Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

Every day, each team member shares something they’ve learned, not limited to finance. It’s our way of trying to be a little less dumb every day. Check it out here

In today’s edition of The Daily Brief:

- Reliance Results: Growth Engines in Action

- World Bank’s Economic Outlook: Gloom & Hope

Reliance Results: Growth Engines in Action

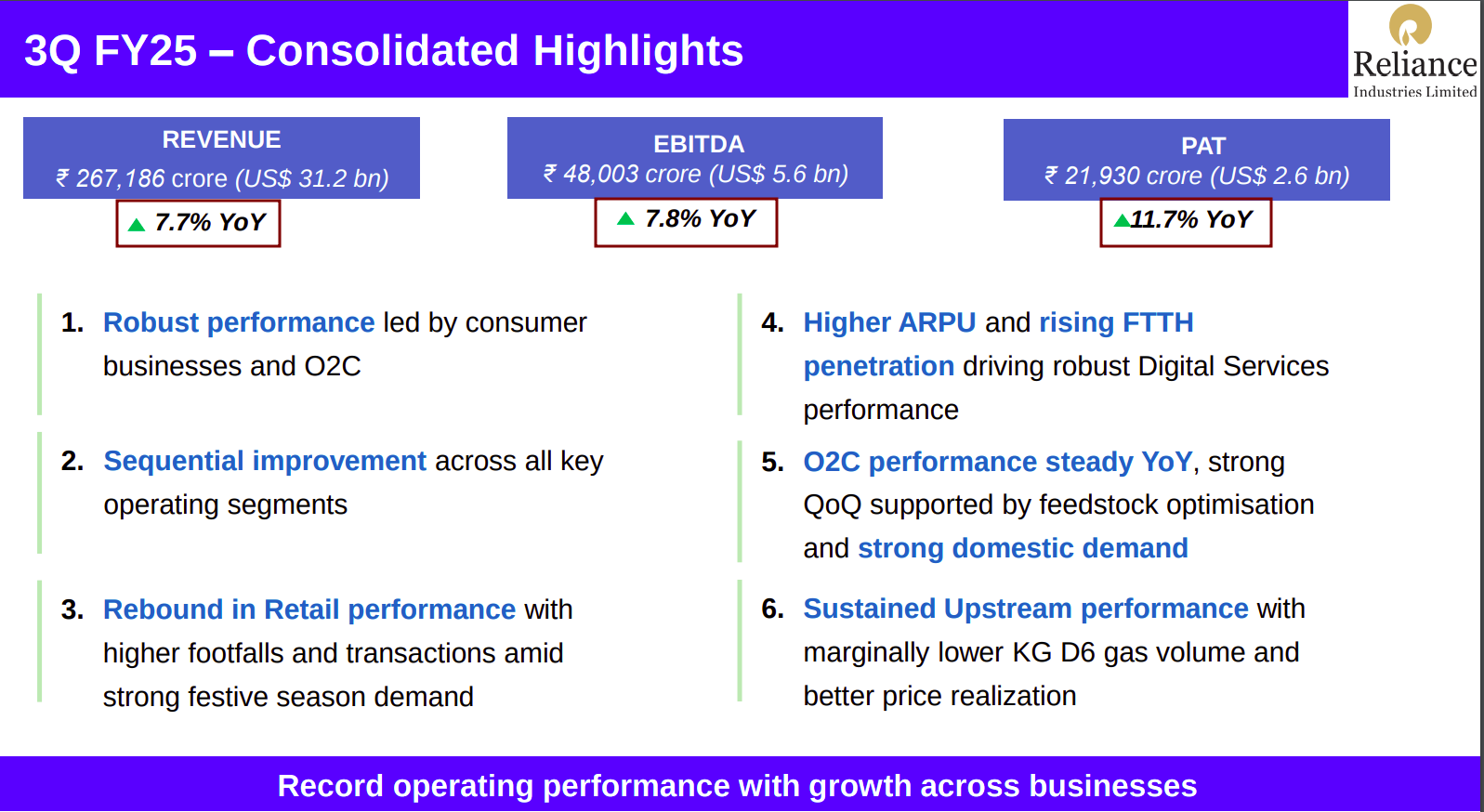

Reliance Industries recently announced its results and social media has been buzzing about how the company “beat” analyst estimates. The highlights? Revenue grew by 8%, EBITDA by nearly 8%, and Profit After Tax (PAT) surged by approximately 12%.

Source: RIL’s Earnings Presentation

Essentially, it performed better than expected, which is one reason being cited for the stock climbing more than 2.65% in a day. While stock price movements and analyst predictions aren’t our focus, the business results of India’s largest company—by any metric—deserve a closer look. And that’s exactly what we’ll be doing today.

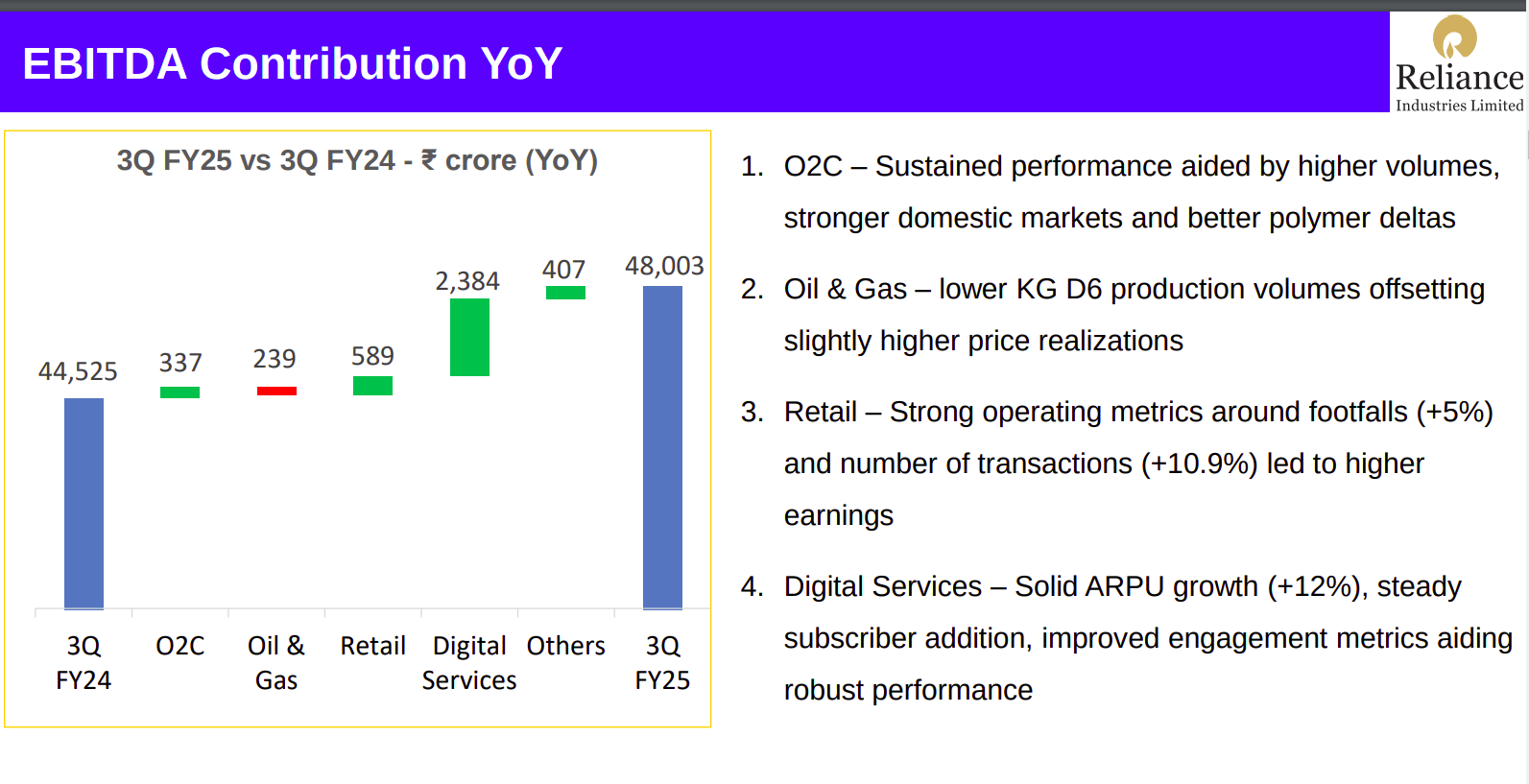

Reliance is a sprawling conglomerate with operations spanning multiple industries, but its results are reported across four key business segments. I’ll walk you through the highlights of each segment, sequenced by their contribution to future profits—from biggest to smallest: Digital Services , Retail , Oil-to-Chemicals (O2C) , and finally, Exploration and Production (E&P) .

To set the stage, out of the additional ₹3,500 crore in operating profit Reliance made this quarter compared to the same period last year, a massive 68% came from Digital Services , followed by 17% from the Retail business .

