If a PUT on the index(not stock) goes ITM, and we roll it OUT to next expiry (same strike), and then it goes deep ITM and we still roll OUT (same strike). So what?!

We collect premiums and there is a breakeven in each expiry before the losses happen (and for a month or two or three, the breakeven could be consistently breached) and the index will eventually come around, at which point all our historical premiums will effectively count. What am I missing?!

I realize that along the way, any losses are realized (pun), but its just a matter of time (or is it?).

I suppose the danger is the big moves: a big down move in an expiry followed by a big upmove to get above your strike in another expiry, wherein your net premiums may not be enough to offset the realized losses.

Currently

Nifty 15000 PE for June 24 is trading at 654.

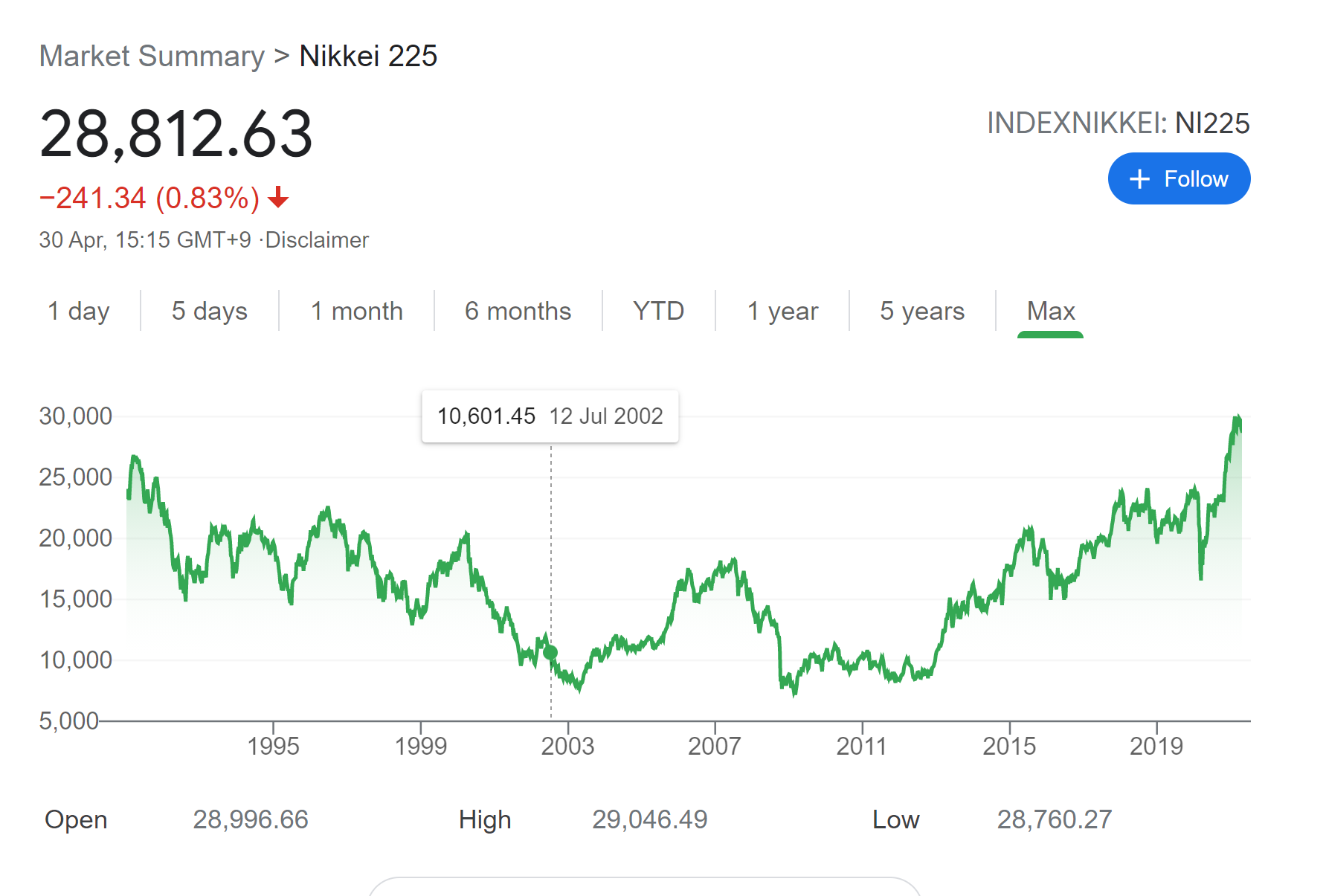

Nothing wrong , but sometime you may have to wait for months and years to get to break even . eg: if you had let say shorted Nifty CE in Oct at 12000 , you would be still waiting to get to break even!!! and would be booking losses every week. In Japan it took 30 years for the index to return to from all time high to all time high!!! so you never know. so if someone shorted Nikkei PE at 25000 he would have waited 30 years to get break even

Rolling CE on the Nifty is trickier imo. Rolling OUT Puts offers some comfort because the Index is assumed to have some upward drift.

