RBI recently released the 25th edition of financial stability report and here are some of the highlights curated by our team.

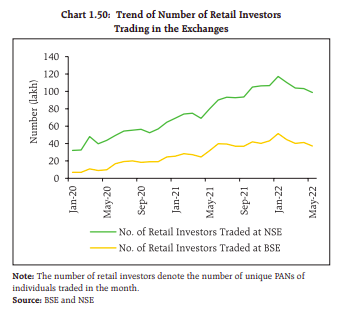

1. Trend of Number of Retail Investors Trading in the Exchanges

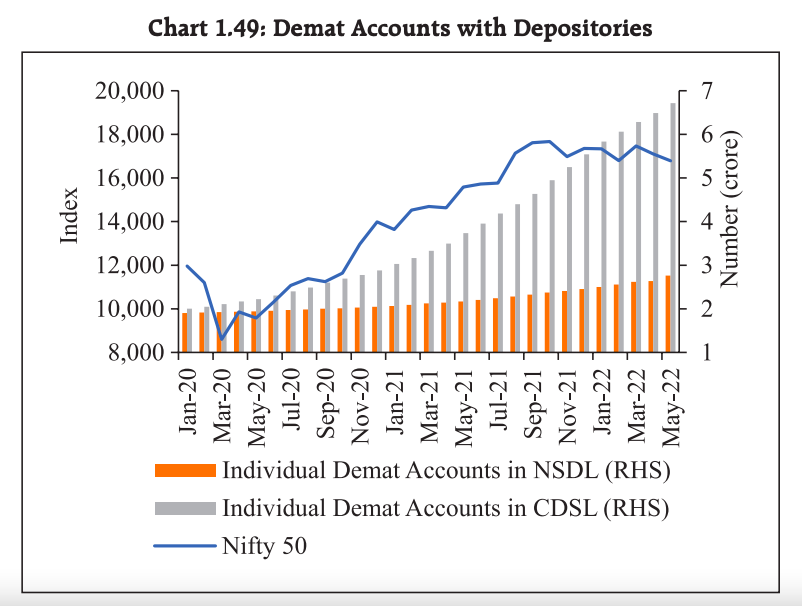

During January 2020 to May 2022, the number of demat accounts of individuals has increased by 3.4 times in the Central Depository Services Limited and by 1.5 times in the National Securities Depository Limited.

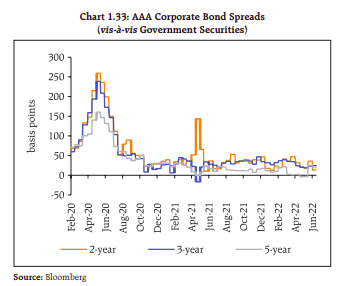

2. AAA Corporate Bond Spreads

AAArated corporate bonds were priced at the same level as risk-free government securities, with spreads turning negative on occasions. As on June 16, 2022, the yield on 3-year AAA-rated corporate bonds was 7.40 per cent, 141 bps up from end-March 2022.

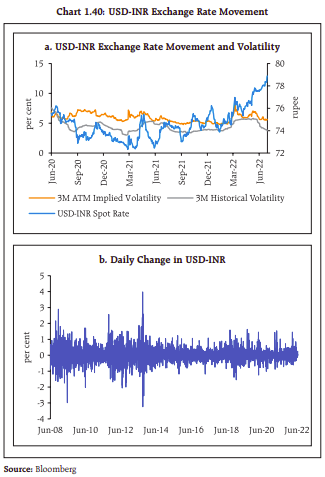

3. USD-INR Exchange Rate Movement

The INR, experienced some volatility and depreciated by 5.7% against the USD during the calendar year 2022 so far (up to June 29). On a financial year basis, the depreciation of the INR was lower at 3.9 per cent.

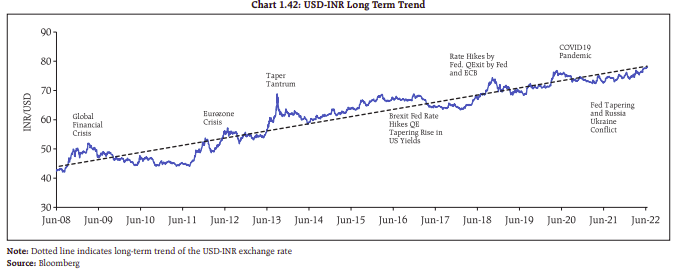

4. USD-INR Long Term Trend

The USD-INR exchange rate touched an all-time low of 78.98 on June 29, 2022, as recession fears and risk-off sentiment spread worldwide.