Source: RIL’s Earnings Presentation

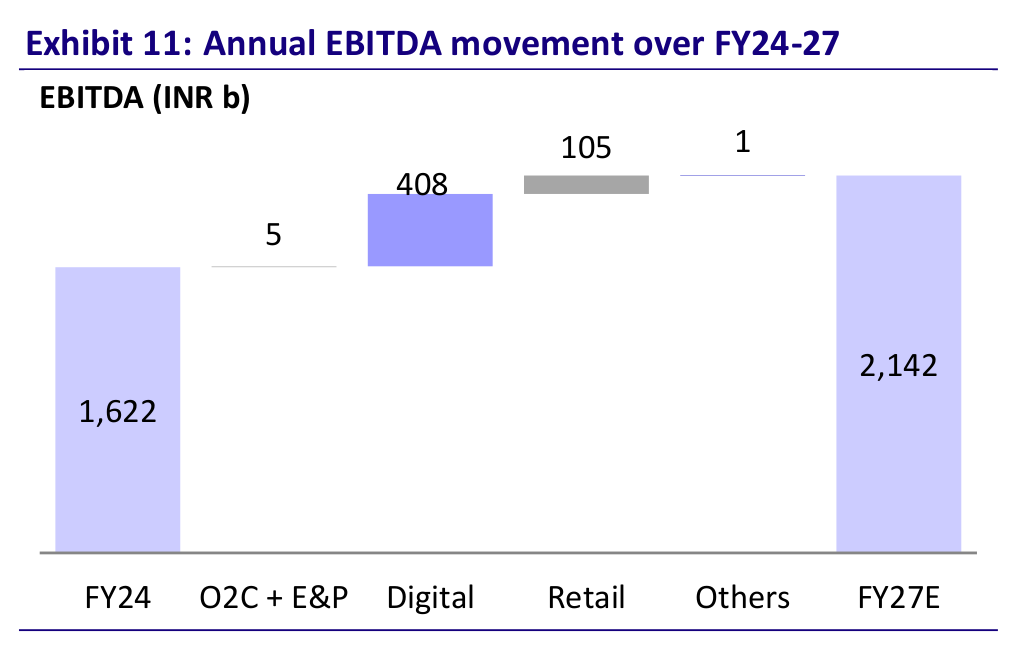

And it’s not just about the current numbers. According to Motilal Oswal, nearly all the incremental operating profit over the next four years (FY24 to FY27) is expected to come from these two segments. Digital Services and Retail represent the company’s growth engines, while the oil businesses (O2C and E&P) are in their maturity phase, providing stable cash flows.

Source: Motilal Oswal

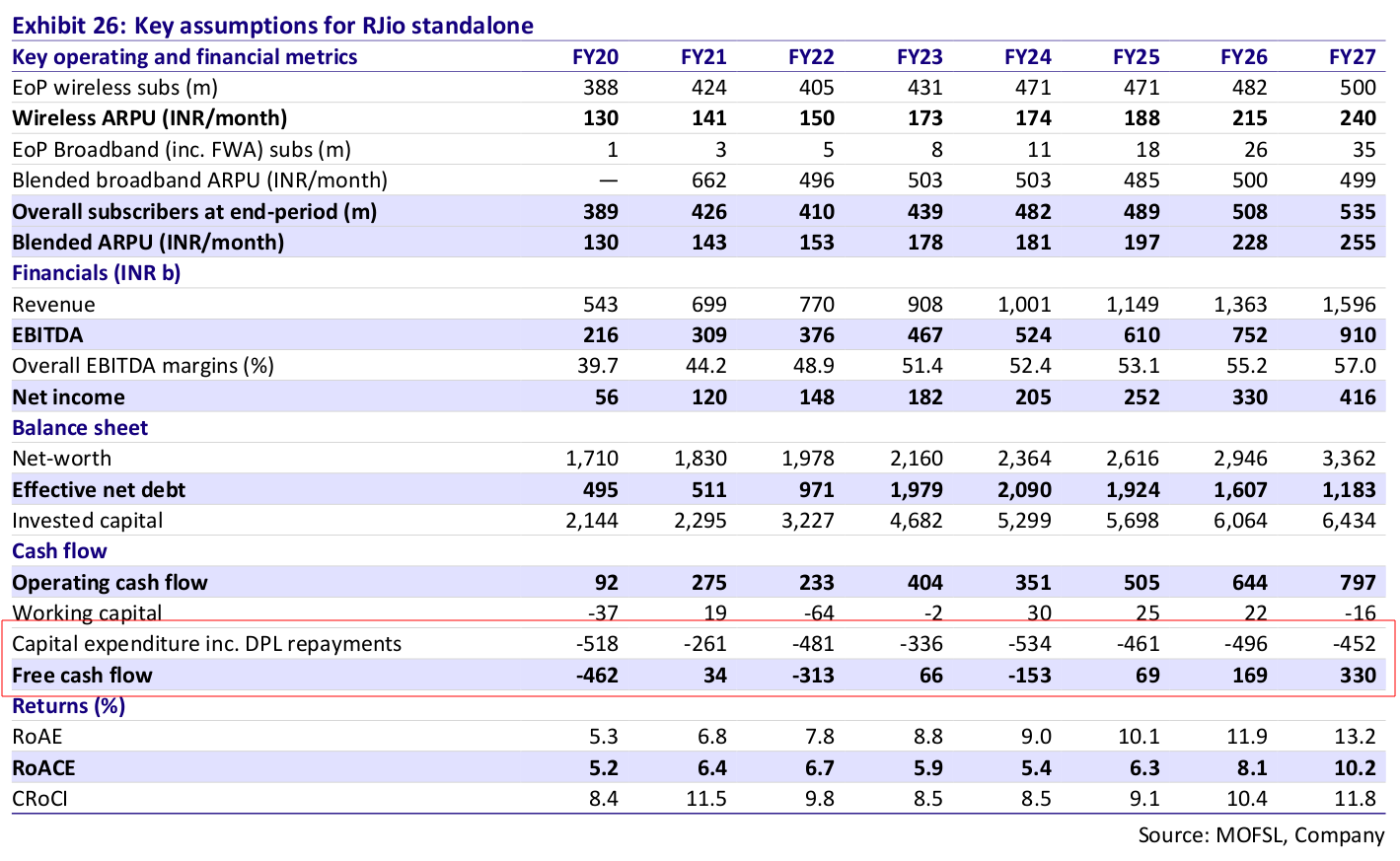

Digital Services

Jio remains the world’s leading Standalone 5G operator (outside China) with a subscriber base of 17 crore. 5G now accounts for ~40% of wireless traffic during the quarter. Jio network continues to attract ~70% of the incremental 5G devices sold in India.

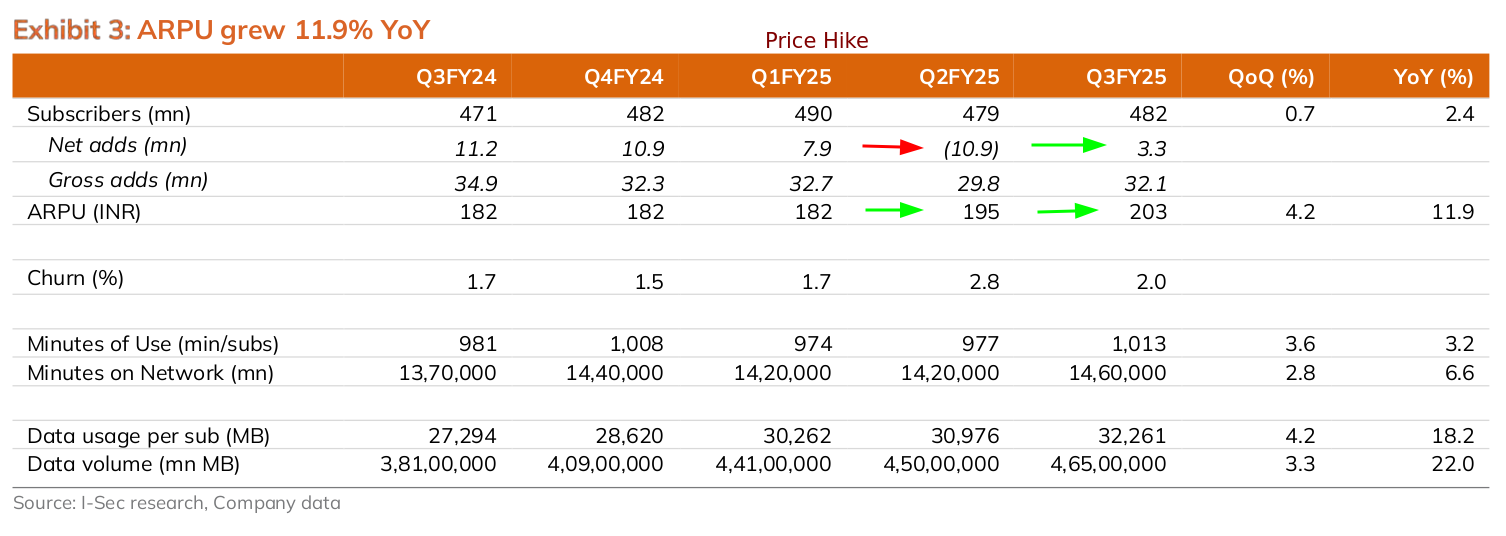

The big story? Price hikes are finally working their magic.

