Howdy peeps,

Please have a look – does it seem sensible?

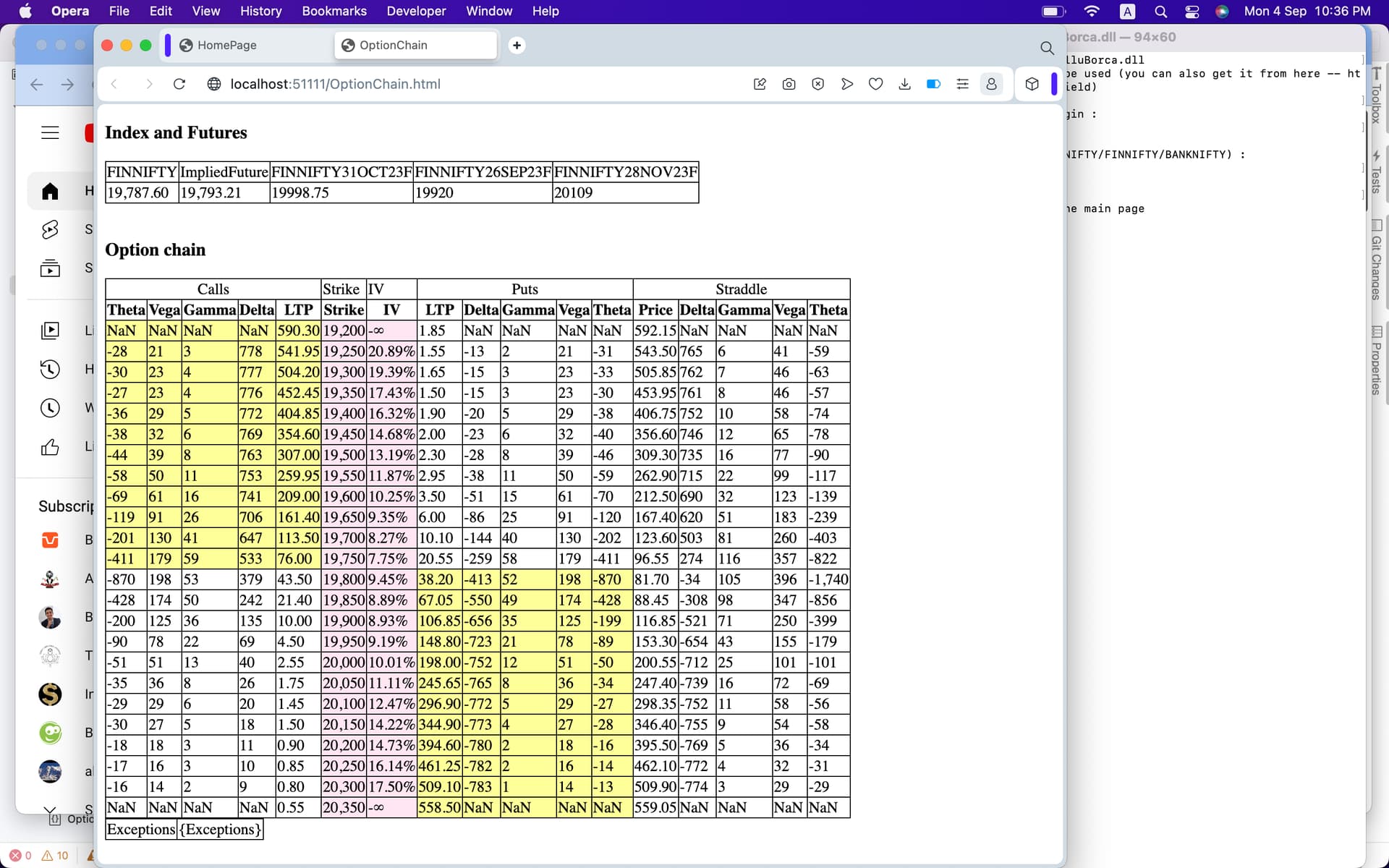

This is Finnifty options (around +/- 3% from spot) taken around 8 pm on 4th Sep. All options here are for 5th Sep expiry.

I am trying to calc the greeks locally using c# and then display as web page. It is subscribed to LTP feed from a broker. This runs as console app running a webserver till user gives the exit command. Webserver simply loads data from a data structure which is being updated via websockets.

RFR is taken from an economics website (I enter it once the app starts). Other inputs are underlying index, expiry date.

Index future is calculated as:

IndexSport * exp [RFR * Time to Expiry]

the future is then used to get the IV. IV for a strike is also calculated for OTM option’s IV (as ITM are illiquid and gave horrible IVs in first attempt).

Black model is the used to calculate Delta, Gamma, Vega, theta.

Delta → 0.1% change in underlying. bump and reprice.

Gamma → 0.1% change in underlying. bump and reprice delta.

Vega → 1% change in IV

Theta → nothing changes except time, which goes to the next biz day. then change in NPV is theta.

I found something similar on sensibull, but delta there is for 1 unit change. Ideally, it should be a generic number like 1% change in underlying or something similar. I chose 0.1%. So for FINNIFTY, the delta represents expected change in option value for ~19 points change.

Hi, I found something similar on sensibull, but delta there is for 1 unit change. Ideally, it should be a generic number like 1% change in underlying or something similar

Sensibull gives delta change for 1 unit. That is too small, specially for large indices. also 1 unit of underlying move for FINNIFTY and 1 unit of underlying move for BANKNIFTY do not carry the same magnitude. So I wanted percentage change instead. All big institutions manage their equity and fx greeks this way.

@Himalayan_Organics Man, Delta has to be calculated using absolute points. It not being calculated as % is the main reason why Options give so big moves. It’s the nature of Options to have Delta in plain points. Try and see some Option charts again, maybe you’ll realize.

Yes.

how do you add and figure out your total risk otherwise?

it is like adding apples to apples vs apples to oranges.

Ex: if you carry positions on both banknifty (in 40k range) and finnifty (in 20k range).

banknifty movement points will be larger in magnitude vs finnifty (usually…).

If you calc delta as 0.1% change in underlying, you can add up deltas of both positions and get an estimate of your total delta. It is more likely to estimate both underlying moving by 0.1% rather than thinking of both moving by “1 bps”.

this is used across the borad for equities and FX. For rates, we use 1 basis point move, because all rates are usually in same magnitude and are mean reverting. Equities and FX are not – so there is a very big variance from penny stock to indices which are marked in 10s of 1000s.

Suppose if Nifty is at 19500, it gives 200 point move, that’s 1.02% in one day, now suppose the ATM strike LTP was 100, now it’s at 300, now how do you transform the 1.02% of the underlying to 200% of the Options contract?

If you’re an Option seller, you’d theoretically need Vega along with Gamma & Delta where Vega would define your risk along with many other factors, but Gamma and Delta would be used only in case your SL was to be hit. I still can not understand how calculating Delta as % works here. Perhaps they simply take some plain points from here and use them as % of something there, all but nonsense, making a joke but why don’t they simply just trap some retailers?

EDIT: I still don’t understand how you intend to use delta to define risk, but I could deduce the above, will be nice i you could say if this was the case with you or something else. (Not even the mean-reversion thing made any sense.)