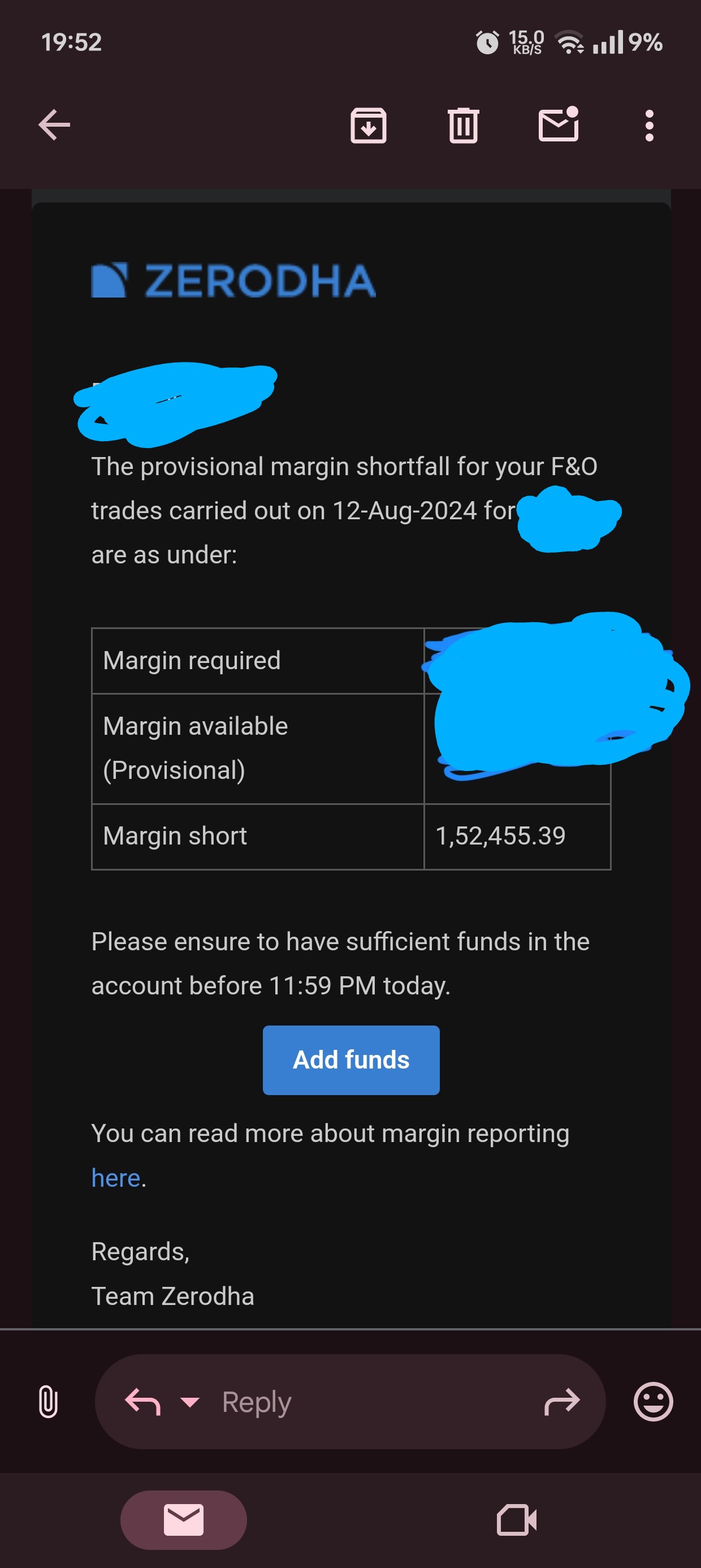

Hi,

I have recieved below email saying, please ensure to have sufficient balance till 11:59PM.

But I have closed all my positions and not carrying any overnight position.

What should I do ??

Thanks

Hi,

I have recieved below email saying, please ensure to have sufficient balance till 11:59PM.

But I have closed all my positions and not carrying any overnight position.

What should I do ??

Thanks

Hi,

A peak margin shortfall can occur due to various reasons during market hours. The Clearing corporation takes four random snapshots of your margin requirement throughout the day. The highest margin among these snapshots is considered the peak margin required for the day. If your available margin doesn’t meet this requirement, a margin shortfall occurs, and we notify clients to bring in additional funds when such a shortfall occurs.

You can read more about it here

Even if you’ve closed your position, the peak margin might have already been captured for your position. And by the end of the day if you do not have funds to meet the peak margin requirement, you will receive this notifications. To avoid this, please maintain sufficient funds or add funds when you receive such notifications.

So, Nothing to be done on my side right?