Back in July 2024, Jio raised its tariffs. And now, the impact is starting to show. ARPU, or Average Revenue Per User, has been climbing for two straight quarters after being flat for a while. This is a big win for Jio because ARPU is a key measure of how much money they’re making from each user.

But let’s not forget, it caused some churn—over a crore subscribers left last quarter, with many heading to competitors like BSNL.

But now things are stabilizing. In Q3FY25, they managed to add back 33 lakh subscribers , bouncing back after the previous quarter’s dip. That’s a clear sign that the SIM consolidation phase —you know, people dumping extra SIMs due to higher prices—is behind them.

Jio says the full impact of the tariff hike is still to come . Translation? ARPU could keep climbing. Plus, some analysts are already predicting another tariff hike in FY26, which could further boost revenue. So, on the ARPU front, things are looking pretty solid.

But it’s not all smooth sailing on Jio’s capital expenditure. It’s still high, and their free cash flow , or FCF, isn’t exactly robust. That’s a bit of a red flag. The good news? Capex seems to be slowing. In the first half of FY25, it’s come down compared to the spending frenzy of FY24. Analysts, like those at Motilal Oswal, are even calling this the peak of Jio’s capex cycle . They believe Jio’s spending will taper off as the major 5G and fiber optic (FTTH) rollout winds down.

Source: Motilal Oswal

That said, any capex savings from Jio will likely be offset by Reliance’s new energy investments —think solar, hydrogen, and battery projects. But the takeaway here is clear: the heaviest spending for Jio might be behind them, giving them room to improve their cash flows.

So, to sum it up, Jio’s ARPU is climbing, customers are coming back, and while capex remains a challenge, there are signs that it’s easing up. All eyes are now on how Jio capitalizes on these trends and continues its journey as a key growth driver for Reliance.

Retail

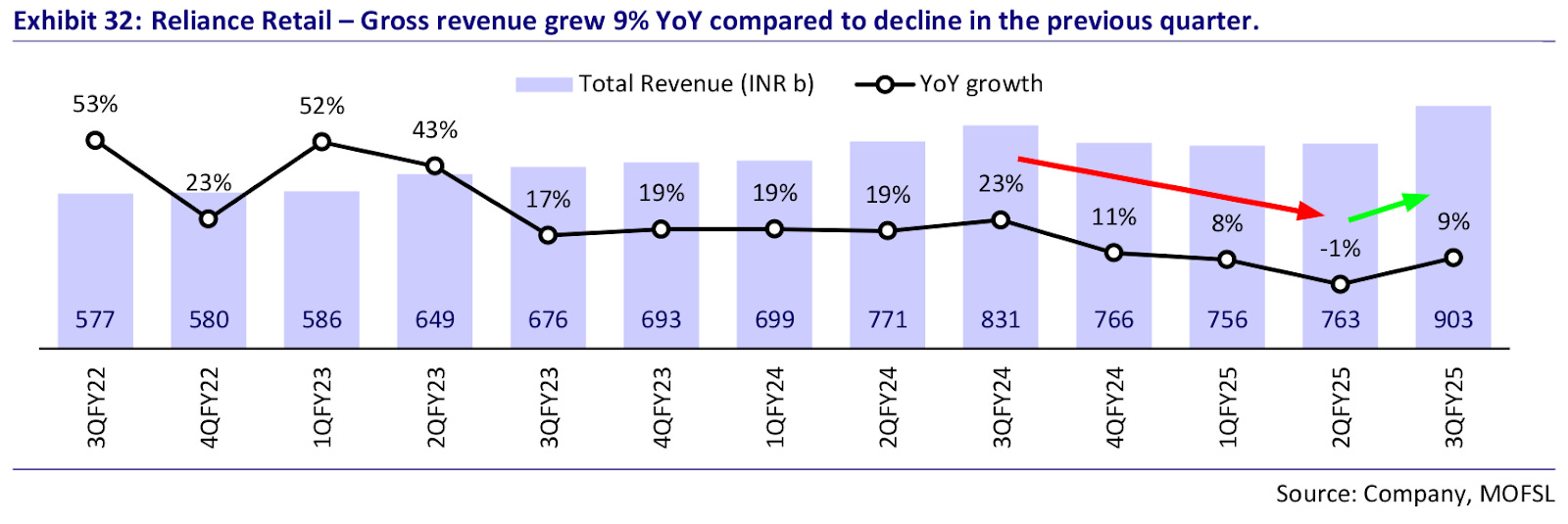

Let’s dive into Reliance’s retail business, which finally saw revenue growth after struggling with slowing growth and even degrowth last quarter . Revenue grew by 8.8% YoY in Q3FY25 , reaching ₹90,333 crore. So, what changed? Reliance attributes this turnaround to productivity improvements and store rationalization .

Source: Motilal Oswal

Productivity improvement means they’ve been doing more with less—streamlining operations, optimizing store layouts, and improving customer engagement. Store rationalization involves closing underperforming stores while focusing on profitable locations. This approach might seem counterintuitive for a growth-driven retail chain, but it’s a smart move for long-term efficiency.

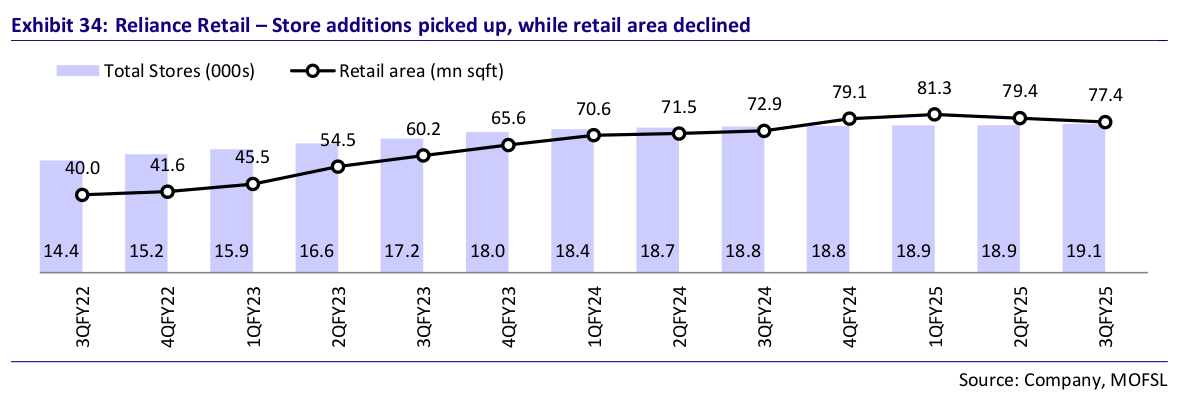

They opened 779 new stores, taking the total count to 19,102, but have been seeing their retail area decrease since the start of the financial year.

Source: Motilal Oswal

Reliance Retail operates across categories—electronics, apparel, grocery , and more. While it doesn’t represent the entire Indian consumption market, its performance gives us valuable hints about broader consumption trends. If Reliance Retail is bouncing back, it might mean consumer sentiment is improving, and spending may be picking up, especially in categories like grocery and apparel.

What really stands out in their retail portfolio is Campa Cola, Reliance’s homegrown brand that has become a key part of their grocery strategy. Acquired in 2022 for just ₹22 crore, the brand has already captured over 10% market share in the sparkling beverage category in select states and is on track to cross ₹1,000 crore in revenue by FY25.

Exploration & Production (E&P)

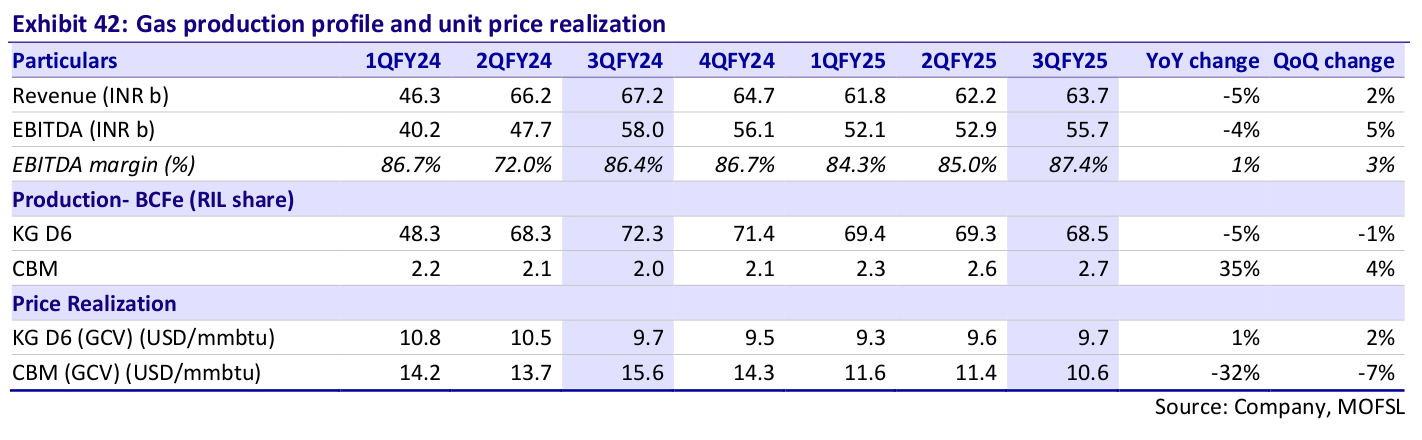

Reliance’s Exploration and Production (E&P) business had a stable quarter, continuing to deliver consistent results. Production from the KG-D6 basin remained steady at 28 million standard cubic meters per day (mmscmd) , with gas price realization slightly improving to $9.74 per mmBtu , compared to $9.66 last year.

