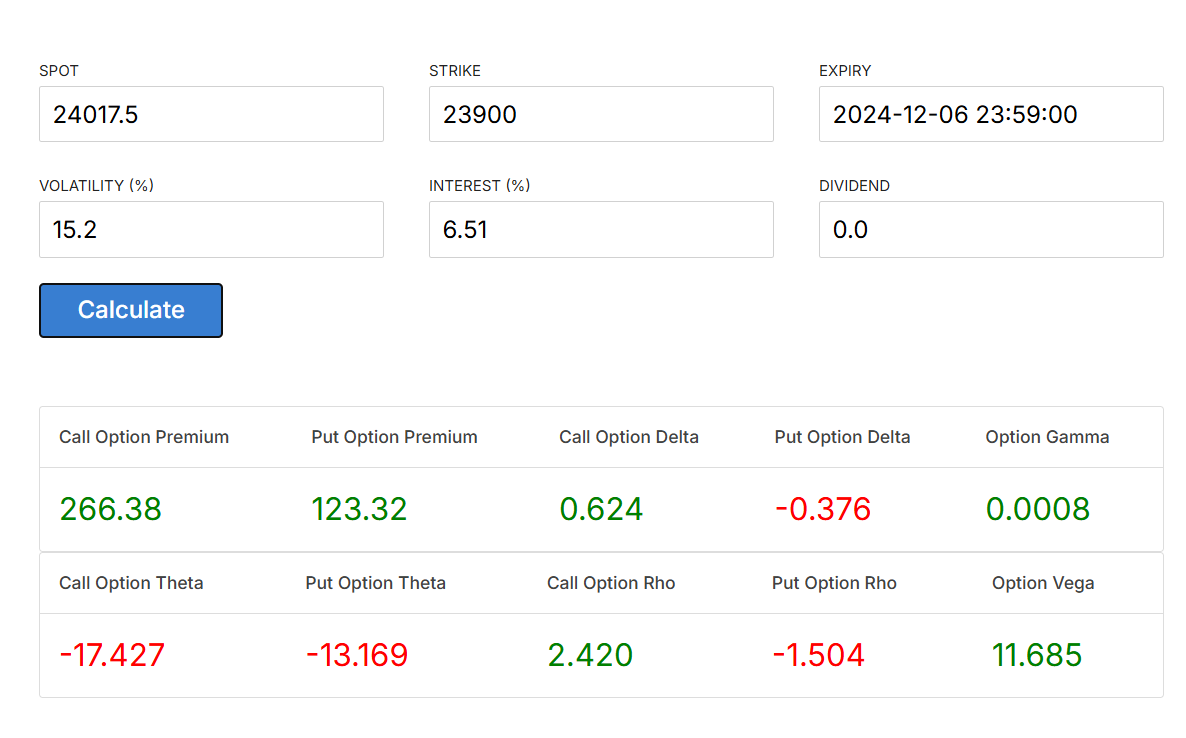

Dec Futures Theoretical = 23914.5*(1+0.06515*(28/365)) = 24034

Future-Spot spread = 24137 - 24034 = +103 points. (Concludes that market perception is 103 points higher than fair value which is quite high, and can lead to spread arbitrage as explained here)

Now coming back to options, there is no weekly futures expiry, so we need to rely on theoretical prices.

Dec 5th Futures Theoretical = 23914.5*(1+0.06515*(7/365)) = 23944

Now we know from futures price that the market is trading at 103 points above fair price, so does the ATM strike (the strike at which the current market thinks it has no intrinsic value - defintion of ATM strike) lies 103 points above the the dec 5th theoretical futures price. So,

ATM strike today = 23944 + 103 ~ 24050 (This is also the same price the actual weekly expiry futures would have traded if it existed)

But I am not entirely convinced, any critical feedback is greatly appreciated. Thanks!