As this is an upfront penalty so broker has to bear the penalty in case clients fail to maintain the peak margin requirement. Going forward, we would request you to maintain sufficient funds in case you get an email about the shortfall

I have the same query.

When exactly does this penalty gets applied and by how much? Margin for the positions keeps fluctuating so at what instances the emails are sent? What exactly is the chronology of margin shortfall - emails sent - penalty applied?

Nothing is clear from your responses.

I’m confused with your question too ![]() so let me try and give you an overview after which you can ask any specific questions:

so let me try and give you an overview after which you can ask any specific questions:

Further, sometime in 2020, SEBI introduced the concept of peak margins. This involved taking random snapshots during the day and calculating margins based on the position of the client at that point of time. Multiple snapshots are taken, margins are calculated and the highest of the snapshot is required to be maintained by the client as margins. Peak margins are qualified as “upfront” in nature.

Now coming to the specific screenshot posted by the OP.

At the end of the day, from the Exchange files, we read the peak margin of the user charged by the Exchange. We compare the peak margins vs available funds of the user and if the peak margins are short, we notify clients and ask them to bring in funds.

How did the margin shortfall occur in the first place?

It could be as a result of the client breaking a hedge position and the Exchange having taken a snapshot then. In such cases, since we have little to no control, the client’s margin for the position exceeds available balance. Even when our RMS squares off positions for lack of margin, the margin shortfall still arises since the Exchange has already taken the snapshot and can’t be undone. So to ensure that there’s no penalty, we ask the client to bring fund the account to the tune of the shortfall.

P.S: this email is sent even if the client has squared off all positions at EOD, since the shortfall is on the peak margins (margin at the time snapshot was taken vs available margins)

Thanks @VenuMadhav . Now we’re talking.

Here are some further questions -

I already asked for a better info on margin as the current info on that page is less than pathetic, hope the team is working on it - NSE Circular on Short margin penalty refund - #230 by paekut

Yes

They’re random, that’s the whole idea. But based on the timestamps we get the file, we’ve guesstimated the snapshots to be as following:

1st - Between 10.20 to 10.35

2nd - Between 12.10- 12.30

3rd -Between 1.00 - 1.30

4th - Between 3.15- 3.30

If your margins become negative, it would mean that you have inadequate margins in your account for the positions you’re holding. This will naturally mean that your position is liable to be squared off by our RMS team

The square off is managed by the RMS team, and is not automated at the moment. The margin utilization is assessed, the type of margin shortall is recognized - for shortfalls arising out of increase in MTM losses, time until the next day is given; for upfront margins position may be squared off the same day.

The RMS will square off position to the extent of excess utilization - which means a portion of the position will be reduced to bring down the margin utilization to permissible/available limits

The email OP has sent is sent to users after the markets have closed and in situations where we’ve assessed the user’s balance to be less than the peak margin snapshot. In such cases, the expectation is that the user add funds for the day (even if the position has been closed) to the extent of margin shortfall to avoid any margin penalty being charged by the Stock Exchange.

Ok, let me rephrase this. Let’s say my margin goes into negative. How much negative should it go, in INR, so that it gets flagged to the RMS team to be squared off?

What are these positions exactly? Can you take an example?

And what is the timing of this square off? Or will they be done randomly at any point of time?

In the Calendar Spread example I quoted, could that mean that only the sell leg will be reduced and not the buy leg, as that frees up the margin more?

How are these permissible limits defined? And how’s it decided how much to square off from the overall position? If I have 900, will they square off 100? 200? 300? And what if they square off 100 but after an hour, the margin again goes into negative?

In the OP’s example, he has already avoided any possibility of margin penalty by squaring off the position. Do you think you should still fire this email? Shouldn’t you assess first whether the margin now is still insufficient, as an extra check, before firing this email?

Awaiting your response. Is this even a priority?

Also, don’t you feel there should exist a proper documentation of this process from Zerodha so that all questions like the ones above should not even be arising in the first place? Newbie traders currently have this huge cost of entry in the form of penalties, fees and things they learn by making losses. Don’t you think that properly documenting such stuff could bring that down sharply?

There’s no fixed number. For an account with 1L, when the margin becomes 2k negative, the RMS may not choose to square off, but if the losses become 10k, the position may be squared off. There isn’t a fixed number I can give. On days when the markets are super volatile, the focus is on squaring off positions for users whose margin utilisation is 150% over clients whose margin utlisation is 103%.