Source: Motilal Oswal

While the segment doesn’t contribute a large share of overall revenue, it plays a vital role in supporting Reliance’s downstream operations by providing essential raw materials like natural gas and crude oil.

However, margins in the E&P segment depend heavily on global crude oil and gas prices, which have been volatile. Despite this, the segment saw a 5% quarter-on-quarter growth in EBITDA to ₹5,570 crore, although it was down 4% year-on-year . On the investment front, capex in E&P remained moderate, as the company focuses on maintaining production rather than aggressive expansion. Looking ahead, Reliance might further cut E&P investments as it shifts its focus toward its new energy projects.

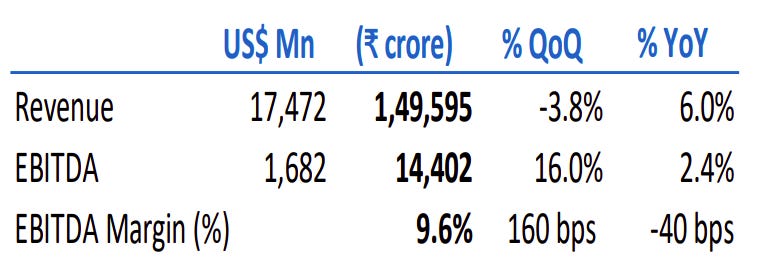

Oil-to-Chemicals (O2C)

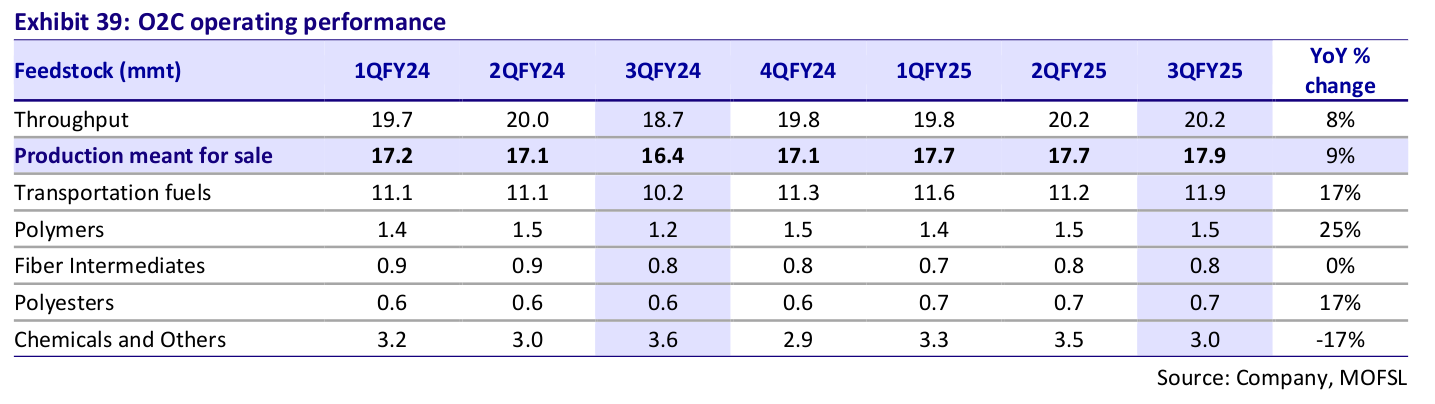

The Oil-to-Chemicals (O2C) business, Reliance’s largest revenue generator, performed well in the third quarter, showcasing its resilience. Revenue grew by 2.4% year-on-year and 16% quarter-on-quarter , driven by stronger refining margins and higher crude processing volumes. Reliance processed a record 17.9 million metric tonnes (mmt) of crude, which is a 9.1% increase from last year , thanks to strong domestic demand.

It was great to see the demand for transportation fuels growing by 17% year-on-year. Higher demand for transportation fuels is typically linked to increased economic activity. This is another sign of relief we see from Reliance’s result.

Source: RIL’s Earnings Presentation

Source: Motilal Oswal

That said, margins were a mixed bag. The EBITDA per tonne declined by 7.5% year-on-year to $95 due to weaker margins in the petrochemical and polyester segments. However, compared to the previous quarter, margins saw a 14% improvement , supported by better refining cracks for products like gasoil and jet fuel.

Reliance has been investing heavily in modernizing its O2C operations, focusing on efficiency and sustainability. While capex in this segment remains high, there are signs that it is starting to moderate. Importantly, a portion of the investment is now being directed toward green energy initiatives, such as carbon capture and hydrogen production, as Reliance prepares for a low-carbon future.

Reliance’s results don’t pack any big surprises, but they do reaffirm the narrative: Digital Services and Retail are living up to their roles as the key growth drivers, while the legacy oil business continues to hold its ground with steady performance. If there’s a segment where we might see more excitement, it’s Reliance’s new energy ventures, where they’ve committed a massive $10 billion investment. However, this is a long-gestation business, and looking at it through a quarterly lens doesn’t fully capture the progress or potential here. For now, Digital and Retail remain the stars of the show.

World Bank’s Economic Outlook: Gloom & Hope

We’ve spent the last week poring over the World Bank’s massive Global Economic Prospects report - all 250 pages of it - so you don’t have to. We’ve extracted the most fascinating insights about where the global economy is headed, with a special focus on South Asia. This is a story worth understanding.

Part 1: The Gloomy Global Economy

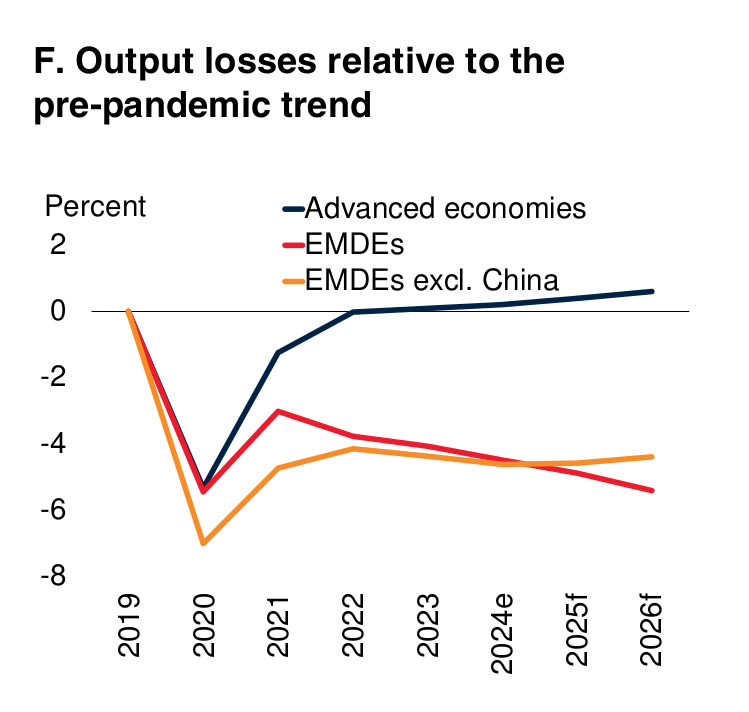

The global economy has hit what economists are calling an inflection point, and the numbers tell a sobering story. We’re looking at global growth stabilizing at 2.7% for 2025 and 2026. Now, that might not sound terrible, but here’s the crucial context: it’s significantly below the 3.1% average we saw in the pre-pandemic decade, and this isn’t just a temporary dip - we’re seeing structural changes that suggest this could be our new normal.

Source: World Bank

Let us paint a picture of what’s happening on the ground. Global trade, which has always been a key driver of growth, is facing significant challenges. This is affecting businesses, reducing opportunities, and having a real impact on people’s everyday lives.

Source: World Bank

Here’s where it gets worrying—we’re seeing what experts call “trade fragmentation.” In 2023, global trade restrictions reached their highest level since records began in 2009. And it’s no longer just about tariffs. It now includes export controls, investment restrictions, and complicated regulatory hurdles.

Take the semiconductor industry, for example. There’s been a major shift in how companies decide where to produce and invest. Instead of focusing purely on economic efficiency, many are now making decisions based on geopolitical factors. This is reshaping global supply chains in a big way.