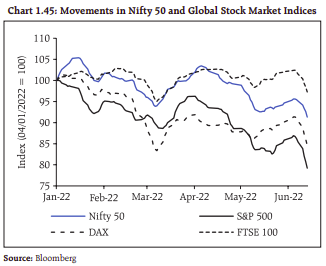

5. Movements in Nifty 50 and Global Stock Market Indices

Indian equity markets have turned bearish and have registered negative returns, with the BSE Sensex decreasing by 11.6 per cent and Nifty 50 declining by 11.5 per cent between end-December and June 16, 2022.

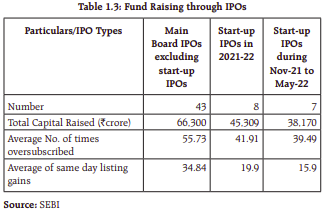

6. Fund Raising through IPOs

Corporates raised the highest ever funds through IPOs in 2021-22, amounting to 1.11 lakh crore. During November 2021 to May 2022, seven start-up IPOs were listed, raising 38,170 crore, with an average oversubscription rate of 40 times and 4 of them registered gains on the day of listing.

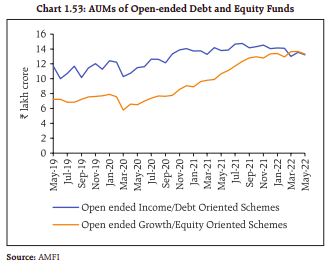

7. AUMs of Open-ended Debt and Equity Fund

Assets under management (AUM) of openended mutual funds, both debt and equity, have grown by 65 per cent since the onset of the pandemic and stood at `26.5 lakh crore in May 2022.

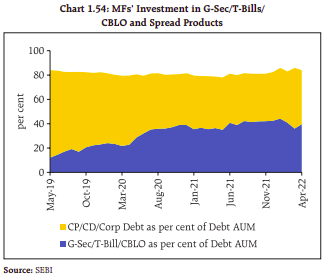

8. MFs’ Investment in G-Sec/T-Bills/ CBLO and Spread Products

Investors’ preference for safe assets in recent times is reflected in the rising share of liquid assets in aggregate holdings of debt mutual funds.

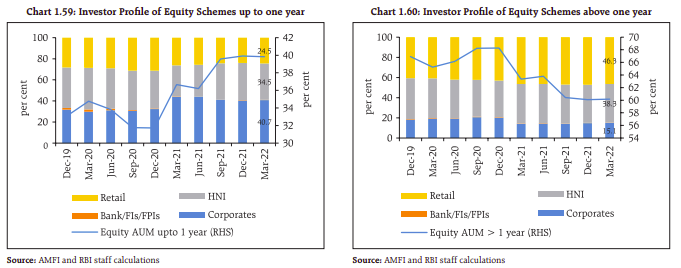

9. Investor Profile of Equity Schemes

The share of equity funds held for longer duration (beyond one year) has gradually declined in favour of holdings up to one year.

10. Cross Margin in Commodity Index Futures

A cross margin benefit of 75 per cent on the initial margin is allowed if a client arbitrages or holds offsetting positions in index futures and futures of its underlying constituents or its variant.

11. Retail Investor Protection

To mitigate the misuse of POA, a separate document called “Demat Debit and Pledge Instruction” (DDPI) was introduced in April 2022, under which the clients are required to explicitly agree to authorise the stock broker and/or to access their beneficial owner account for the limited purpose of meeting pay-in obligations for settlement of trades executed by them.

