Its transperent as it is directly allocted by RBI.

Overall 1 week process i think. exact duration I forgot.

It will be listed on Tuesday and till Thursday it will be available for subscribe. After that it takes some 2-3 days to appear in your demat.

once available in demat you can pledge. next day you will get margin

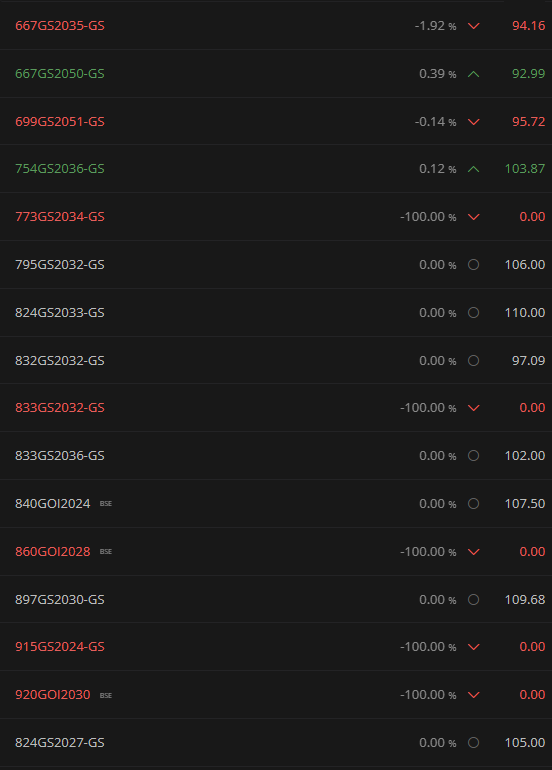

depends on the Gsecs… some has no liquidity at all and some have little price variation.

In kite it is mainly on ask/bid… you may have to wait till you get fair value. ( you have keep putting limit order at your desired price everyday. if any seller wishes to sell it will get execute. although because of limit of order, your capital will be blocked…)

In coin it is auction based… I presume would at par with market running value.

I have purchased 1 lot of 7.38% GS 2027 from coin as a trail… after that purchased 49 lots from kite as i dont wanted to wait for 1 more week…

There is nothing called as fair value, it all depends on your priority & purpose.

Facevalue is set to 100. If you buy lower say 98 you get higher yield. GS7542036 will yield 7.69% annualy

whereas if you buy for 102, you get 7.39% instead.

Buying on coin wont assure you any preset prices, it still goes through auction. Its better directly to bid/ask yourselves via kite and save the 6/10000 brokerage.

