While the centuries of evolution

might have optimized the human-brain to quickly catch a tiger (or a snake) within a mass of bushes.

It is evident at this point that nothing has prepared us to accurately intuit at numerical extremes.

Consider these 2 events,

Event A - 99% unlikely to occur.

Event B - 99.9% unlikely to occur.

It is not immediately evident that

one of the events is 10x more likely to occur than the other.

After Friday’s market close in the US,

Moody’s announced that it had downgraded the U.S. credit rating from AAA to AA1

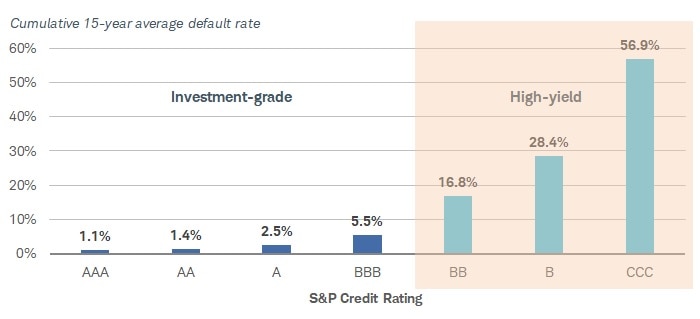

One way to understand what this credit-rating downgrade means in numerical terms,

is to look at actual incidences of defaults over the years, grouped by credit-rating.

AA rated bonds have defaulted ~25% more often (1.4%) than a AAA rated bond (1.1%).

Data from Standard & Poor’s 2022 U.S. Corporate Default Study, as of 6/13/2023.

The 15-year cumulative average default rate is calculated by weight-averaging the marginal default rates in all static pools.

Dont you think it is a good thing that retail investor are buying when there is a dip. We are talking about S&P500 stocks. 52 week high was 6,147 and low was 4,835. Now it is 5,939. Investors will defenetely buy any dip as things are clearing up.

When it fell to 5,062 on first week of April, someone must have bought what was sold. I am sure the buyers are the real investors. Same thing happened in India during corona. People whether FOMO or whatever did buy after that, and still made huge amounts of money as index peaked to 26000 or so (from the low of 7,500 approx. whoever bought thinking FOMO at 16K or 17K or 18K still made lots of money - provided they know when to sell as well)

Moodys did the same with India, long time back, they reduced India Sovereign rating BAA3 during corona time. This was the lowest in the last 22 years. Imagine, India’s Sovereign Rating not any index or anything. What value will you give to them, when India has not every defaulted on its dues ever. I remember, India even pledged gold and took loan from IMF. India issued India Melineium Bond in usd from NRI where interest was given at 8.5% or so. It got oversubsubscribed. This is our strenght and moody downgrades???. IMF took gold as security whilst NRIs based on the sovereign guarantee subscribed for the bond.

IMHO, it was a sign of weakness not strength.

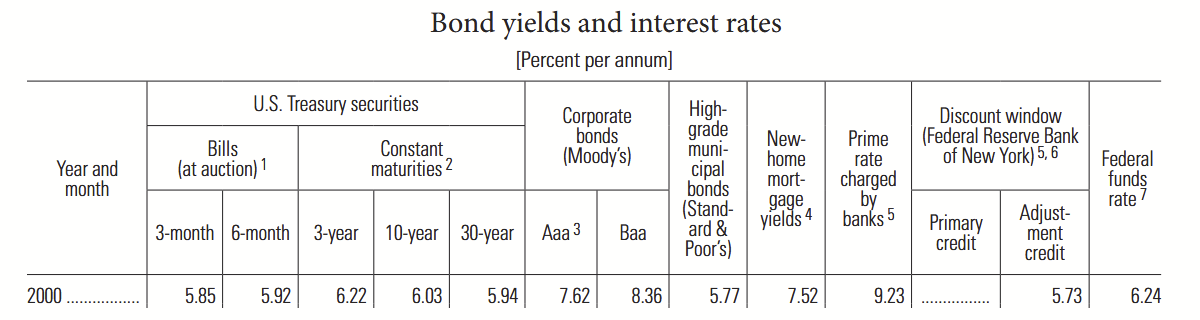

In a period of low-interest rates globally,

India had to offer 8.5% Dollar-denominated returns and ~7% Euro-denominated returns to attract investment.