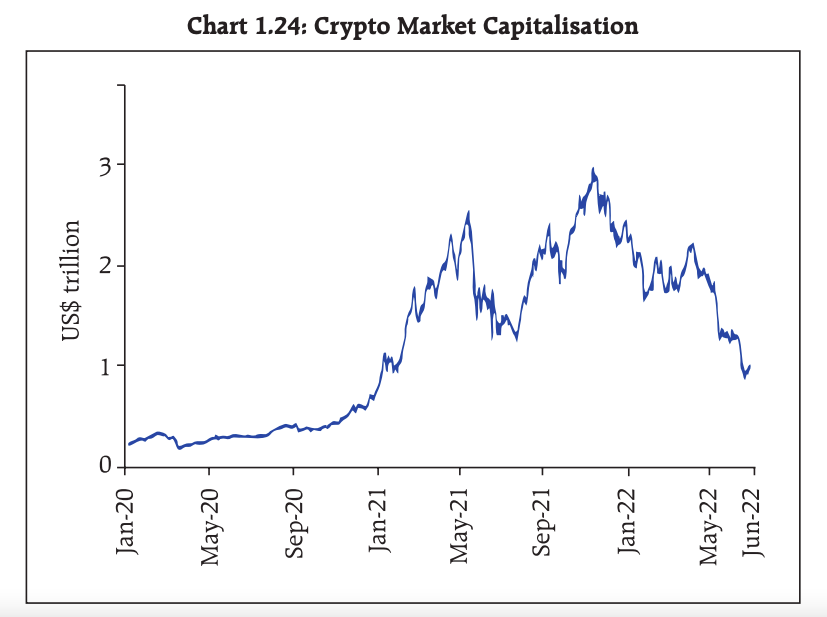

12. Cryptocurrencies are a clear danger. Anything that derives value based on make believe, without any underlying, is just speculation under a sophisticated name. While technology has supported the reach of the financial sector and its benefits must be fully harnessed, its potential to disrupt financial stability has to be guarded against. : RBI Governor.

-

Reflecting the uncertainty surrounding the course of the war, persistence of inflation and the future path of the pandemic, global uncertainty has surged, which by itself, could reduce global growth by 0.35% points.

-

The benchmark 10-year G-sec yield hardened by 116 basis points (bps), between December 2021 and June 16, 2022, to 7.62%, mainly reflecting global developments interspersed with domestic factors.

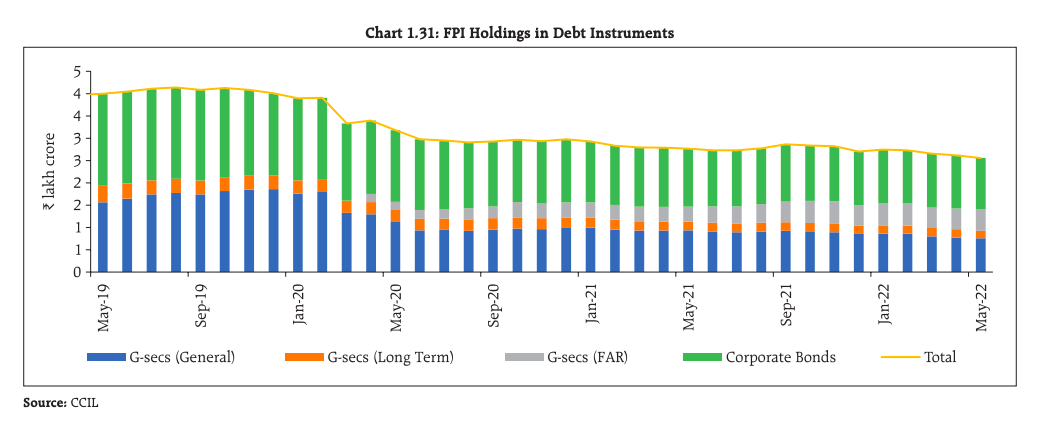

Foreign portfolio investments in Debt Instruments.

-

The war has exacerbated supply chain disruptions and forced a sharp rise in commodity prices with heightened volatility.

-

The market value for cryptoassets grew tenfold from early 2020 to late 2021 when it peaked at almost USD 3.0 trillion before recording a sharp decline below US $ 1 trillion in June 2022.

