Background Summary

Background Summary

-

Age: 21

Age: 21 -

Investing Since: 2023

Investing Since: 2023 -

Risk Appetite: Very High

Risk Appetite: Very High -

Investment Horizon: Long-term (Capital Growth Phase)

Investment Horizon: Long-term (Capital Growth Phase) -

Financial Goals:

Financial Goals: Become financially independent by age 30

Become financially independent by age 30 Build enough capital to live off dividends and interest

Build enough capital to live off dividends and interest Let compounding kick in post $1M net worth

Let compounding kick in post $1M net worth

-

Current Status:

Current Status: Full-time student

Full-time student Working a full-time job alongside studies

Working a full-time job alongside studies Moved abroad from India in search of better opportunities

Moved abroad from India in search of better opportunities

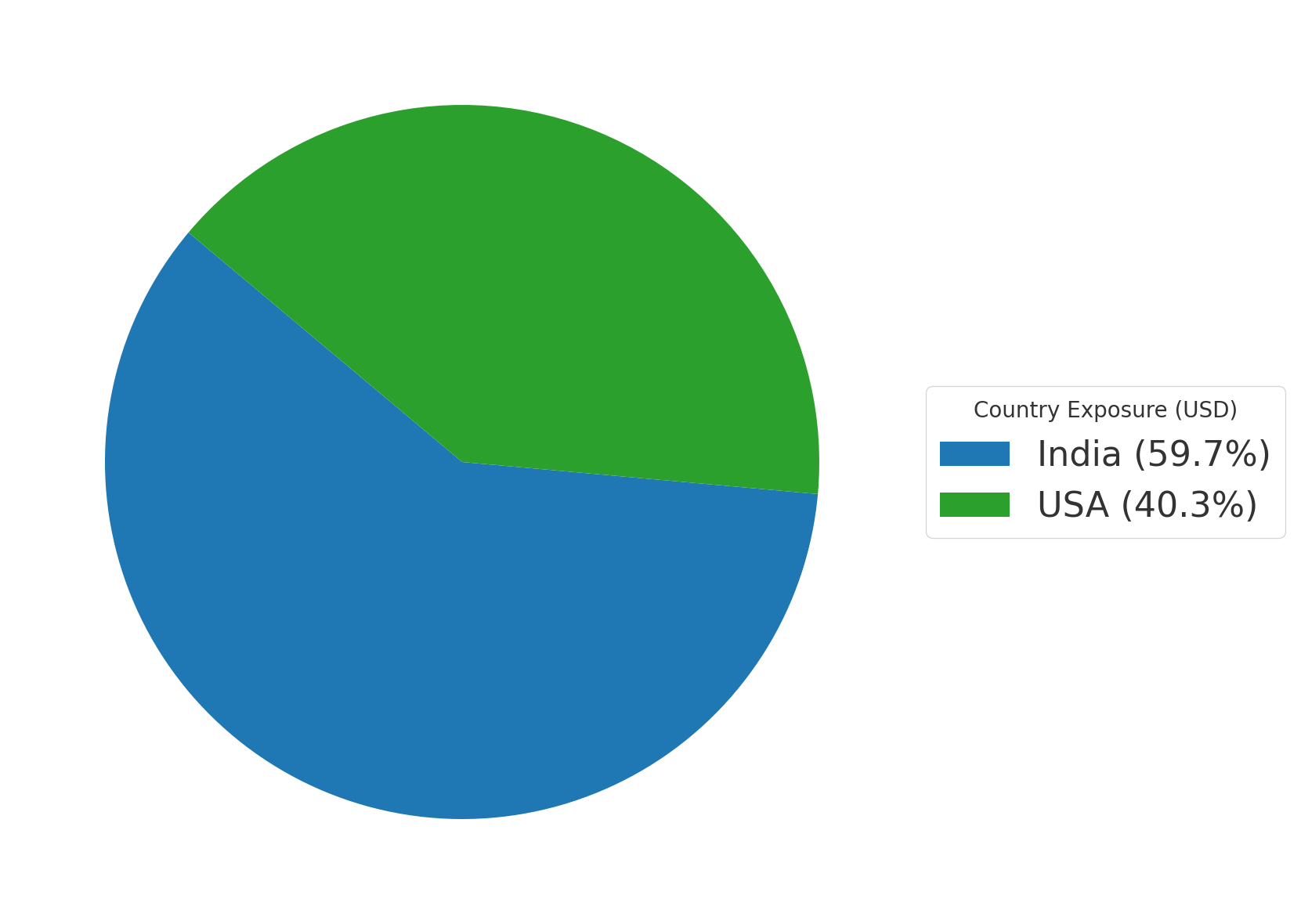

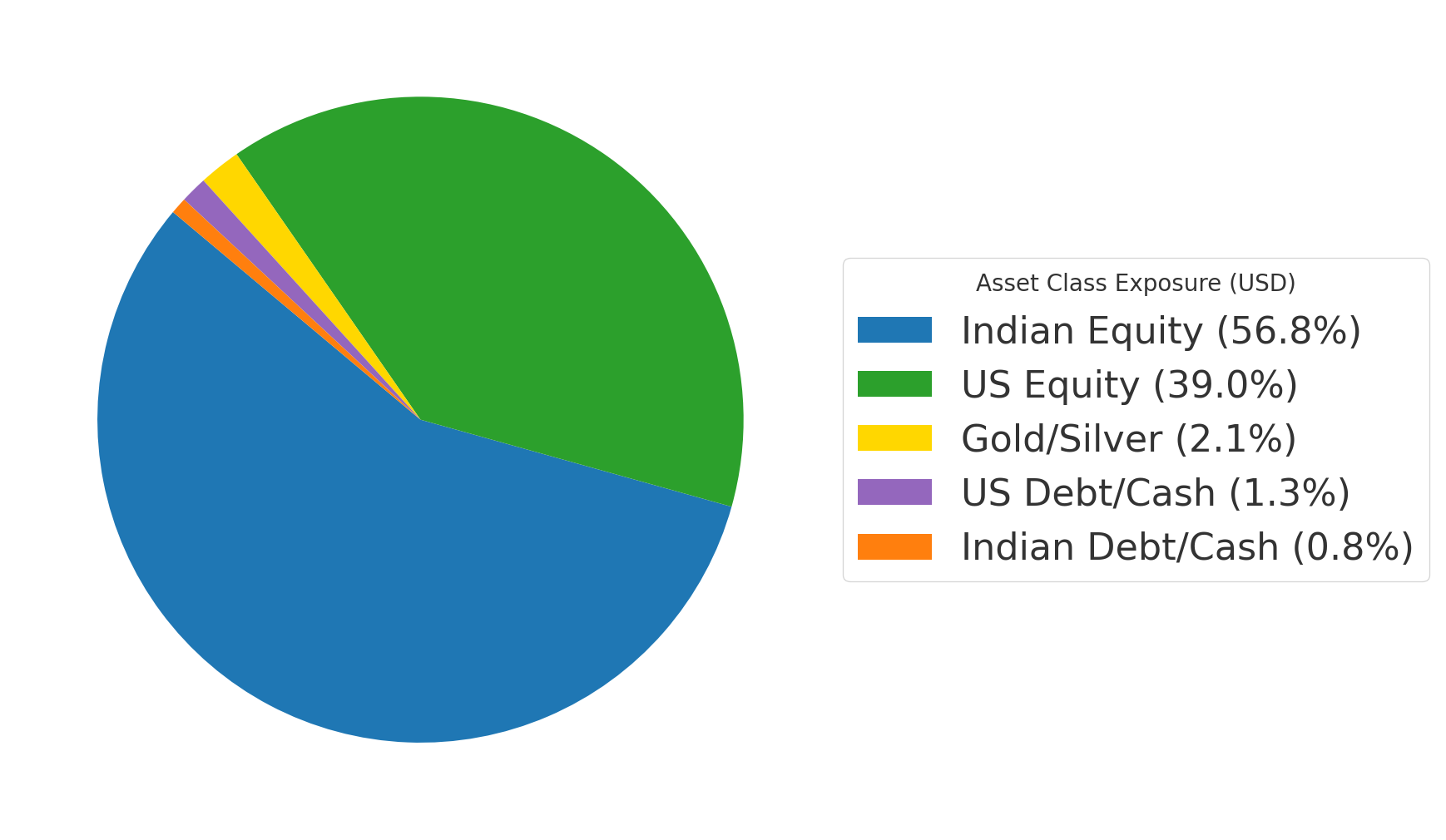

Capital Allocation Overview

Here is a consolidated view of my current investments across regions and asset classes.