That is just one aspect of credit-worthiness.

The credit rating for sovereigns also accounts for

how well established in the Global economy a sovereign is currently and in the near future,

including their Forex reserves and revenues (even if projected).

In 2000, the US Govt. itself was offering ~6% returns over 3-10 years,

India had to offer ~8.5% on a 5 year bond,

to account for the additional risk that

India might not have sufficient USD at the end of 5 years

(however remote the possibility may be).

Also, due to competitive pressure,

these rating agencies continued to rate highly

even securities with known low-quality constituents.

IMO, it is perfectly fine to ignore the upside of these credit-ratings.

But better to pay extra attention whenever a credit-rating is downgraded.

(FWIW, like trailing indicators in TA,

these rating-downgrades often occur after the fact, most of the time.)

A similar situation exists today in the Indian domestic bond market.

A bunch of NBFCs have popped-up,

offering retail individuals access to corporate bonds

offering returns twice as much as sovereign bonds.

(often digitally, at a click of a button on some page).

However, upon careful consideration,

the risk-adjusted returns on offer are only marginally higher.

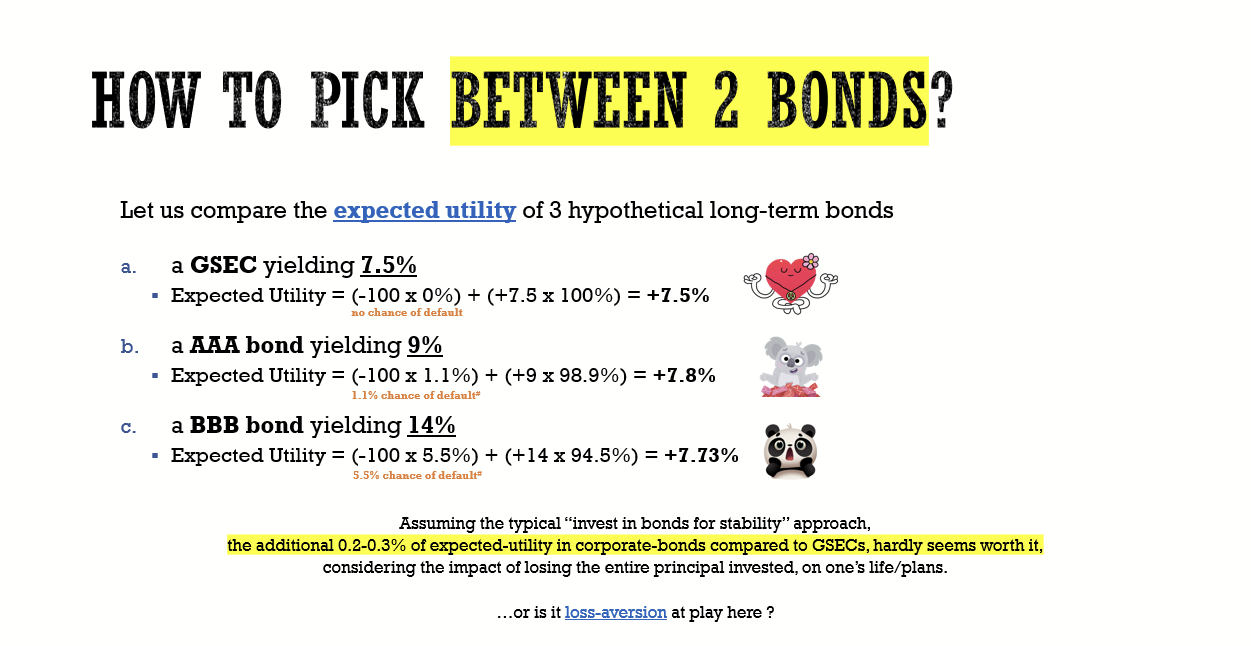

Assuming the typical “invest in bonds for stability” approach,

the additional 0.2 - 0.3% of expected-utility in corporate-bonds compared to GSECs, hardly seems worth it.

