I don’t think (not verified) arb opportunities would exist considering the bid-ask spread also if it does the gains would be lower than the cost involved like brokerage, STT etc.

I don’t think the NSE IVs would be incorrect. The system calculates IV based on LTP and considers interest rate of 10% (see notes below the option chain). My point is IV is an output and LTP is the input. LTP is based on demand and supply so puts being in higher demand are priced higher as a result giving a higher IV to justify the price.

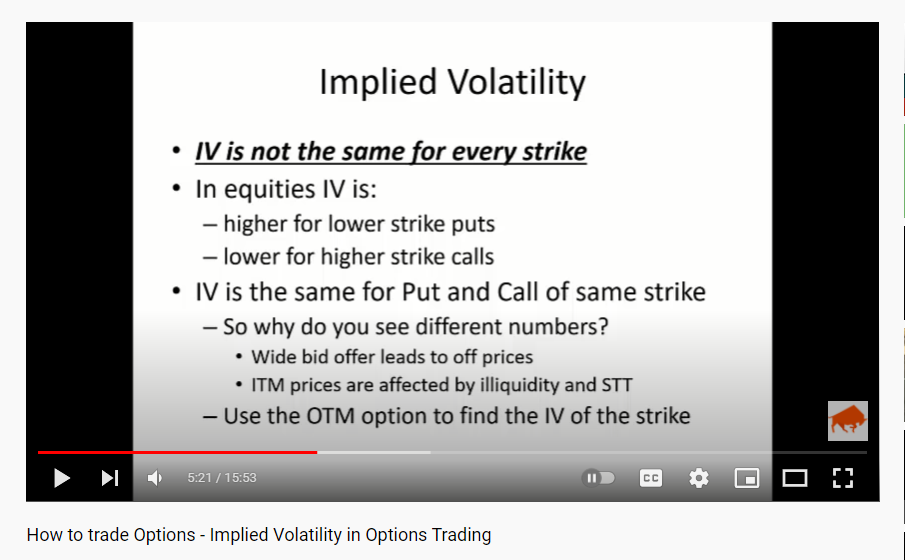

I took a screenshot from a Sensibull video which answers your question.

All credits to Sensibull. I beg your pardon @Sensibull if I have broken any laws by posting this image. I would be more than happy to take it down immediately if required by you. The URL of the above video is https://www.youtube.com/watch?v=ayeeICl2IdY

I hope this answers your question.