IMHO, it was a sign of weakness not strength.

In a period of low-interest rates globally,

India had to offer 8.5% Dollar-denominated returns and ~7% Euro-denominated returns to attract investment.

That is just one aspect of credit-worthiness.

The credit rating for sovereigns also accounts for

how well established in the Global economy a sovereign is currently and in the near future,

including their Forex reserves and revenues (even if projected).

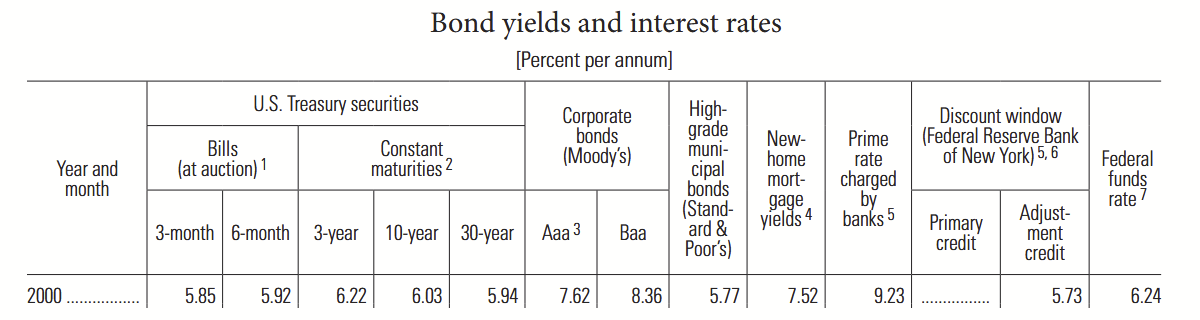

In 2000, the US Govt. itself was offering ~6% returns over 3-10 years,

Source: https://www.govinfo.gov/content/pkg/ERP-2011/pdf/ERP-2011-table73.pdf

India had to offer ~8.5% on a 5 year bond,

to account for the additional risk that

India might not have sufficient USD at the end of 5 years

(however remote the possibility may be).

Also, due to competitive pressure,

these rating agencies continued to rate highly

even securities with known low-quality constituents.

Here’s a dramatic recreation of the same, from the movie The Big Short (2015)

IMO, it is perfectly fine to ignore the upside of these credit-ratings.

But better to pay extra attention whenever a credit-rating is downgraded.

(FWIW, like trailing indicators in TA,

these rating-downgrades often occur after the fact, most of the time.)

A similar situation exists today in the Indian domestic bond market.

A bunch of NBFCs have popped-up,

offering retail individuals access to corporate bonds

offering returns twice as much as sovereign bonds.

(often digitally, at a click of a button on some page).

However, upon careful consideration,

the risk-adjusted returns on offer are only marginally higher.

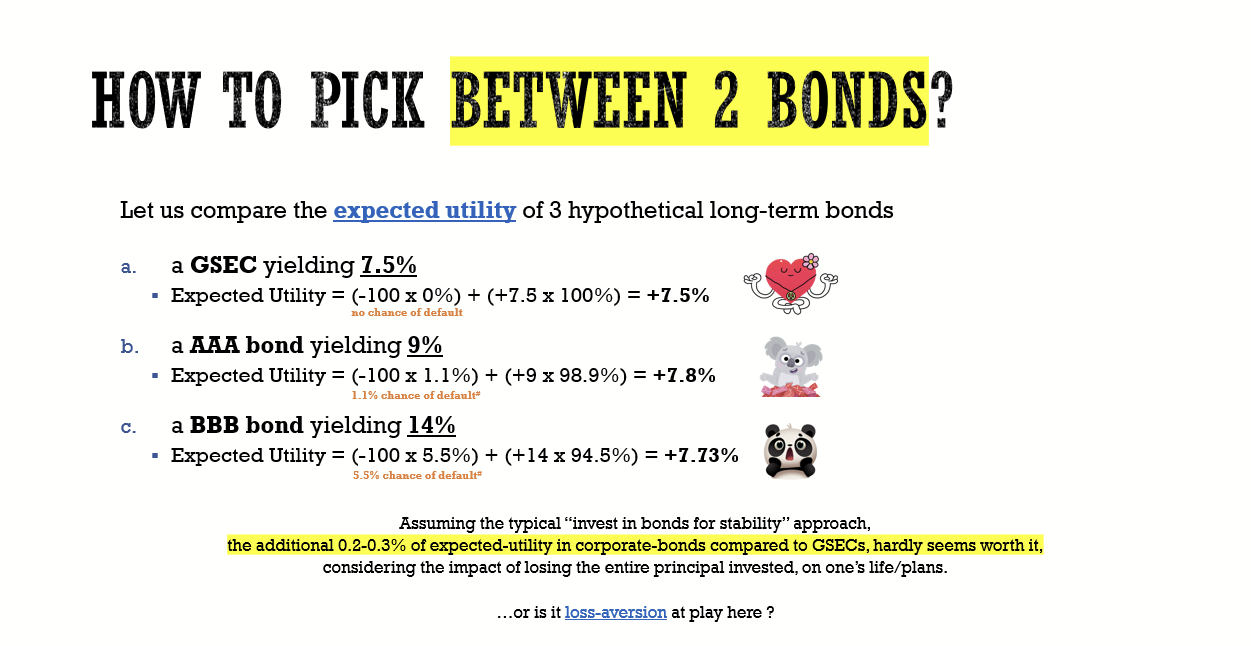

Assuming the typical “invest in bonds for stability” approach,

the additional 0.2 - 0.3% of expected-utility in corporate-bonds compared to GSECs, hardly seems worth it.

Considering the impact of losing the entire principal invested, on one’s life/plans.

…or is it loss-aversion at play here ?