In view of the rising CPI inflation, the Reserve Bank of India (RBI) has begun tightening its monetary policy stance following most other major central banks. Just last month, i.e. May 2022, the RBI raised the policy repo rate by 40 basis points (bps) to 4.40%, after more than 2 years. While the stance of the policy was kept accommodative, the RBI said that it would be ‘focusing on withdrawal of accommodation’ to ensure that inflation remains within the target going forward, while supporting growth. During such a rising interest rate scenario, how should you position your debt portfolio?

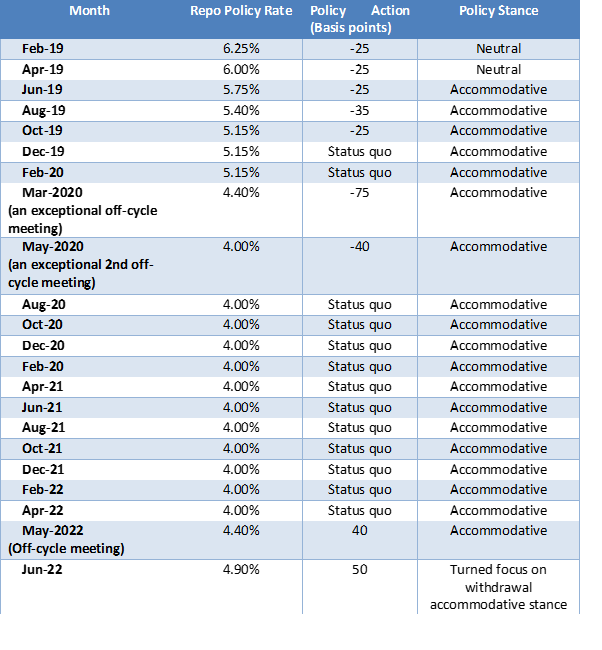

Table 1: RBI Monetary Policy Actions

Data as of June 8, 2022

(Source: RBI Monetary Policy Statements)

In the monetary policy meeting held today (i.e. June 8, 2022) the RBI once again increased the repo rate by 50 bps (much higher than 40 bps expected by most economists), placing it at 4.90% with immediate effect. Further, the Monetary Policy Committee (MPC) decided to remain focused on the withdrawal of the accommodative stance.

The consecutive rate hike, however, is not very surprising, given that the RBI Governor, Mr Shaktikanta Das, earlier indicated that in the current inflationary times “expectations of a rate hike is no brainer”.

The decisions of the RBI are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4.0% within a band of +/- 2.0% while supporting growth.

The RBI, at present, sees risk to inflation trajectory emanating from…

- Tense geopolitical situation and elevated commodity prices

- The shortfall in the rabi production due to the heat wave

- Pressure on edible prices due to global supply conditions (notwithstanding some recent correction due to the lifting of an export ban by a major supplier)

- Elevated international crude oil prices (which pose a risk of further pass-through to domestic petrol pump prices, even though some relief is passed on to buyers after the recent cut in excise duty)

- Upside risk from revisions in the prices of electricity

- Higher logistic costs

Moreover, the manufacturing, services and infrastructure sector firms polled in the Reserve Bank’s surveys expect further input and output price pressures going forward.

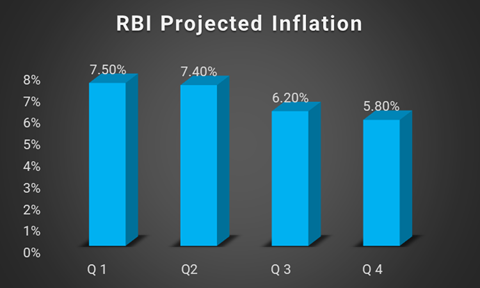

Taking into consideration these factors and on the assumption of a normal monsoon in 2022 and an average crude oil price (Indian basket) of US$ 105 per barrel, the RBI has now projected CPI inflation to be at 6.7% in 2022-23 (with Q1 at 7.5%; Q2 at 7.4%; Q3 at 6.2%; and Q4 at 5.8%, with risks evenly balanced.

RBI Projected Inflation as of June 08, 2022

Past performance may or may not be sustained in the future.

These projections make it clear that CPI inflation is expected to be above the tolerance level (of 6.0%) through the first three quarters of 2022-23. The MPC notes that persisting inflationary pressures could set in motion second-round effects on headline CPI.

Against this backdrop, you may be wondering where interest rates are headed.

The RBI’s latest monetary policy statement mentions the need for calibrated monetary policy action to keep inflation expectations anchored and restrain the broadening of price pressures. It is also decided to remain focused on the withdrawal of the accommodation to ensure that inflation remains within the target going forward while supporting growth.

From this, it is clear that we are in an early stage of the interest rate upcycle.

Interest rates and bond prices are inversely related. In other words, when interest rates go up, bond prices move down, making it economical for you to invest and vice versa.

In the year 2022, bond yields so far have already shot up and may inch up further. With ensuing rate hikes, and additionally owing to the weak rupee, higher government borrowings, higher debt-to-GDP ratio, and overall economic uncertainty, it is possible that policy rates may move up further this year. For you, the investor, this is an opportunity to earn better from certain debt instruments.