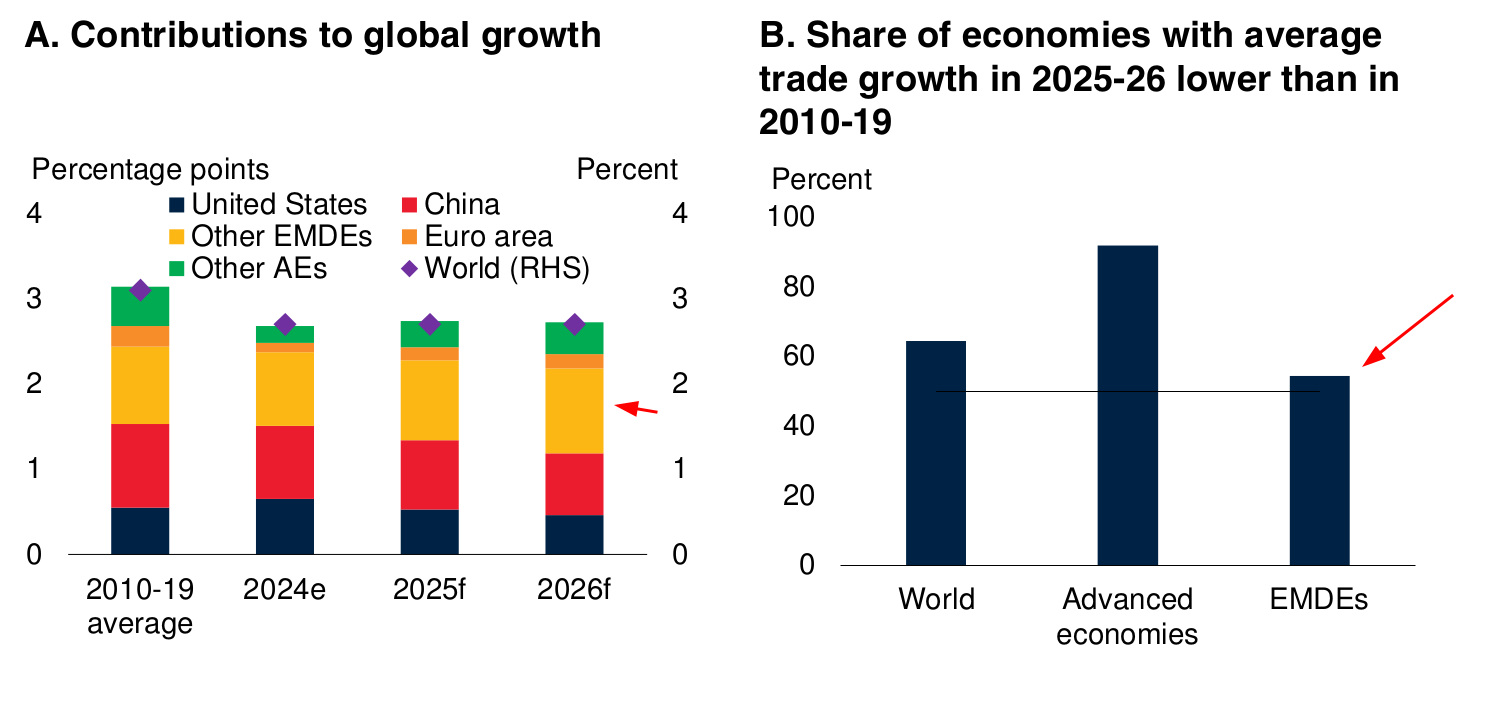

Now, let’s look at the potential impact of changes in U.S. trade policies. Our analysis shows that a 10% increase in U.S. tariffs could reduce global growth by 0.2 percentage points. If other countries retaliate—which history suggests is likely—that impact could grow to 0.3 percentage points. To put this into perspective, that’s roughly the same as wiping out the entire annual economic output of a country like New Zealand.

And here’s something that doesn’t get talked about enough: the services trade. While most attention is on goods, services trade has actually been growing faster since the early 2010s. Today, services make up 24% of global trade, which is fundamentally changing how economies grow and respond to global challenges.

The combination of higher interest rates and slower growth poses significant challenges, especially for developing economies.

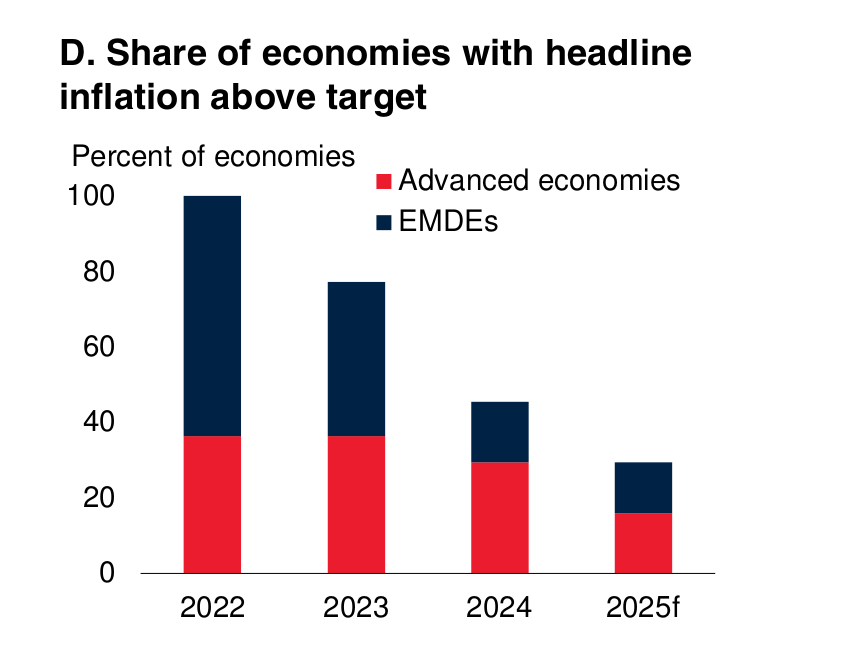

Now, let’s talk about monetary policy because it’s a key piece of the puzzle. But first, a quick look at inflation. By late 2024, headline inflation was at or below target in over 60% of economies, and in most other places, it was only slightly above target.

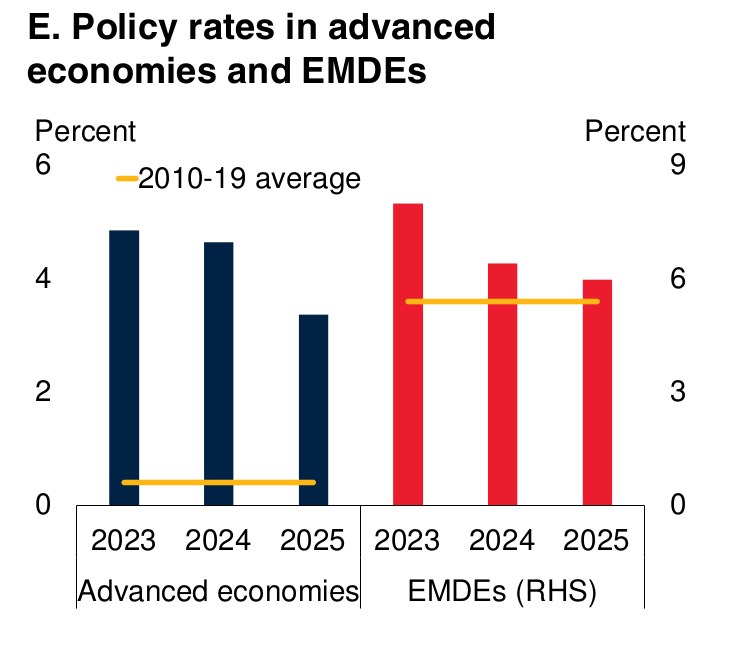

Policy rates in advanced economies are expected to come down in 2025. However—and this is important—they’ll still be much higher than the unusually low levels we saw in the 2010s. While inflation has been declining in most advanced economies and Emerging market and developing economies (EMDEs), strong economic growth and rising wages could lead to global inflation staying higher than expected. If that happens, central banks in both advanced economies and EMDEs might keep interest rates high for longer, which could slow down economic activity in EMDE regions.

In EMDEs, nearly 70% of countries are expected to experience slower trade growth in 2025–26 compared to their average from 2010–19. This mix of higher interest rates and slower growth creates serious challenges for developing economies.