Considering the impact of losing the entire principal invested, on one’s life/plans.

Really??? India did not have fx to pay fuel cost at that time.

It was that time this issue csme out and nri indians subscribed.

How is this a weakness.

The entire world was surprised by the oversubscription by nri Indians.

That is just one aspect of credit-worthiness.

That is just one aspect of credit-worthiness.

Every other aspect gets nullified when indian government guarantees a debt. Whstever other aspects are technical.

If nri at that day thought of other aspects, they will be sitting without earning anything. Banks in the middle east leveraged on these bonds to give retail nri 1:9 loan against pledge of these bonds.

All had absolute faith in the sovereign guarantee.

Before we get into all the details, here’s a thought -

If every participant gets a “First place” medal,

does the medal have any value

in grading the participants / determining their relative competence?

Also, none of my comments in this thread about strength or weakness are about nationalist pride or sentiment.

Taking on debt at a relatively higher-cost isn’t a sign of financial strength.

Exactly.

The fact that NRI Indians would step-in to finance the debt

(assuming that is what happened in significant numbers),

wasn’t a safe assumption to make beforehand.

This paper from 2004 that reviewed NRI deposits in India over the past decades,

summarizes the conventional wisdom as…

It finds that monthly deposit flows have been quite stable since the 1991 crisis; nevertheless, there have been occasions when monthly flows turned negative in the short run, coinciding with adverse domestic or external events.

Econometric analysis shows that the NRI deposits are influenced by standard risk and return variables. In particular, NRI deposits respond positively to changes in relative interest rates on NRI deposits and LIBOR; negatively to political and geopolitical uncertainties, such as the government resigning in mid-term, and tensions on India’s borders; and negatively to adverse external events, such as the Asian crisis.

Are you stating or asking this?

If you are stating this, then the lower credit-rating appears to have accurately reflected that precarious situation.

…only when 8.5% dollar-denominated returns were offered. (or maybe the “desi” version of white-guilt was also a factor in the minds of NRIs? )

Subsequently. Right?

And while that was happening, …

…what was the credit-rating of the Indian sovereign?

(i am assuming it would have been higher than the credit-rating when the 8.5% dollar-denominated bond was issued)

…what were prevailing rates of dollar-denominated bonds maturing in a couple of years?

…were there any other factors at play (eg. global sanctions) that limited the ability of these lenders to achieve their desired exposure to USD directly by investing in US bonds?

…which currency were these loans disbursed in? Did the lenders have a surplus of that currency?

BTW, what's a '1:9 loan' in this context? Any public links/references to this?

If it is a loan amount of 9x the pledged security,

that definitely sounds unusually risky for the lender,

without additional guarantees or unusually aggressive repayment plans being involved.

Definitely a scenario that deserves a second look.

Of course, credit-ratings change. As do Bond yields.

As circumstances change, bets considered risky may become safer in future.

The Indian sovereign guarantee can be a “zero-risk” 100% guarantee domestically,

and simultaneously be a sub-par rated guarantee globally.

…in India.

Maybe even in the sphere of influence of the Indian sovereign.

Not globally.

As an hypothetical example,

this conversation would flow differently,

on our chartered flight to the Bahamas (or Liechtenstein),

that we would have to pay in USD (not INR)

when we are being prosecuted for

publicly expressing our views on domestic financial instruments on TradingQnA

(if that day ever comes).

Yup.

A technicality

that was worth roughly 2.5 percentage-points of annual-returns,

on a 5-year dollar-denominated bond, in the year 2000.

It is not about the sovereign guarantee, any government can print money to settle its debt, but doing so, increases the supply of money in the system, which will have cascading effects on our economy.

When there is a credit rating downgrade, it increases the cost of raising fresh funds for the government, due to an increase in risk perception, resulting in a demand for higher interest rates/yields.(risk premium)

When ratings are downgraded, more people start selling govt bonds to invest elsewhere, this results in bond prices falling, and when prices fall, the yields rise.