| A | Total Value |

|---|---|

| India (INR) | |

| Listed Equity | 436,747.49 |

| Unlisted Equity* | 0 |

| Equity Mutual Funds and ETFs | 48,54,877.63 |

| Debt Mutual Funds and ETFs | 77,001.99 |

| USA (USD) | |

| Listed Equity | 26,297.50 |

| Equity Mutual Funds and ETFs | 17,485.00 |

| Cash/Money Market | 1,500.00 |

Total Portfolio Value

Total Portfolio Value

| Region | Total Value (INR) | Total Value (USD) |

|---|---|---|

| India | 53,68,627 | 67,024 |

| USA | 37,58,406 | 45,282 |

| Total | 91,27,033 | 112,307 |

Questions I Asked Myself

Questions I Asked Myself

Why didn’t I include the cost basis?

Why didn’t I include the cost basis?

Because I believe in Prospect Theory — we tend to overvalue losses and gains relative to their actual impact. Instead of focusing on whether an investment has made me a profit so far, I prefer to ask: “Is this asset still worth holding based on its future potential?”

The past doesn’t change the opportunity ahead.

Why is my unlisted equity marked as ₹0?

Why is my unlisted equity marked as ₹0?

Most of my unlisted equity holdings (except Oyo and Otis) are currently illiquid and valued lower than their purchase price.

Since I don’t plan to sell them anytime soon — not until their IPOs, which could be years away — I’ve conservatively marked them as zero.

Special case: Otis

Otis has announced a mandatory capital reduction for minority shareholders. I purchased shares at a ~10% discount to the buyback price and am currently waiting for NCLT approval to complete the process. It’s less an investment and more a strategic event-based trade.

Covered calls on Intel?

Covered calls on Intel?

Intel is one of my core holdings, and I occasionally generate extra yield by selling covered calls — but only at strike prices I’d be genuinely happy to sell at.

Thanks to relatively high implied volatility (IV), this strategy has worked well and provided solid short-term returns without compromising my long-term thesis.

I purchased 200 shares of Intel at an average price of $22, amounting to a total investment of $4,400. Since then, I’ve generated approximately $500 in premium income year-to-date by selling covered calls with strike prices between $25 and $27 — which aligns with my original take-profit range.

While I love this strategy, the amount of time and effort it takes is very high, hence I don’t do this with any of my other holdings. Also- you need at least 100 shares to sell covered calls and Intel was the only one in my portfolio for which I could do this.

What are my current observations and next steps?

What are my current observations and next steps?

