Recently came across the following article in Zerodha Varsity / Z-Connect.

The above article claims the following condition is applicable for LTCG tax-exemption claimed under 54F

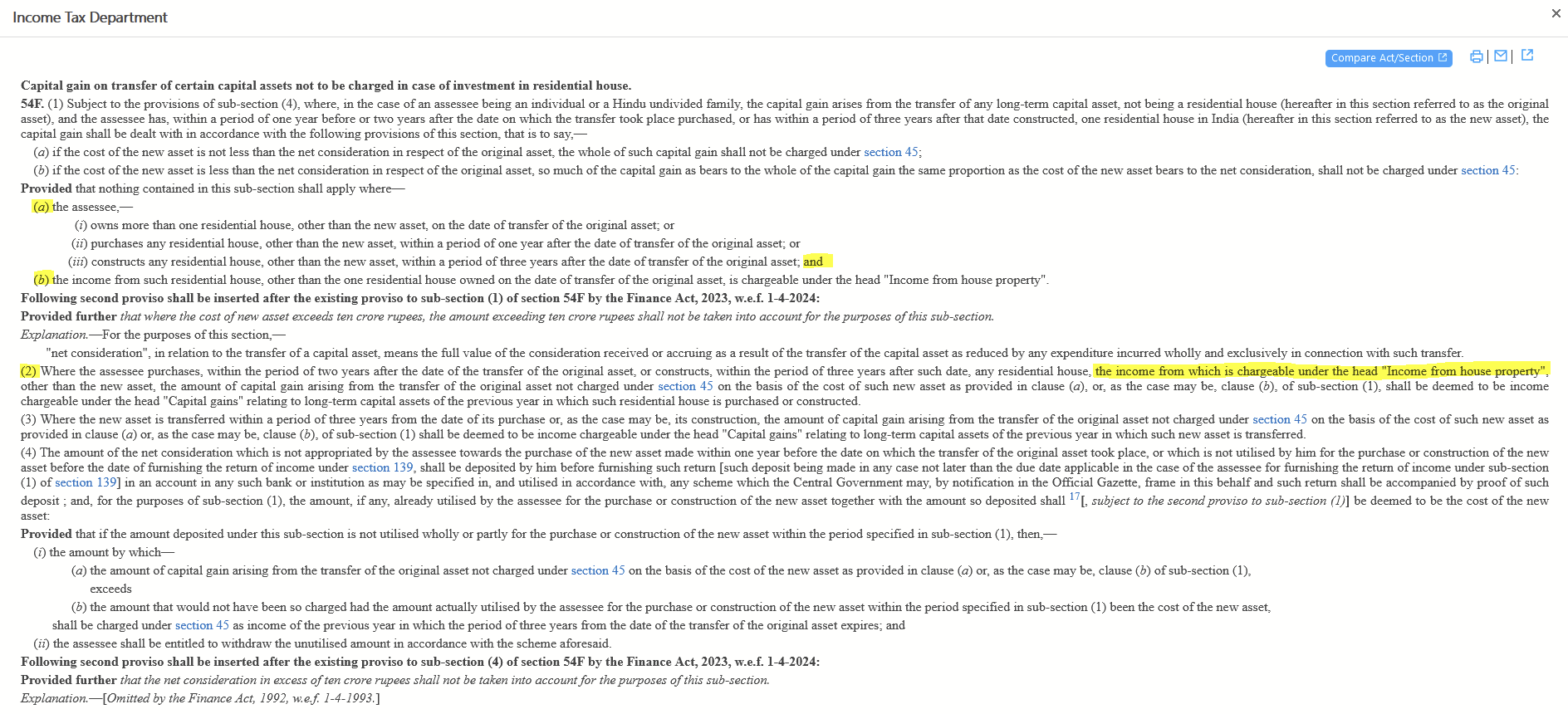

The taxpayer should not buy or construct any additional residential house

except for the one they’re claiming the tax break for a stipulated period,

or they’ll lose this benefit.

However, upon careful review of the Section 54F of the Income Tax Act,

it appears that the actual condition is that

one must NOT purchase/construct another residential house for 2/3 years,

the income from which is chargeable under the head “Income from house property”.

i.e. purchasing/constructing another house

within the stipulated period

on its own is NOT a restriction, as long as one does NOT receive any income from it.

Refer highlighted sub-sections, clauses, and explanation -

This one seems a bit tricky. Checked with the team but we wanted to verify this with @Quicko as well. Will get back to you in a couple of days. Sorry for the delay

In our opinion, we should always interpret the lines of the act according to the intent of the person drafting it. Thus, by providing an exemption in Section 54F, the government intended to provide relief to individuals who do not own multiple properties simultaneously and whose primary source of income is not derived from buying and selling properties.

We can take an example here:

Rental income can be taxed under the head “Income from Business & Profession” for a taxpayer engaged in the business of renting properties, which may include both residential and commercial properties. A developer or builder must record rental income from unsold flats under the head “Income from Business & Profession” rather than “Income from House Property”.

Therefore, the provision stating that income is chargeable under the head “Income from House Property” is added so that the properties are used for residential and not business purposes.

Furthermore, an individual cannot own more than two self-occupied properties at any given time. Upon acquiring a third property, even if there is no rental income, it must be treated as deemed let-out, and rental income must be shown at the minimum rent determined by the local authority based on the area and size of the property.

Coming to the original statement in the Varsity article,

that prompted this discussion…

The taxpayer should not buy or construct any additional residential house except for the one they’re claiming the tax break for a stipulated period, or they’ll lose this benefit.

So, in this scenario

individual has claimed 54F exemption on the LTCG used to purchase their first residential property.

individual purchases/constructs a second residential property within 2/3 years.

individual claims 54F exemption on LTCG used to purchase the second property as well.

Neither property is let out. No rent received from either property for the next 3 years.

@QuickoIs the individual well within their rights to properly claim LTCG tax exemption under Section 54F on both the residential properties ?

In our opinion, as soon as you purchase/construct the 2nd property within 2/3 years from the year when you claim the Section 54 exemption, the same shall be withdrawn and you will be liable to pay tax with interest and penalty.