Part 2: The Rise of EMDEs

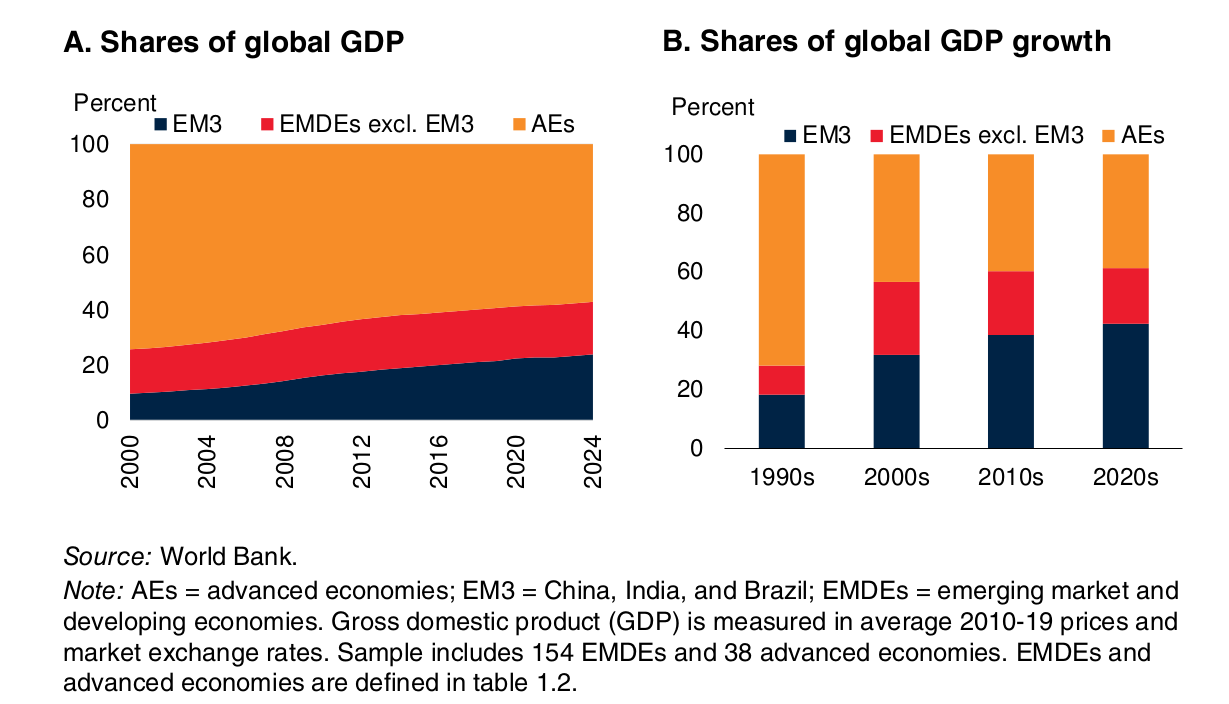

Now, here’s where our story takes a fascinating turn. While developed economies have been struggling, emerging market and developing economies - or EMDEs - have been rewriting the rules of the global economy.

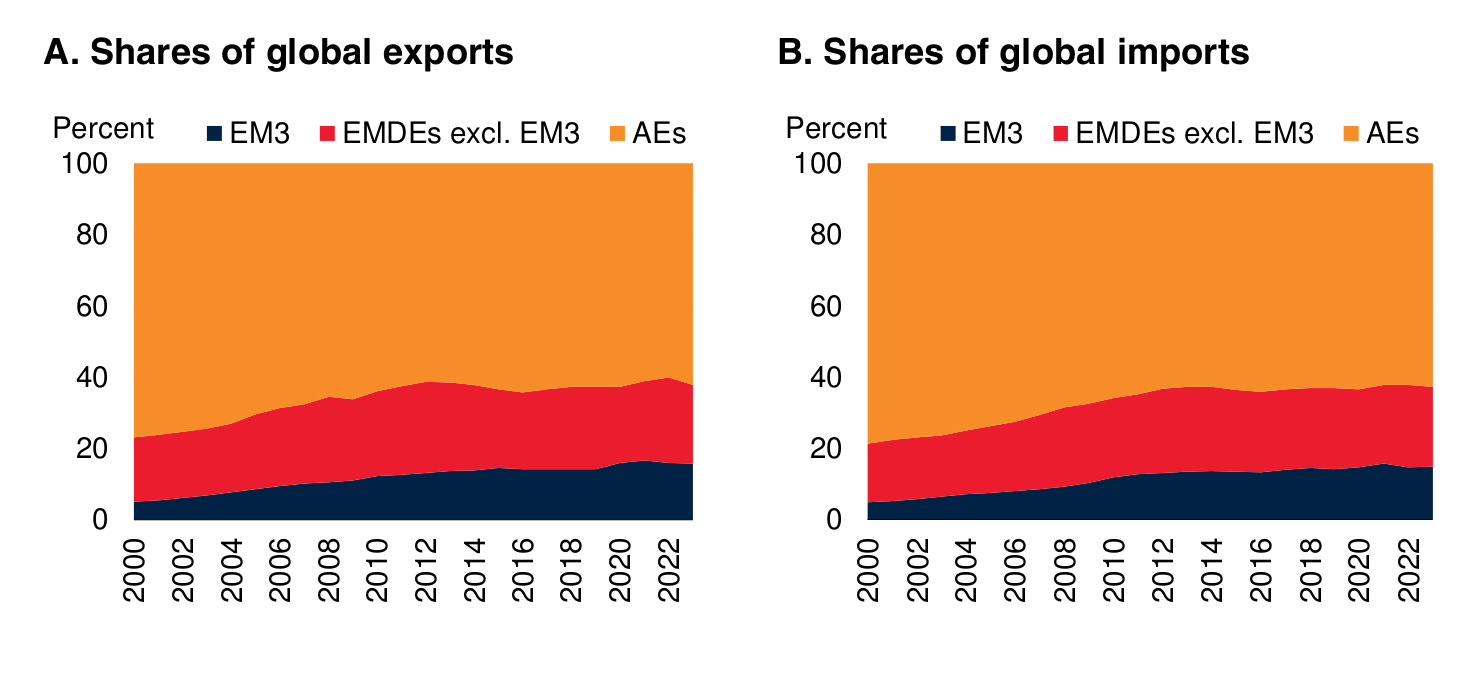

The numbers are staggering. EMDEs now account for 45% of global GDP, up from 25% in 2000. They’re responsible for 60% of annual global growth, double their contribution from the 1990s. They are also home to 85% of the world’s population. And here’s a stat that really drives home the shift: EMDEs received 21% of global capital inflows during 2019-2023, compared to just 6% in 2000-2004.

Source: World Bank

The real game-changers have been what we call the EM3 - China, India, and Brazil. Together, they now produce about 25% of global GDP, up from 10% in 2000. Just think about that - in just over two decades, these three countries have more than doubled their share of the global economy.

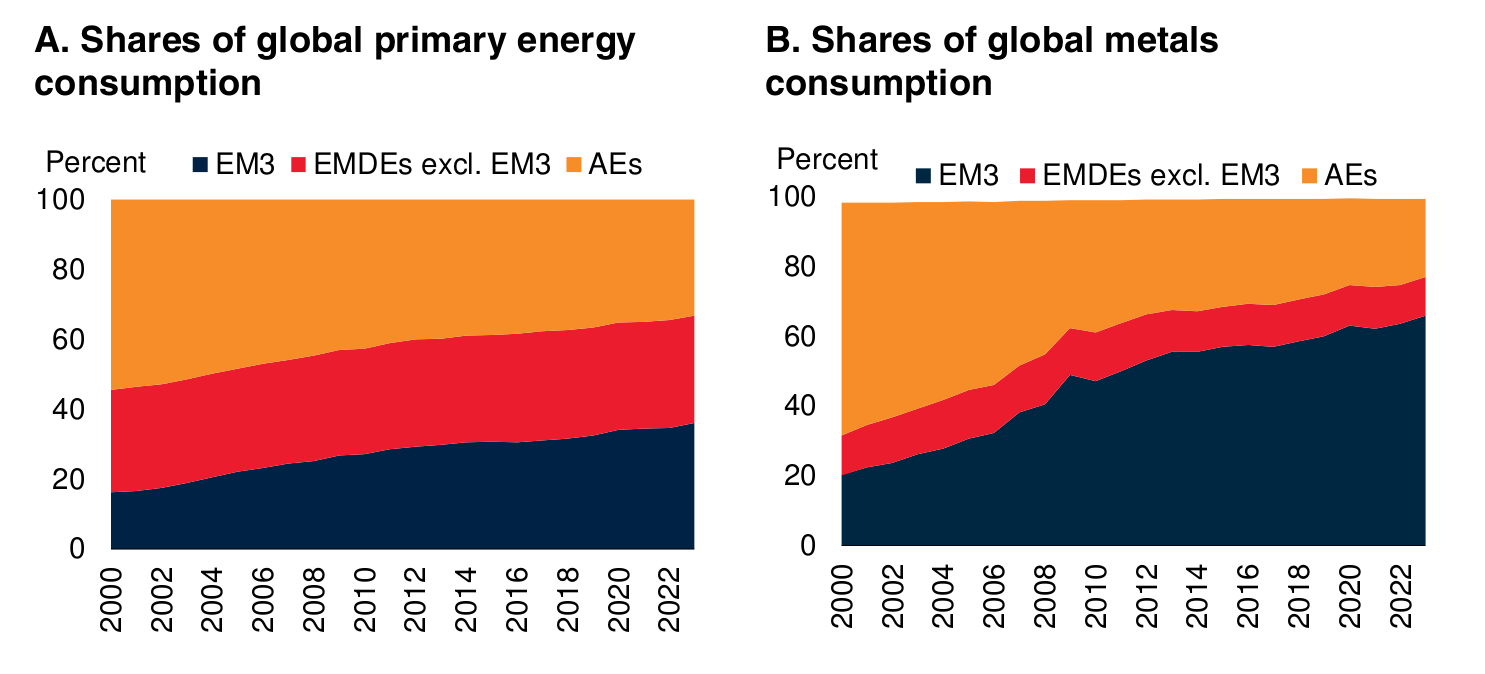

Here’s something fascinating about these emerging economies - they’re becoming increasingly important in global commodity markets. EMDEs have outstripped advanced economies in demand for primary energy since 2004 and for metals since 2007. China alone now accounts for 60% of global metals demand, up from just 13% in 2000.