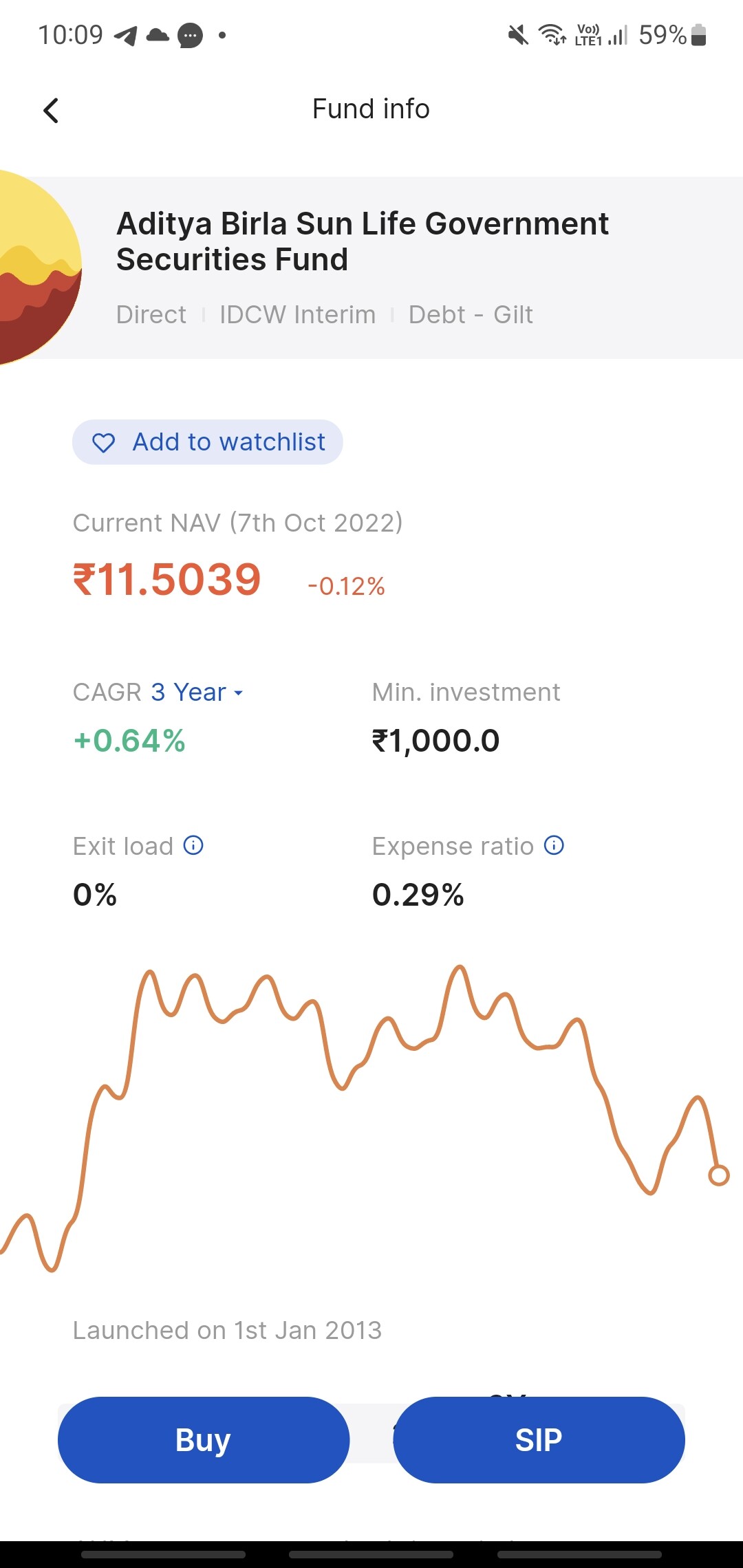

I checked out Mutual funds which invests mainly in Government securities. I expected to see a linear return graph with stable CAGR. But the fund is super volatile. Any idea why?

Because of interest rates and the duration of the securities these bonds hold. Gsec bonds are very volatile, they can even give negative returns for months.

There are few factors you can take into consideration.

Simple facts

Gsecs pay out interest half-yearly. TDS is not deducted - but it is taxable at your income tax slab

Growth option mutual funds do not pay out anything & is taxed when you withdraw at the applicable slab

Complicated facts

Gsec pays you simple interest, if you dont reinvest or use it wisely the wealth does not compound. If you wish to get compound interest - its not feasible that easily

Growth option mutual funds auto compound monthly or yearly as per the scheme, at the end of 10 years the compound interest will overtake the original principal amount (say at 7 to 8% yearly return)

If you are using Gsec or mutual funds as pledge collateral to do options or futures trading then the mutual funds are a better alternative as the collateral balance automatically increases as the nav increases. Whereas Gsec collateral value remains the same all through.

If you are just starting, dont have any other incomes and trading is not generating consistent returns then you can prefer Gsecs as you will get a comfort of a salary like income paid half yearly

Which mutual funds act as proxy for G-secs without any additional interest rate risk?

When we purchase G-secs, irrespective of trajectory of interest rates, we know that we will get fixed interest and capital at the end of the term. Can we remove interest rate risk if we remain invested in gilt funds or equivalent? Willing to wait till the end of the tenure for interest payments too.

I have observed that most of the gilt funds are open ended, so not sure how they will behave if interest rates keep going up for a period of 5 years or more.

@sameer_ranjan i cannot suggest a specific mutual fund because there are lot of dynamic variables in it. However i can theoretically tell you how to find a fund.

During a interest rate hiking regime always find a mutual fund that invests in ultra short term debt like a liquid fund, money market fund. Check if they are investing in 7 day to 30 day tenures.

During a interest rate falling regime invest in long term bonds like 8 to 13yr funds, GILT constant maturity etc

Getting the interest rate regime direction is more difficult than predicting the direction of nifty index - thats why most of them gets stuck in bonds.