RMS will attempt to square off the least amount of positions to bring down the margin utilisation of the user under permissible limits. So if you’re holding 900, and the margin shoots up, and if closing 100 is sufficient to bring down the utilisation, only 100 will be squared off. Subsequently, if the risk goes up and the margins shoot up again after one hour, further positions may be reduced. So square off is only to the tune of bringing down margins to the extent that’s available in the client’s account. It does not account for future risk, even if it’s one hour away.

Usually, in a calendar spread, margins don’t go up significantly because the position is hedged and any one sided movement will get negated with the offsetting position you’re holding. However, in the worst case that a calendar spread has to be squared off, both legs of the contract will be squared up, since squaring off one leg will result in a risk to the client. It’s not unusual for the RMS team to even call up the investor and insist that funds be added to avoid squaring off of positions/give a choice to the investor to square off positions themselves.

You’re not getting the point. The snapshot is already taken, and once the margins are determined, they remain as it is, even if the client closes the position subsequently. As a broker, we have to ensure that such “peak margins” are maintained by the user on that day. If the user is short on margins, then we have to insist that the user tops up the account with funds to the extent of shortfall. Else, there is a margin penalty that is charged by the Stock Exchange.

Understand your requirement, but this is not a priority at the moment.

Most of it is available in the form of support articles. As I’ve said in the first reply, there isn’t one fixed number, which when reached, the position will be squared off. The portfolio has to be analyzed, human discretion has to be applied after which actions are taken and thus, it is tough to put it in black and white and describe.

As a client, if there’s one thing you ought to know, it is to maintain sufficient buffer for positions you’ve taken and avoid getting into a situation where a margin shortfall arises and a need for squaring off of positions comes about.

Hi Team,

Sorry to bump the old thread. As the topic is the same, I’m posting my question here. If required, I can open new thread.

I’ve documented my questions in the support ticket 20250930162982. I don’t think I’m getting the right answers from the customer support who is assisting now.

The issue is that I couldn’t see margin shortfall until the EOD on expiry day and only in the night (probably post exchange statement) I’ve got the email notification.

It’s clear that I’ve hedged legs in the last expiry but I’ve rolled over the hedges too with the one exception that the new ones are far OTM than the existing (i.e, last expiry) hedges which could’ve bumped up the margin requirement. While I expected some difference but not to the tune of over 20% shortfall. Since this is upfront margin shortfall, I wonder why I was allowed to open new positions yesterday with debit margin.

(Note: My available margin stayed positive throughout the day and one of my trade even got rejected due to lack of margin. This gave me an impression that everything was working as expected. So I wasn’t really aware my margin was already in debit and that too by -20+%. And there was no RMS auto-square off too if it was really negative, not sure if it was due to any defined buffer time).

Aren’t these conditions taken into account in the current margin calculation in Kites → Funds page? The ability to forecast such margin shortfall is important for F&O traders as it is not possible to manually calculate my margin requirements. This expiry was full of surprises and lack of prior notification or updated available margin as per live position have resulted in lot of firefighting and impacted my trading. I believe there is room to improve the margin calculation, upfront margin blocking and new position rejection mechanism.

While I’ve ensured the margin is freed and in positive balance now, I would like to know whether there is any margin penalty levied in this case. I couldn’t see any interest statement updated as of now.

Please take a look at the ticket and help me clarifying this.

Hello, we are checking this

Elm margin shortfall come under upfront Margin shortfall,so penalty is not pass to customers?

yes upfront penalty should not be passed to the client according to the exchange…lets see what zerodha says

Hi,

As per the screenshot shared by you, we can see that there is a shortfall in your EOD margins for the position held, which is likely to become your BOD margin on the next day. This shortfall will be captured in the first peak snapshot. If sufficient margins are not maintained, a penalty may be applied, or your positions may be squared off. Please note that if the penalty is due to upfront margin shortfall, it will not be passed on to the client. However, if it arises due to an increase in upfront margin requirements because of a hedge break or the expiry of one leg, it will be passed on to the client. Please check this article for more info.

See d first row,second column in screenshot ,dere is zero margin shortfall,in d second row dere is a short fall of 4 lakh rupees,in dis u have added extra 2 percent elm margin , according to sebi 2 percent elm is applicable only in expiry day,but u r adding elm Margin on 1dte expiry and send fake provisional margin shortfall message ,dere is zero margin shortfall in margin statement also,

If u want to add 2 percent elm den add in d expiry day morning n den send provisional margin shortfall if dere is shortfall ,

Hi, yes, we now have a system in place that prevents hedge breaks.

But sometimes it doesn’t allow me to exit if additional margin is blocked because of delivery margin. If I don’t add funds I can’t exit

@Jyoti_P_Deshpande when we receive email why provisional margin is mentioned on subject of email, it should be final margin. I got penalties and on the basis of provisional margin email.