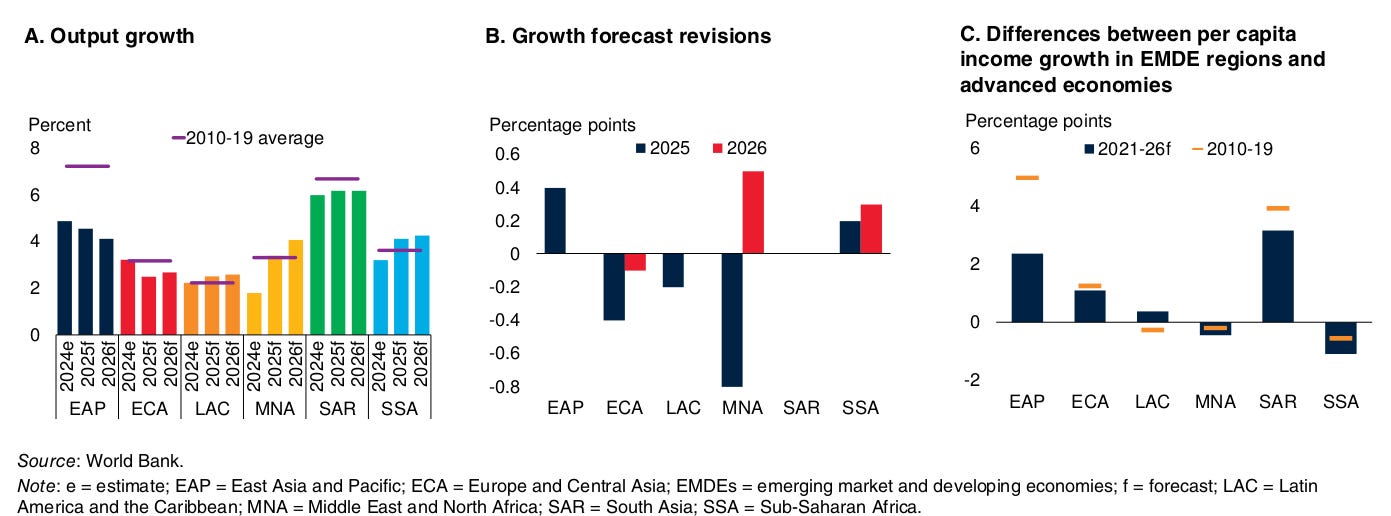

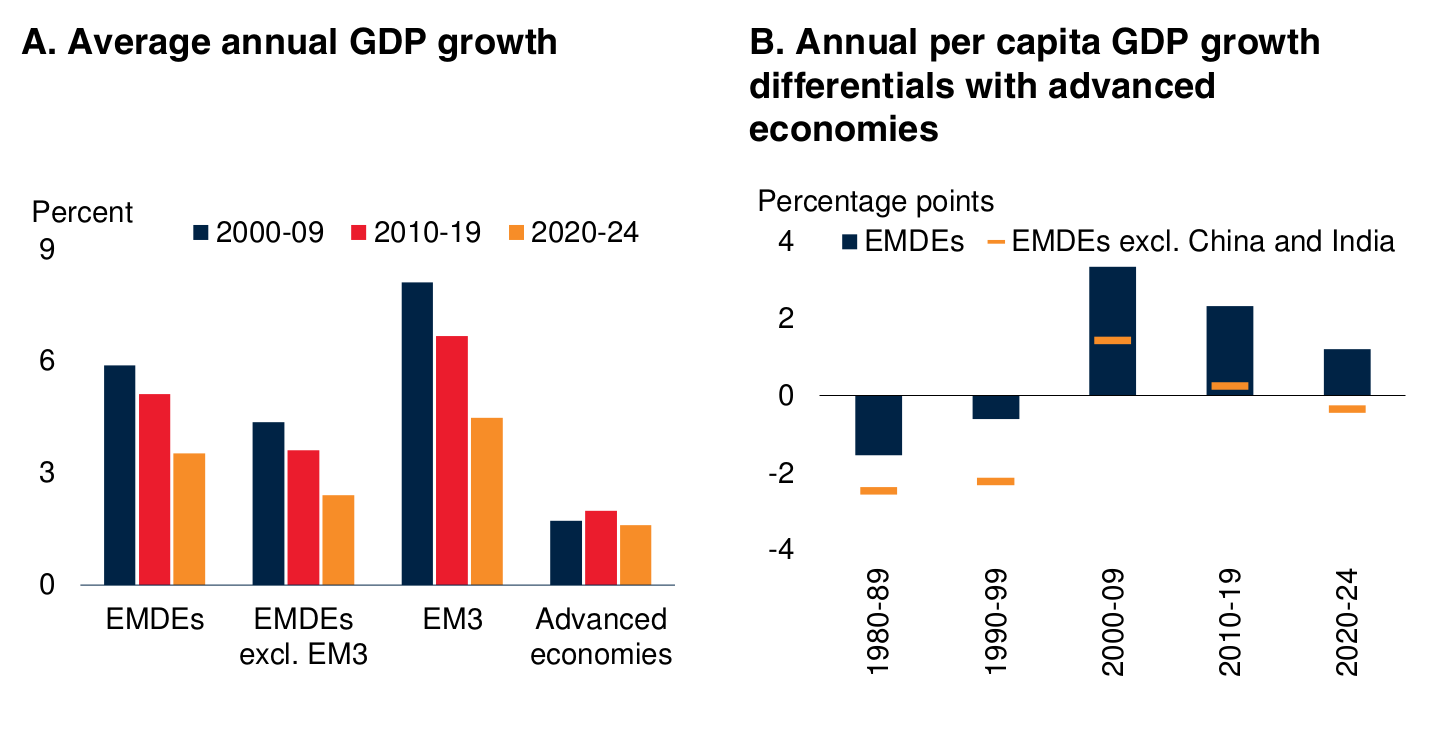

But - and this is crucial - EMDEs are facing their own perfect storm of challenges. Growth has slowed dramatically, from 5.9% in the 2000s to 3.5% during 2020-24. As of 2025, they are facing the lowest five-year-ahead potential growth rate since 2000.

They’re facing rising debt levels—government debt reached 70% of GDP in 2024, the highest since records began in 1970. A big part of this stems from the spending required to prevent their economies from sliding into a depression during COVID-19. But it’s not just about how much they owe—it’s also about who they owe it to. The creditor landscape has become much more complicated, with China now the largest single bilateral creditor to other EMDEs.