@Ragavendran_V - NSE debt ETFs UNDERLYING → GSEC

Again i havent seen an outperformance on the ETF vs direct GSEC in the last 2 to 3 years. May be because the ETF mentioned are long term and right now the interest rates are rising.

We cannot remove interest rate risk by investing in gilt funds, we remove the credit risk, and on the contrary if the gilt funds hold long term gsecs, the interest rate risk remains for extended periods of time, thereby giving negative returns too.

I think there used to be gilt funds which held 1 year maturity gsecs, but they don’t exist anymore, I think we have long term gescs now.

Forgot to say something. When you purchase a bond with FV = 100 for 103, you stand to lose the capital of Rs3 at the end of tenue

If you purchase 10000 qty of 754GS2036 at 103 ie 10 lakh qty, you would need to pay 10.3 lakh and after tenure you will get back only 10 lakh. Rs3 * 10000 qty is loss in capital

Govt will pay only face value of bond. that is 100. The reason it is trading at 103 could be bond is issued at high interest rate and now due to lowering of interest rate current yield is reduced so automatically face value will change as interest rate remains same as the level at issue time.

Suppose if bonds issued at face value 100 at 8 % interest. Govt will pay 8% interest and pay 100 back with face value at expiry. So if interest rates fall then face value will increase so new buyer gets same interest rate. But if current yield is 7 then face value will increase to compensate.

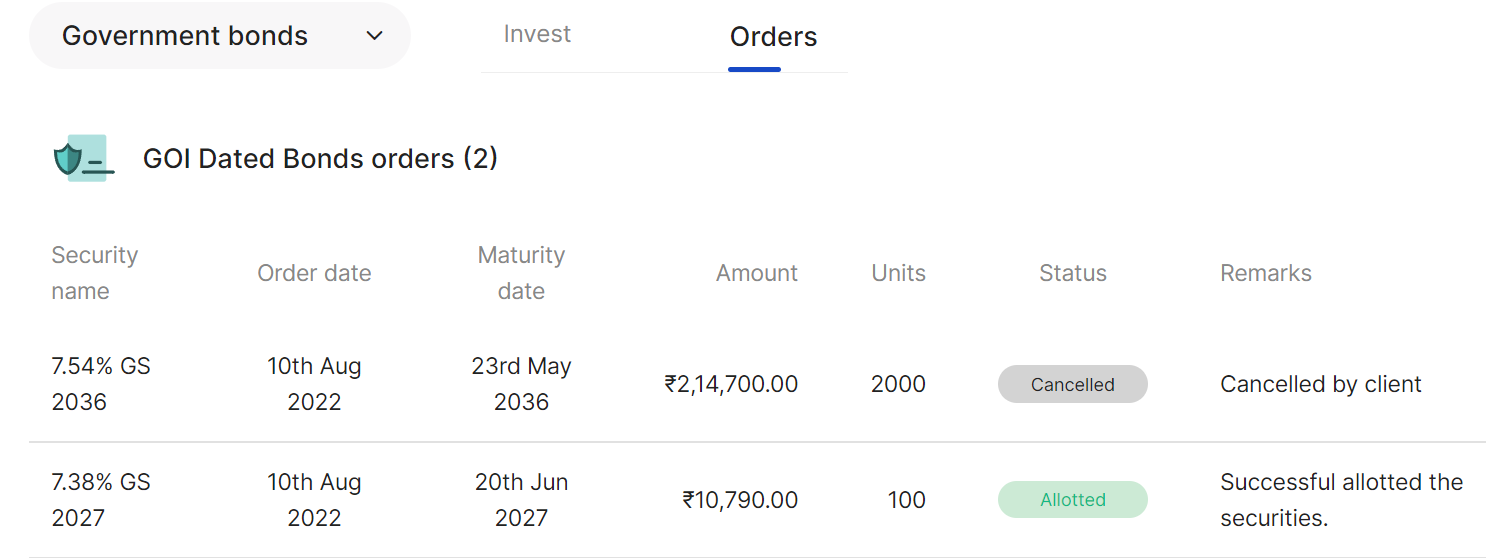

Did you get any order confirmation from Coin on Thursday? When did the funds get deducted from the account? @ShubhS9 I placed an order today, and post 8pm cutoff time, can’t see my order anywhere on the app. Nor has the amount been deducted/blocked. A confirmation mail at least should go out.