I am aware of the Nikkei slump, and its alarming

At its height, in 1989, real estate in Tokyo sold for as much as $139,000 a square foot—more than 350 times as much as choice property in Manhattan. Such valuation made the land under the Imperial Palace in Tokyo notionally worth more than all the real estate in California .

Nifty from Nov 2010 to Nov 2013 didn;'t cross the highs, so your break even took 3 years. Same in 2000- 2004. So unless you are 100% sure of catching tops and bottoms , this won’t work in sustainable ways. Markets always form new patterns !! + At some point you would face liquidity crunch on those strikes as well. I personally not prefer positional options and Futures more than 3 months. Maybe you may set a timeframe that if breakeven don’t come in X amount of time you may book loss. Then it might be sustainable.

While I can make a rough guesstimate what you are trying to achieve … can you please explicitly state it. Probably in a sentence or two. It should go like this -

My strategy is to do XYZ every month and my exit point will be either expiry or ABC (risk/reward).

And maybe then, it is easy to do SWOT analysis on your strategy.

I have been testing a lot of mean reversion scenarios on excel and doing some backtests. It appears there is no real edge (as expected) in Naked Options, but there is something in the short ATM and NTM PUTS in high IVP when there is the slightest hint of reversal. But here too, there are some pitfalls.

And so, I was considering rolling OUT the ITM puts, when in significant loss, a few times. And like @AlgoEye pointed out, there has to be a point when you stop doing that. History shows that. Having said that, this Nifty is a completely different beast compared to yesteryears Nifty .

Here’s a plan (more a scenario)

Sell ATM or 30 delta puts on Nifty based on 5-10 EMA crossovers in high IVP scenarios.

If ITM, Roll it out. Buy some Nifty Bees

If still ITM, and realized loss for the expiry, roll it out. Buy some Nifty Bees

If still ITM, but with some profit for the expiry (but not in overall profit), don’t buy Nifty Bees, Roll it Out

Stop after max 5 Rolls.

Liquidity will affect feasibility ofcourse. And you could argue that one could place fresh trades at new strikes, but it all depends on one’s psychology and for some, psychology has to be protected (within reason).

Writing puts at 30-50 delta you make 1% as maximum premium on a weekly basis. (nifty long term average)

You do this come what may without any cross over condition or your emotions.

You do not buy nifty bees when it goes ITM. Keeping it out of the equation. It is like saying if you buy NIFTY BEES the market will stabilise which is certainly not true.

You sticking to only one position in a month and not increasing the quantity.

I did a backtest for 22 years. And the results are -

A margin money of 1.5 L will roughly become 6.21 L and that is a CAGR of 6.67%.

At the same, NIFTY itself has gone from 890 to 14631 producing a CAGR of 13.57%.

The strategy also had a maximum drawdown of -83265 and maximum profit of 10k. Assuming anytime when you have a drawdown more than than three times the maximum profit your can make - you blow up your account, (since you can’t take new position next week) - You actually blow up your account 13 times out of 119 weeks.

So it is needless to say - this is a horrible strategy. And this on NIFTY which hardly had any longer term slump in the market like Japan over the past 22 years.

Hope the data points in my explanation help you give pointers on how to form a more reliable and consistent strategy.

I backtested since 2014 when IVP > 50 and Close crossovers 5 EMA. Looks alright without the Rolls when you book losses at max 100% and book profits at 80%. Results are bad when you just let it expire without loss management. Forgot to mention this small detail

Ok … I will try to answer those questions and call few of the assumptions -

I have my own python based infra that I rely on.

This is based on technical analysis. I picked almost all the technical indicators and tried to find an edge out of them and they have an exact probability of 50% of giving profit that too in 1:1 risk reward and it actually decreases when you set risk reward 1:2. That is as good as tossing a coin - over a very long period. Hence, I don’t rely on it.

Has two sides … May work in giving you higher premium, but reduces probability of profit. I don’t have an infra to test on this for the latest IV values kind of overrides previous ones making them moot over a very long time. But will think about it.

Ok. So this is like a key point. Let me attempt to explain - You do not know in the middle of an open position if the position you are having is going to give you loss at expiry or profit. If you do loss management, you might just turn a position that was going to give you profit at expiry into twice the loss.

This does not mean risk management is not required. But at least when you are designing the strategy … look at minimising the drawdowns and possibility of account blowups.

I don’t think I can explain it … but it can only be learnt by experience.