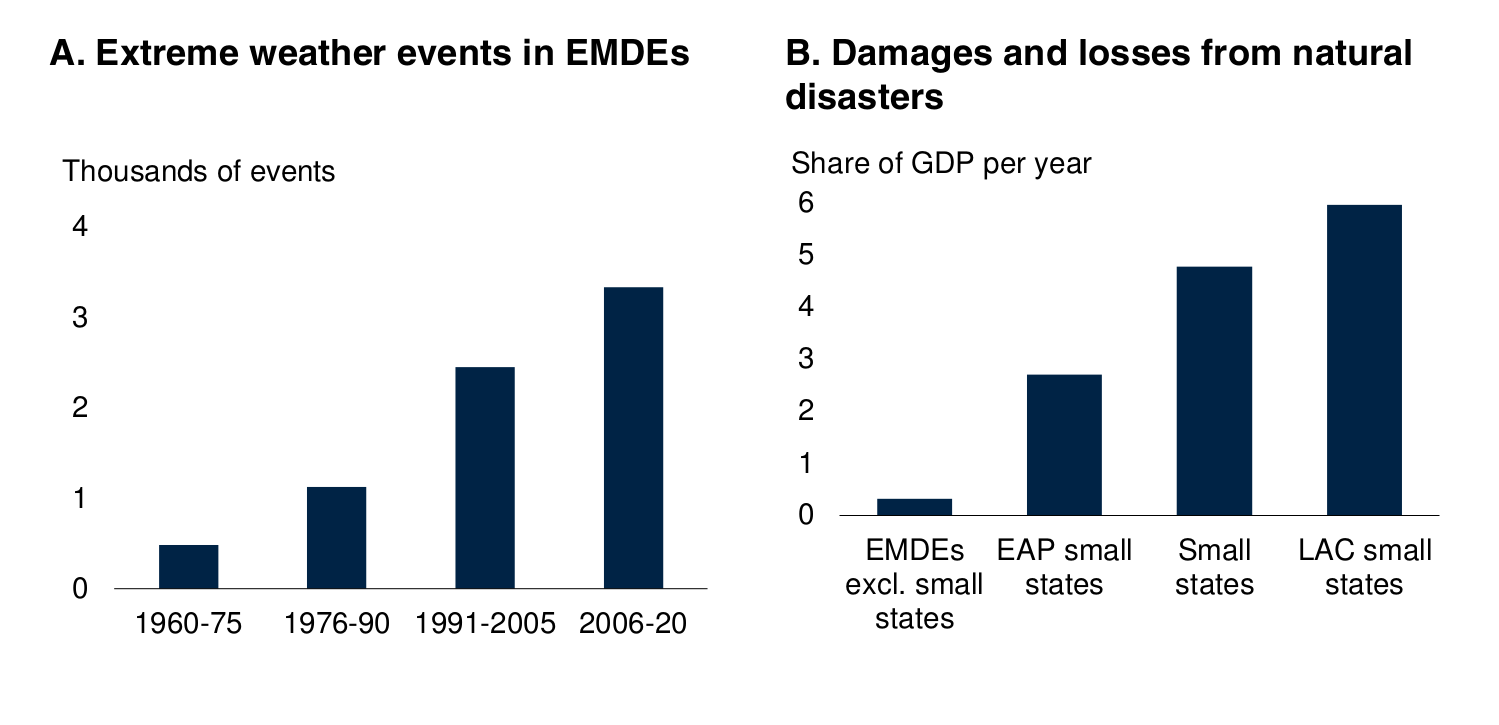

Climate change poses an existential threat. Climate-related disasters have become more frequent and costly and are putting an immense strain on governments that are already dealing with historic debt burdens.

Estimates suggest that climate change could push over 130 million people into extreme poverty by 2030. And these countries are increasingly interconnected - almost half of their exports now go to other EMDEs, compared to just one-quarter in 2000.

Part 3: Growth Outlook

Let’s take a closer look at the two giants reshaping the global economy—China and India. Their paths couldn’t be more different, but both are key to understanding where the world economy is headed.

China is going through what economists call a “managed slowdown.” Growth is expected to slow to 4.5% in 2025 and 4% in 2026. But this isn’t just about numbers. China is facing major challenges—a property sector in crisis, an aging population that’s creating demographic pressures, and the need to shift from an investment-driven economy to one focused on consumption.

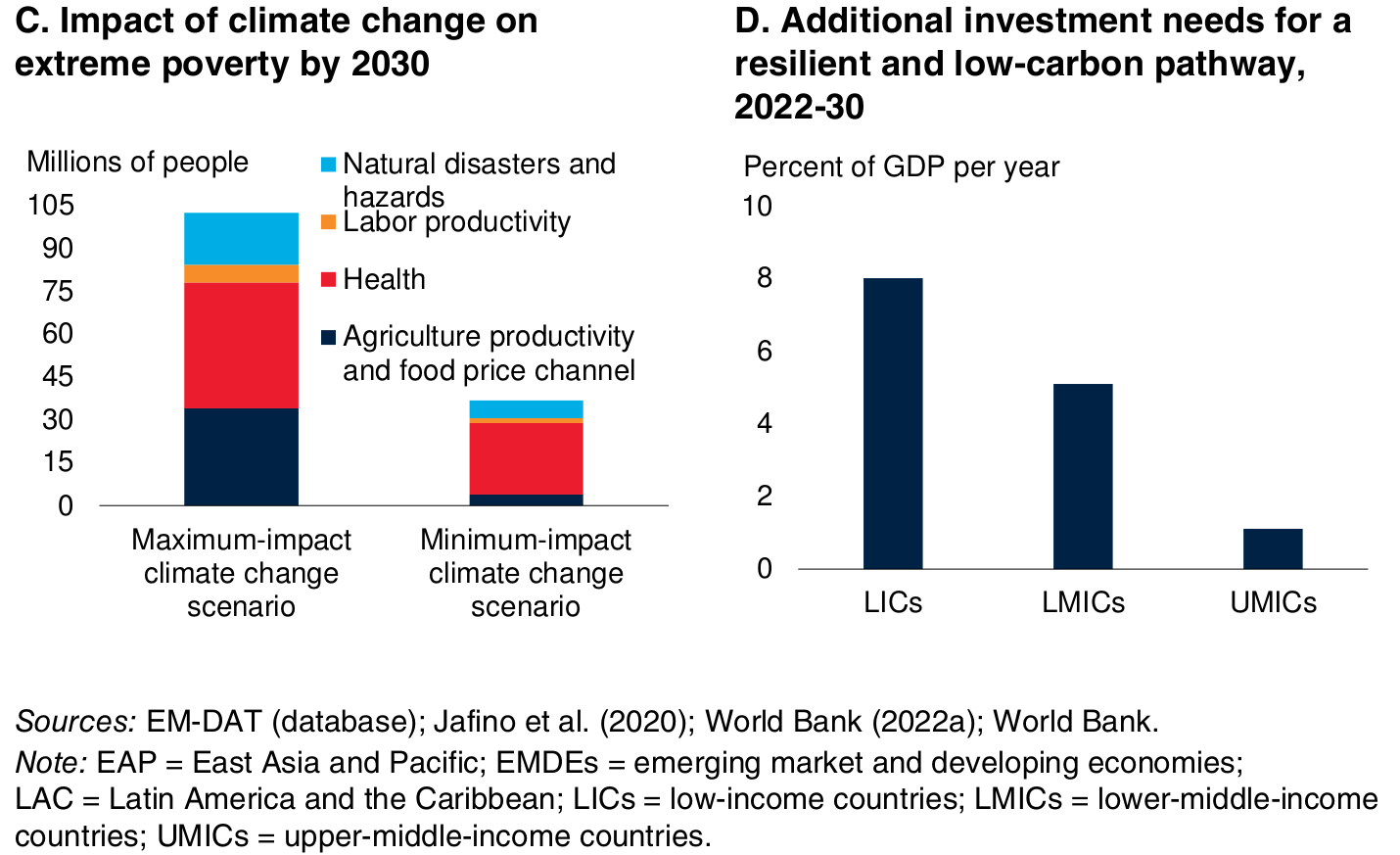

To put this in perspective: when China sneezes, does the world still catch a cold? According to the World Bank, a 1-percentage-point increase in China’s growth boosts other emerging markets’ output by a cumulative 1.8% over three years. Interestingly, a similar boost from the United States has an even greater impact, leading to a 2.9% expansion in other emerging markets.

This shows that while China’s role in the global economy has grown significantly, the U.S. remains the key driver of global economic cycles. However, if growth slows in either China or the U.S., the entire global economy will feel the impact.

India, on the other hand, is emerging as a new engine of growth. With projected growth of 6.7% in both 2025 and 2026, it’s set to remain the world’s fastest-growing major economy. What’s fueling this growth? A mix of factors: a booming services sector, improved manufacturing activity driven by government initiatives, and strong private consumption supported by a healthier labor market.

But it’s not all smooth sailing. Higher inflation and slower credit growth have hurt consumption, particularly in urban areas. Another challenge for India’s economy is weak investment and sluggish manufacturing growth. Many companies don’t see the need to invest, and this comes at a time when government spending—both at the national and state levels—has also remained subdued.

The bright spot, however, is the rural economy, which is showing signs of revival thanks to a good monsoon season.

Source: World Bank

But India’s story has another crucial dimension - the demographic dividend. While China’s working-age population is shrinking, India’s is expanding. By 2050, this demographic difference could be a game-changer for global economic dynamics.

Conclusion

As we wrap up today’s brief, let’s take a step back and look at the bigger picture. We’re not just seeing economic shifts—we’re witnessing a fundamental reordering of the global system. These changes are transforming everything, from global institutions to technological leadership and cultural influence.

Yes, there are significant challenges—rising debt, climate change, and geopolitical tensions. But there are also incredible opportunities. The rise of EMDEs isn’t just about a shift in economic power; it’s about the creation of new markets, groundbreaking innovations, and fresh approaches to doing business.

Tidbits

- Torrent Power will invest ₹18,000 crore in a modern thermal plant in Madhya Pradesh, creating over 7,000 jobs and strengthening the state’s energy infrastructure. This forms part of ₹32,520 crore investments aimed at transforming the region into an industrial hub.

- India’s palm oil imports are expected to hit a five-year low in January 2025, declining to 340,000-370,000 tons due to negative refining margins and premium pricing over soy oil. Refiners are turning to alternatives like soy and sunflower oil, reshaping trade flows.

- Suzuki plans a $4 billion investment in India to double production capacity to 4 million EVs annually by 2031. With the e-Vitara launch, Maruti Suzuki aims to support India’s 30% EV penetration goal while exporting to markets like Japan and Europe.

-This edition of the newsletter was written by Kashish and Bhuvan

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.