The rising yield is a sign of rising interest rate, now, if the US govt wants to issue new bonds, it has to do so at a higher interest rate. Just like how, India had to pay a higher interest rate to raise fresh funds when our ratings got downgraded.

And the other side of rising interest rate is that, the government’s interest expense increases, which increases the fiscal deficit, resulting in further borrowing.

The bond yields, act as the base for borrowing rates in the economy, so when yields rise, businesses and households will have to borrow from banks at a higher interest rate, which reduces their purchasing power, resulting in economic slowdown.

Coming to the topic of US retail traders buying the dips despite the rating downgrade, IMO this behaviour looks odd due to the following reason.

When interest rates rise, the interest expense and cost of inputs increase for businesses, which affects their profits, and when future profits are anticipated to be lower, would you invest in stocks now, when they are trading close to ATH ?

This is probably why @Prakashsingh questioned the logic behind retail traders buying the dip, especially when the future looks murky.

it was never a question of financial strenght or not. IMF needed gold as pledge which India did deposit. When the Government had three months of fx reserve to pay for crude, Indian Diaspora coming in and subscribing for the bond shows the belief that the bond will not be defaulted. This is the point that was highlighted. I buy Term Policy only from LIC - not because of any sentimentality or national pride but only because it is owned majority by central Government and hopefully will survive and pay out the money after my death. Same with ETF - chosen SBI ETFs So yes it is strenght at that time.

Again during those times, getting FX inflows had trickled down, Banks offered NRE deposits to double in 4 to 5 years time, This was the rate that was being offered just to attract fx into india. Again this was the time when the Government wanted Foreign currency. NRI obviously obliged only because of the sovereign guarantee.

No one cared what the rating was in 1991. It was survival, to pay in fx for the next shipment of oil. Interest rate or any other factor was not an issue. Getting Fx was the issue. Hence as mentioned above, Banks were offering NRE deposits which doubled in 4 to 5 years time.

The rating downgrade done by moody on India was during Corona time June 2020 and not 1991. So not clear what you mean by stating or asking this. Was our condition that bad during Corona that Moodys reduced Sovereign rating to BAA3. They downgraded and stock market flourished and touched 26,000 did it not. Did anyone stop investing because my dear Moody downgraded. Yes overseas loans would be higher so what, did the economy grow since 2020 or did we face recession.

Obviously, what is so strange in this, no one is here to do charity no one is here to show nationalist pride or sentiment. Government needed USD offered guarantees and Indians subscribed, as this was a great opportunity at that time at that rate. There was no other alternate bond which was offering such high rate for USD with sovereign guarantees and the rate was fixed for the tenor of the FD. I remember few years there was Gold Gilt or Bond at a higher rate which was then closed by government. Same logic applies why did the Government close these bonds, they could have continued and given it at this rate as it was for their own indians. It was not profitable for them, so they closed.

You really think NRI has guilt. He is putting in money as long as NRE deposits have reasonable interest rate and which is tax free. Try bringing it in par with resident indians and see the outflow of funds from the same desi NRIs. No one cares, as long as interest rate is high and customer treated like a king when they come on vacation. Go to Kerala and see the ads that Bankers put up for NRIs in June July - school holiday in gulf. The joke is every NRI or banker visits branch or his house when a NRI comes to kerala - this is the trend. Some even offer taxi service from airport to their home town. Now stopped. The current trend most of the savvy investors has stopped transferring funds in INR to place in NRE deposits. It is transferred as FCNR B deposits as interest rate is above 5.50% due to constant INR depreciation. Gift City allows USD SB account where interest is paid on a monthly basis - tax free. ( I am sure all are aware that for NRE’s FD interest is given only if the minimum tenor is 1 year). Remove all this and see the flight of capital out from the same NRI.

During the real estate crisis when banks were falling in USA, a senior banker from the Gulf mentioned that, this will not have a major impact in India as companies need to produce to feed the domestic population. This is the strenght - Not trying to patrnoise or have any nationalistic pride. This is the fact.

Did not understand the philosophical bit and passing it.