Trust me, I am careful and I am cognizant and wary of account blowup possibilities. Backtest in the past 6 years, shorting puts when IVP > 50 with some EMA crossover criteria has meaningfully outperformed other IVP and non-tech criterias when done with loss and profit management.

Ofcourse, but you have to, to prevent/reduce blowup possibilities.

And all I have is without the ROLL ofcourse. I need to see it fail badly. I want to break it (without it breaking me). How are you backtesting . I mean, what are you using to backtest? Python?

Yeah. That my friend is like really getting involved, making sure you are on the terminal at all times and is constant decision making. And that a backtest won’t tell you. This is the devil that lies in the detail - i.e. operational execution.

Sure … Try to live with open positions in your strategy on the following weeks -

#

Date

Close

Weekly PnL

1

3/20/2020

8745.45

-83265

2

3/13/2020

9955.2

-69327

3

2/28/2020

11201.75

-56872

4

1/29/2021

13634.6

-44519

5

5/8/2020

9251.5

-38235

6

10/5/2018

10316.45

-37852

7

10/10/2008

3279.95

-37513

8

4/3/2020

8083.8

-36739

9

2/1/2020

11641.25

-36339

10

2/12/2016

6980.95

-32494

11

1/18/2008

5705.3

-32460

12

3/7/2008

4771.6

-29975

13

7/10/2009

4003.9

-28208

14

5/19/2006

3246.9

-27499

15

7/3/2008

3925.75

-26021

16

9/25/2020

11050.25

-25474

17

5/10/2019

11278.9

-23717

18

2/26/2021

14529.15

-22709

19

1/8/2016

7601.35

-21166

20

9/4/2015

7655.05

-20016

Don’t just look at OHLC, but how your strategy will respond when you are in the middle of the week, whether the preconditions will eliminate these weeks altogether or not, etc.

Note: On IVP, if volatility increases to 80% (Mar 2020) it will mark a 39% IV not part of your criteria. But during all previous times an IV of 39% would have met your criteria giving IVP Rank 1 (100%). So do check the backtesting infra if it is point in time or overall and I think it will be overall making the payoff calculations moot.

I only looked at monthly expiries, not weeklies, and look to exit trades after 15 days, no matter what. That’s another criteria that I failed to mention. Not at all comfortable with Weekly expiries for this strategy, the IV will usually need some time to cool off.

Yes 2020 was a special situation IVP, but seemed ok overall.

@abhiwin123 how are you backtesting? Did you purchase data? And splice the data with python? Please do let me know if possible.

Yes. At one point in time from DotEx. The company is merged in NSE now.

Yeah, own Python Backtesting Infra, its pretty basic actually and mainly built on - NumPy, ScipPy, Pandas, TA-Lib, Zipline, etc. Serves me well …

Hi, how can we do this type of backtest if we don’t know python and other infra etc which you have ?

Are there any 3rd party softwares or platforms where we can do this type of backtest ?

options would be difficult but you may indirectly do it with index or futures. Yes, it won’t be too accurate. Python is very flexible in that way otherwise some online tools etc

There is streak - requires no coding and is mainly on technical analysis. But I don’t think it is for Options. Not aware of any 3rd party software / platforms that can do the same.

Also, I don’t think there can be a platform that can do option testing for the sheer inability to do this on scale with the multitude of strike data and non-continous nature of it. Plus with low liquidity in indian markets its very very difficult to trust the payoffs.

Say you write at 30 Delta Put every week. For a platform to test it needs to first of all make a continuous chain of strikes that is available at 30 delta and then treat it as a continuous data - which precisely is a scalability nightmare. The juice is not worth the squeeze for anyone selling this.

So if you think about the silver lining, it is worth investing in necessary time and effort to do it on an individual level. I don’t have that granular data. If you are reading through for the same example above, I just assumed 1% premium at 30-50 delta which a platform cannot.

And I do believe there is significant alpha remaining in building such a system for your own. I am sorry but I can’t share more. I hate the fact that option selling is no longer as profitable as it used to be from 2014-2019 after which this tsunami of option seller trainers hit the market reducing the arbitrage opportunity. @Vij probably the reason why you see this strategy profitable in backtesting because 2014-19 timeframe was golden period for option selling.

Ya well, I agree, there’s no real mechanical edge… In any case I’m going to mostly do secured puts and covered calls initially. Just looking to build on what’s been good for me trading stocks. Add a few % points, smoothen the curve, that sort of thing.

You will keep booking losses and depending on the down move it could be a big loss too…loss impacts your available margin…you r right at some point mkt will reverse. Assuming you roll out for the same credit as the position you’re closing your max profit would be the credit on your first trade …this is martingale strategy and can also be used with calls…as margins get impacted position sizing critical