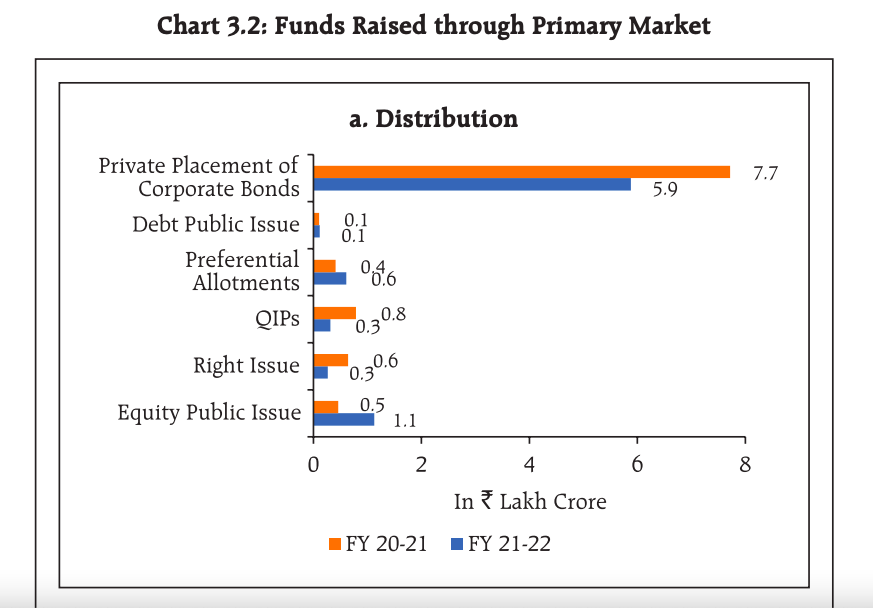

17. The total capital raised in primary markets during the period 2021-22 stood at 8.3 lakh crore, as compared with a mobilisation of `10.1 lakh crore during 2020-21.

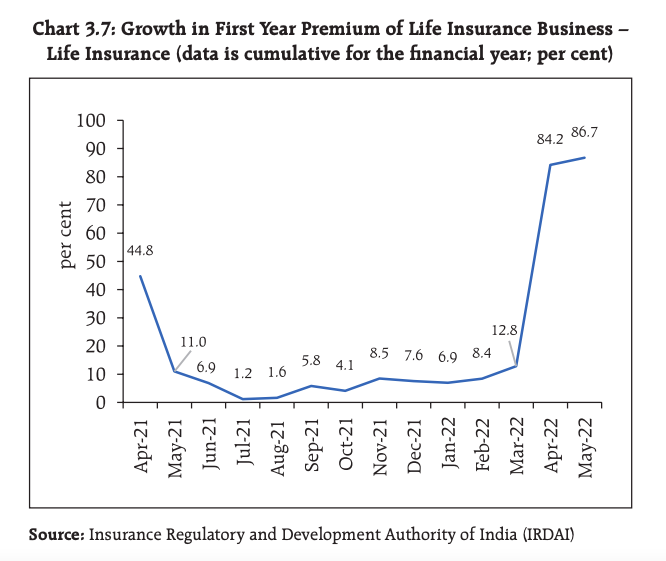

18. The life insurance industry experienced low level of activities during the period April-May 2021 on account of second wave of the pandemic. However, the industry experienced normal level of activities during the period April-May 2022.

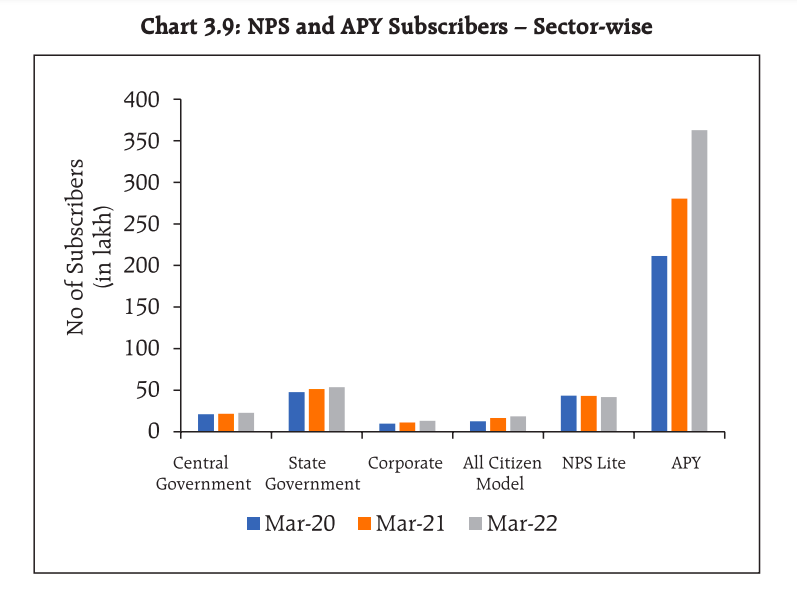

19. The National Pension System (NPS) and the Atal Pension Yojana (APY) recorded a 22.6% annual growth in number of subscribers and 27.3% growth in the corpus during 2021-22.

PS : This report is of 158 pages and has 100s of interesting bits of data. We can share and discuss if there are other interesting stats in the thread below ![]()