When a person cant repay a Term Loan and his security is being foreclosed, then the banker says they will agree for a reschedulement but interest rate will increase by 2.5 perentage- points. YUP, I am sure know what the borrower will say…Not sure if he will say, its not ok …2.5 percentage points of annual returns on a 5 year term loan will have issue, so please sell the property and I will find a bedspace in the nearest railwaystation or bus stand in this superhot kerala weather also will give my blood as charity to the mosquitoes.

Now the next user.

We all know this concept but try for a second understand the circumstances India was in at that time. I am sure when a person meets with an accident, he will not check whether he has 485.35 to pay for the ambulance, he will just call them and try to get the accident patient to the hospital…

Cascading effects will come in only when you survive the crisis.

Yes fully agree. That is from the overseas market - where does this moody rating impact. If there is a foreign pension fund or government entity or any other multinational want to invest, they have a minimum criteria that the risk grade should be xxx. Yes since India has this down graded rating, they will not invest. But then the world is not centered on these funds alone, As an example when Adani group had serious issues, some Investor from Australia invested right? There will always be investors to invest. If someone can invest in a Teak planatation, looking at pictures of teak in the next 10 years and promising high returns, then real investors will invest in real companies.

Assuming interest rate will rise how much will it rise. Will it be 6% or 7% in US markets. I am sure this interest will be taxed. ARe investors happy with post tax returns, when the worlds best corporates are available in Index fund/EFT and it has fallen sharply where returns will be much higher.

Apart from Treasury Bonds not sure if they have FDs, must have but most of them invest in the market so then they saw the dip they bought. Is this not the same in Indian Markets. In March Nifty fell to 22,100 odd level, was this not bought in and today it is 24,800. Did retailers not buy into this dip, what is so strange, I do not understand.

I wish someone with repute, do advise when market falls to buy. At that time, no one puts their neck out and say “Dont catch the falling knife” and other phrase. When the market is at the peak they say a different story. Gold at its highest level and new ETFs are introduced… why not when the same product was at the lowest.

PS: All valid points are taken in good faith by both the users.

…and the additional returns over and above the 6% returns offered at that time by a AAA rated US bond.

In 2000, the Indian sovereign guarantee (from 2000 to 2005, the duration of the bond)

was worth relatively lesser than the US sovereign guarantee. And the credit-rating reflected that.

The central thrust of my comments in this thread can be summed-up as “People were greedy idiots then. People are greedy idiots now”

Lower credit-ratings result in increasing the cost of debt.

In theory, this is expected to act as a deterrent against risky behavior by borrowers (even sovereign ones).

I see the downgraded ratings of US Sovereign bonds now

(and the past couple instances of Indian sovereign bonds)

as well justified steps to highlight/reflect the relative risks/uncertainties involved on a global scale,

from the perspective of the rating agency.

The fact that NRIs invested in a relatively risky Indian sovereign bond in the past (2000),

has no bearing on why a rating-agency should not downgrade Indian Sovereign rating during the pandemic.

Tangential point...

Of course a lot of things can change if the USD stops being the primary reserve currency of the world. And while it is an entertaining thought, there is no clear path

from here (a world with USD as its primary reserve global currency)

to there (a world where it is NOT)

Even after all the mis-steps by the USA over the years,

as financially relevant/significant nations are themselves exposed to USD,

In this game of dare, that these nations are playing with/against each other,

no one is ready to blink first. Not just yet.

As far as retail investing in stocks goes, risky behavior continues to be prevalent.

This is especially true of folks, who in their current financial situation,

feel that they have little to lose, and much to gain.

(Not being in their shoes, i’m finding it extremely hard to relate to such a risk-loving mindset)

We are talking about the US market, and the increase in retail trading volume.

What’s strange about this behaviour, is the fact that, the dip is not a fall by great margin, all major US indices have shot by more than 15% - 20% in the last 1 month, primarily because of alleged new trade deals and favorable negotiations and easing of tariffs especially on China.

So, I’m not sure what’s driving this market behaviour, other than speculation/FOMO.

Let’s wait and see, if it goes on to make new highs or falls from here, to understand this behaviour.