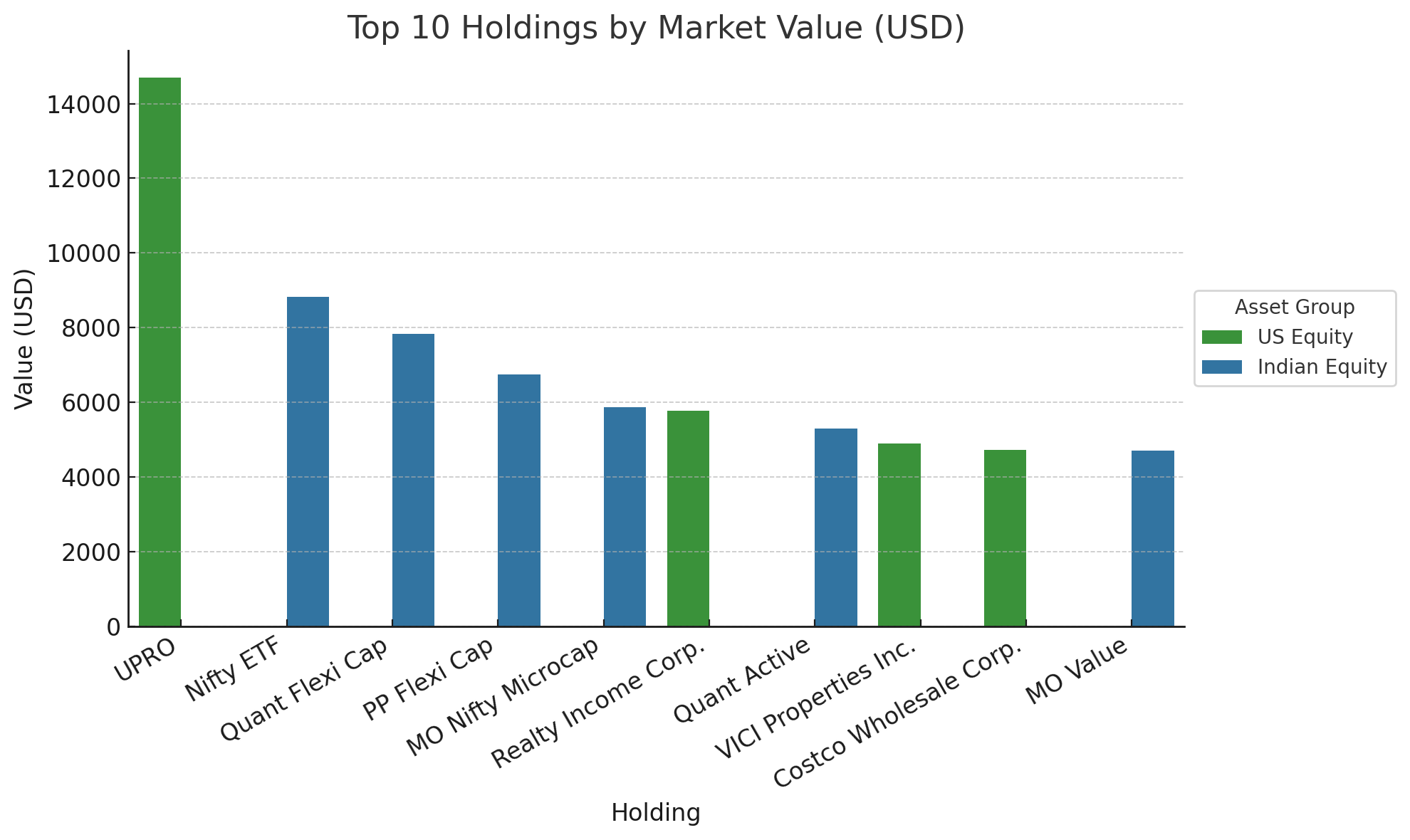

- Given global uncertainty, I’m considering a higher allocation to gold, especially since two of my largest positions are in EXTREMELY high-risk assets (3x Leveraged S&P500 ETF and an MO Nifty Microcap 250 Index fund).

- My portfolio has struggling in recent months, in line with broader market trends. While I’ve thought about expanding into Europe or China, I’m cautious about over-diversification.

- VICI and Realty Income have been standout performers — they provide consistent dividends and are relatively resilient to market sentiment. I also have high conviction in SCHD, and plan to increase exposure.

- In India, I plan to exit some individual equity positions once the market recovers slightly. It’s increasingly inefficient to track so many companies, so I’ll be reallocating into mutual funds with a few concentrated stock bets based on my own research.

- Quant Mutual Funds were giving ludicrous returns before the market downturn and being greedy, I allocated a little too much capital towards them. As of now, I have ~13.7 Lakh or 15% of my entire portfolio (25% of my Indian portfolio) in mutual funds by Quant. I think it might be worth moving some of this to a different AMC. Now might be a good time for this given the market downturn because some of them are at cost, potentially saving me Tax todo so now rather than when it is in profit.

- PPFAS in India is absolutely amazing and underrated. My only complain with it at the moment is extremely long minimum holding period to avoid the exit load. I understand it is for long term investors but this makes occasional equity-debt-gold rebalancing or tax harvesting difficult.

- I also intend to shift more capital outside India due to unfavorable tax treatment on capital gains. I’m making no new investments in India — only reallocating existing ones. All new contributions are directed to my U.S. portfolio, and potentially towards more international exposure.

Have my portfolios outperformed?

Yes. So far, both my Indian and U.S. portfolios have consistently outperformed their respective benchmarks (Nifty 500 and S&P500).