Hi, this is my first post on trading q&a, apologies if this is too theoretical for this forum. If you look at NIFTY option chain on NSE website, you can spot that call and put options of same strikes have different IV values(see attached image). This is bit bizarre from my theoretical understanding, which suggests at same strike IVs should be same for calls and puts, if they are not arb opportunity exists through put-call parity. I will be surprised if arb opportunity exist at such high volumes. Could it be that NSE vol computation is wrong, which would be equally surprising?

On @Sensibull I find one IV for same strikes calls and puts, which seems to be the average of NSE values, is my understanding correct?

[optionchain]

Hey Piyush!

Check out this video by Sensibull which gives the answer to your question.

To summarize, its mostly because there are more market participants who lose money when the market falls hence there are more put buyers resultantly driving put prices ( or simply put -demand and supply).

All credits to Sensibull.

Thanks Hemant. I understood the skew argument, which works for puts and calls equidistance from the spot. However for the same strike options IVs should be same i.e. to say the vol curve theoretically is same for calls and puts. Here is a snippet from Hull that explains the concept:

volsmile_1|600x350

I don’t think (not verified) arb opportunities would exist considering the bid-ask spread also if it does the gains would be lower than the cost involved like brokerage, STT etc.

I don’t think the NSE IVs would be incorrect. The system calculates IV based on LTP and considers interest rate of 10% (see notes below the option chain). My point is IV is an output and LTP is the input. LTP is based on demand and supply so puts being in higher demand are priced higher as a result giving a higher IV to justify the price.

I took a screenshot from a Sensibull video which answers your question.

All credits to Sensibull. I beg your pardon @Sensibull if I have broken any laws by posting this image. I would be more than happy to take it down immediately if required by you. The URL of the above video is https://www.youtube.com/watch?v=ayeeICl2IdY

I hope this answers your question.

1 Like

Thanks Hemant for the link. It seems, as explained in the video, that ITM pricing and hence IV is unreliable due to wider bid ask spreads (lack of liquidity) and this STT factor as well. Also, possibly LTP may differ significantly from bid-ask prices in case of illiquid contracts.

Another point, if you could explain, why is @Sensibull using futures and not spot price to compute ATM strike. It can cause a difference at start of month when futures will trade at premium to spot.

Hi Piyush!

I am sorry, I do not know that. Also, can you please tell the name of the book from which you sent images.

No worries, thanks for the help. This is the book I referred to:

Options, Future & Other Derivatives

Theoretically it might be possible. But implementation cost will set off any arbitrage gain.

Take futures for example. Theoretically futures should trade at spot plus interest rate for the period to expiry. But it won’t be the same. So if you try to explore this opportunity you will end up in loss more often than not. Transaction cost is totally ignored in Theoretical prices. Same applies to Put call parity theory.

{kind=link}

{kind=link}

{kind=link}

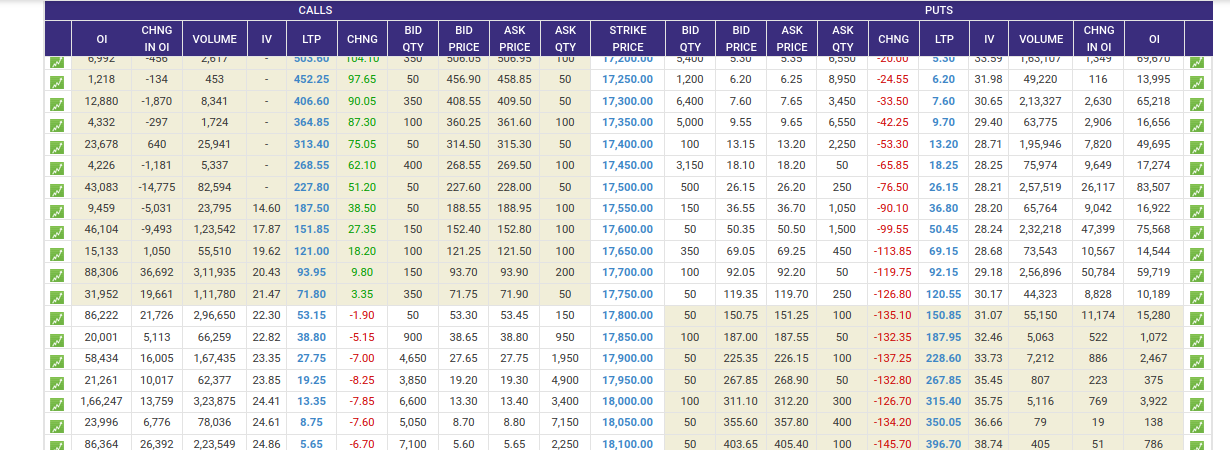

In the above screenshot that I have shared, there is an arbitrage opportunity.

- Sell nfity futures.

- Buy 17500 call.

- Sell 17500 put.

Theoretically you should get net 1.55 points. But if you try exploring this you will end up losing.

1 Like