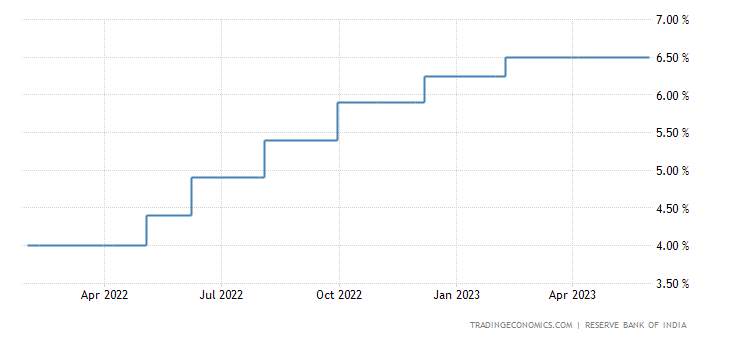

If you look a the US FED funds effective rate - there is a sharp increase from Mar 14 2022 to May 17 2023

i.e from 0.08% to 5.08%, whereas RBI has gone from 4% to 6.5%

In my view - both the central banks cannot be right, one of them is certainly doing it wrong!

As it stands RBI has shown too much restraint in hiking rates thereby protecting the major banks in India. It may even seem RBI is winning vs FED.

Why would any foreign investor put money into India @6.5% when they get it at 5% in US + assured USD stability? I still think if RBI does not match up the rates, we could see capital erosion - your thoughts??

2 Likes

Both the central banks or any of the central banks in the world will increase rate to tame inflation. US inflation is totally different from India inflation. Inflation at the peak was 8.3% in USA for 2022. Whilst India peak inflation was 6.67. Although the inflation rate cannot be compared between two countries, what the central bankers are doing is to control the same. One of the tools that they have is to hike interest rates. One of the core RBI mandate is to control inflation.

How does hiking rates protect major banks. Not clear. These rates are nothing. The highest repo rate was 14.50 in 2000. Nothing happened to banks then. I do remember those years for NRI banks used to double money in 4 years time.

Have a look at this chart.

Not clear on what this 6.5% is.

India forex reserve is almost 600billion.

Currently for USD FCNR, Yes bank is giving 6% upto 2 years. SBI is around 5.35%. INR deposits is around 8% for similar tenor with small banks. NRI would defenetly use this opportunity to pump in money in FCNR rather than in INR as this has additional currency depreciation. Not seen such high rates been offered for USD FCNR deposits,

too much rate hike will put lenders under pressure. new loan growth should exceed the deposit rates. Old borrowers if not restructured will leave a hole in banks balance sheet.

When there is a increase in benchmark rates, this is automatically passed on to all customers on the interest reset date. There are fixed rates loans which is a rarity and floating rates, these fixed rates are given after taking into account the maximum hike that can happen. For a bank, majority of their portfolio will be linked to a benchmark which increases as and when the rate hike happens.

In fact when rate increases, the NII (Net Interest Income) of a bank jumps sizably. due to the interest rate hike. The cost which is the hike in deposits happen over a period of time as no bank increases deposit rates immediately. Earlier there was no penality for premature closure of deposit, nowadays, customers have become savvy, and close and reopen the deposits. Hence they have started penal rate as well. This is additional income as well.

In fact the effect will be on the borrowers who might face cash flow shortages due to the hike in interest. Normally this is covered as banks make marginal contingency provision for this. Bank is the only industry where income jumps when rate is hiked. Whether the customer pays or not comes in after 3 months or after the moratorium period which is generally given for major capex loans.

Agreed 100%. Rate hike is good for banks in theory. There is a point beyond which the borrower will be unable to service the EMIs. Not just the individual but the corporates also.

only for individuals. Corporate loans are not re-structed automatically.

If the cost of financing goes up, you know what happens to the operating margin.

Corporate loans are high ticket loans and they are linked to benchmark rates. No banks are allowed to give Corporate loans until and unless they are linked to bench mark rates which when increased will automatically pass on to the customer.

Again I am writing the above from the Bank Balance sheet perspective and not from the ultimate customer. Yes customer will get affected,

The answer is true. NPA will be lower as customer can pay which means lower provision the bank has to make.

When Interest rate is high, the NII will jump for the Bank (in the bank balancesheet) due to the rise in interest rate. Bank will have to make additional provisions but there will be a lag.

Okay now I understood where the disconnect is. According to me a high interest rate for an elongated period of time is suicide for the banks.