Corporate Bonds

The yields in the corporate bond segment – across ratings and tenures – have moved up. However, not all corporates may afford borrowing at a higher coupon/interest rate for the corporates (particularly in challenging times), and therefore the issuances may be low. And if a company is offering a higher coupon, you need to be careful; assess if it has the financial strength to service its debt obligations.

It would be best to stick to corporate bonds that have consistently commanded AAA ratings (highest safety) and not to choose the ones with longer maturities (given the interest rate risk involved) or those with a lower rating (given the credit risk involved). Do not simply get lured by high interest or coupons, for higher returns, as it would also attract higher interest risk as well for you, the investor. Keep in mind, that the risk of default is higher in the case of low-rated corporate bonds.

Government Bonds

Currently, the yield on the 10-year government bond is 7.53%, while on the 5-year government and 3-year government bonds, the yields are around 7.38% and 7.07%, respectively (as of June 7, 2022). With such yields (and the possibility of moving up further), investing in government bonds may be rewarding. That said, given that we are in the early stage of a rising interest rate scenario, avoid government securities with longer maturity debt papers.

Despite India’s rating being BBB- (with a stable outlook), as per the international rating agency, Standard and Poor (S&P), never in history, the Government of India has defaulted on its debt.

Government securities like Central Government bonds, State Government bonds, Treasury bills, State Development Loans (SDLs), Sovereign Gold Bonds (SGB), etc., are the safest forms of investment. The market-related risk, of course, does exist, which, however, could be reduced by holding the securities until maturity. The interest rate/coupon earned on the tenor of a government bond may help you address your liquidity needs. Besides, they are tradeable, providing you with the option to exit in the secondary market.

The RBI vide the ‘Retail Direct Scheme’ has offered retail investors the opportunity to invest in the Indian government securities or bonds. All you are required to open and maintain a ‘Retail Direct Gilt Account’ (RDG Account). This account can be opened through an ‘Online portal’ created specifically for the ‘RBI Retail Direct’ scheme. There are no fees to open and maintain the RDG Account with RBI.

Once the RDG Account is opened, you can participate both, in primary auctions in small lots (say Rs 10,000) as well as transact in the secondary market. In the secondary market, the orders need to be placed on Negotiated Dealing System-Order Matching system (NDS-OM), which is a screen-based electronic anonymous order matching system for secondary market trading in government securities owned by the RBI. All you require to pay is the nominal payment gateway fee while trading in G-secs.

Some of the key benefits of investing in government securities or bonds are that the risk of default is almost nil, protects capital, and is liquid. In your debt allocation, a higher portion may be invested in them, but you ought to have a basic understanding of the functioning of the debt markets. If you feel you do not possess that, then consider investing in G-sec Funds, Debt ETFs investing in G-secs, Banking & PSU debt funds, and/or pure Liquid Funds.

The tax implications:

The coupon/interest earned from government bonds is taxable (under ‘Income from the Other Sources’) as per your income tax slab unless it’s a tax-free bond.

Speaking of the capital gains, if you remain invested in bonds for more than 3 years, it could prove more tax-efficient particularly when you are in the highest income tax slab. The Long-Term Capital Gains (holding period of more than 3 years) is taxed @ 20% with indexation benefit.

On the other hand, if the holding period is less than 3 years, classified as short term, then the Short-Term Capital Gain will be taxed as per your income-tax slab. So, when you are selling, corporate bonds or government bonds, care must also be taken whereby the tax impact is minimised.

The Mutual Fund Route for better diversification and active risk management

If you find investing in corporate bonds a complex task or are commencing your investment journey or simply do not have time to track the interest rates, you can consider Debt Funds as a crucial part of your portfolio. Instead of direct investment in Government securities or corporate bonds, the mutual fund route could offer you optimal diversification plus better liquidity with a professional fund manager doing the job of selecting the best securities for you.

A Debt Fund invests in fixed-interest generating securities such as corporate bonds, government securities, treasury bills, commercial paper, and other money market instruments.

You should consider investing in a short-term debt and liquid fund portfolio where you can put your surplus money to build an emergency fund. Given their short duration, these funds take low interest rate risk.

You can also consider Dynamic Bond Funds for a longer investment tenure that invest in corporate bonds and Government bonds. Dynamic bond funds are a type of debt fund that invest across duration and have different average maturity periods as these funds take investment decisions based on interest rates and invest in instruments of longer as well as shorter maturities.

Therefore, before beginning your investment journey in debt mutual funds, ensure your suitability and evaluate the safely managed Debt Funds that can help you earn risk adjusted returns at lower credit risk, interest rate risk and liquidity risks. When investing in bonds or debt funds, do not assume all are 100% safe. Do your research. Choose bonds and debt funds that carry the least risk while wealth preservation is the objective along with modest capital appreciation.

Remember, sensible investing is pivotal to your long-term financial wellbeing.

Happy Investing!

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual fund investments are subject to market risks read all scheme related documents carefully.