Securities and Exchange Board of India has put up the Annual report for 2017-18.

Click here to view and download the report.

Understanding the economic and regulatory environment can definitely give an edge when it comes to trading and investing. This reports contains useful information & data regarding -

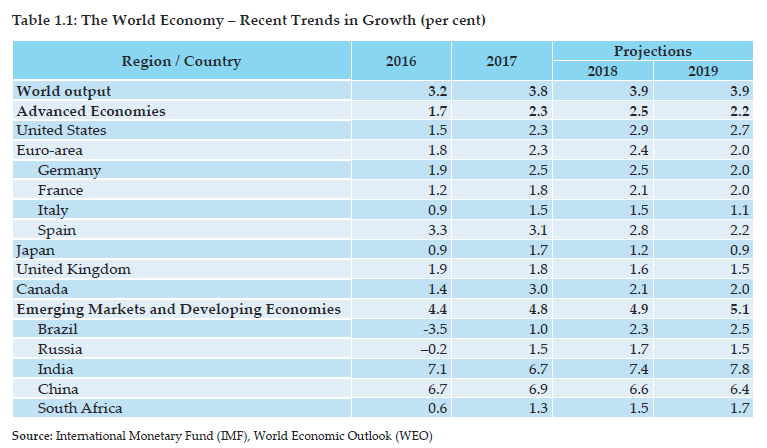

- Trends in global economic growth

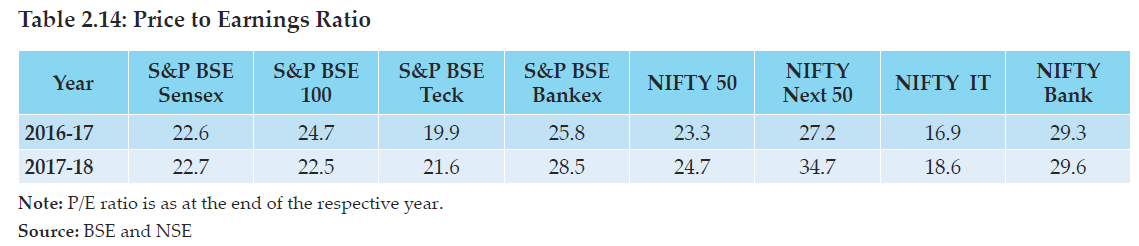

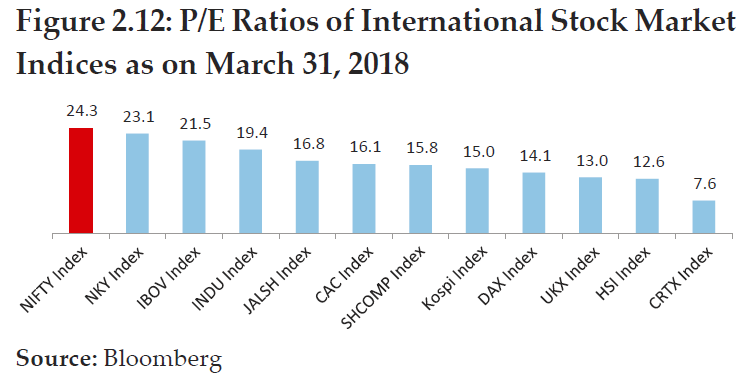

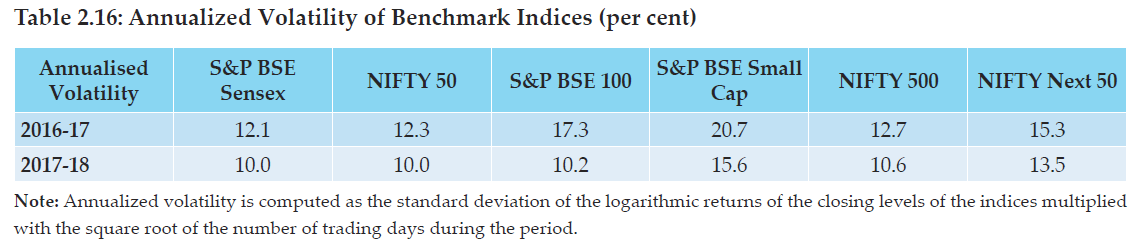

- Major indicators in the Indian securities market,

- Trends in the Index & Stock F&O markets,

- Trading statistics of Stock exchanges,

- Trends in Mutual Fund resource mobilization & Transactions on Stock Exchanges

and more. You can check out page 21 on the report for the lit of box items i.e interesting nuggets of data represented visually. Some important and relevant aspects i’ve summarized in the posts below -

Overall Economy

-

As per the annual data for 2017 published by World Federation of Stock Exchanges (WFE), NSE is placed at first position in the World in index options and at second position in stock futures, when ranked in terms of the number of contracts traded

-

According to IMF projections, the Indian economy is expected to grow at 7.4 per cent in 2018 and 7.8 per cent in 2019 which is significantly higher than the 6.7 per cent growth in 2017.

-

Growth trends by country - in terms of %

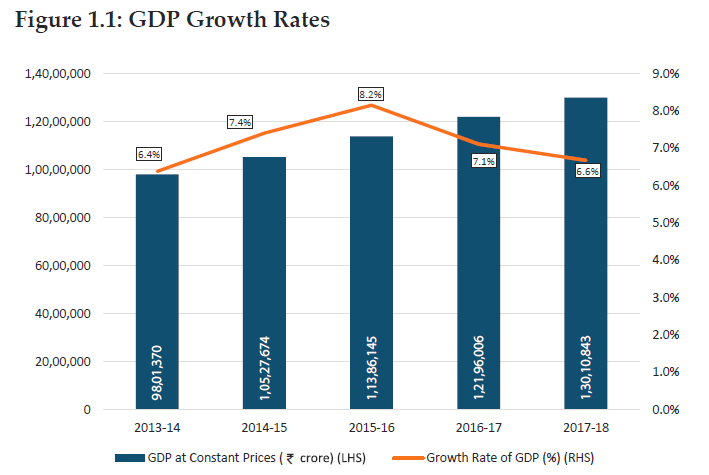

- As per the Central Statistics Office’s (CSO’s) provisional estimates, the Indian economy grew by

6.7 per cent during 2017-18 against a growth rate of 7.1 per cent during 2016-17. Economic Survey 2017-18 forecast that India may record real GDP growth in the range of 7.0 to 7.5 per cent in 2018-19

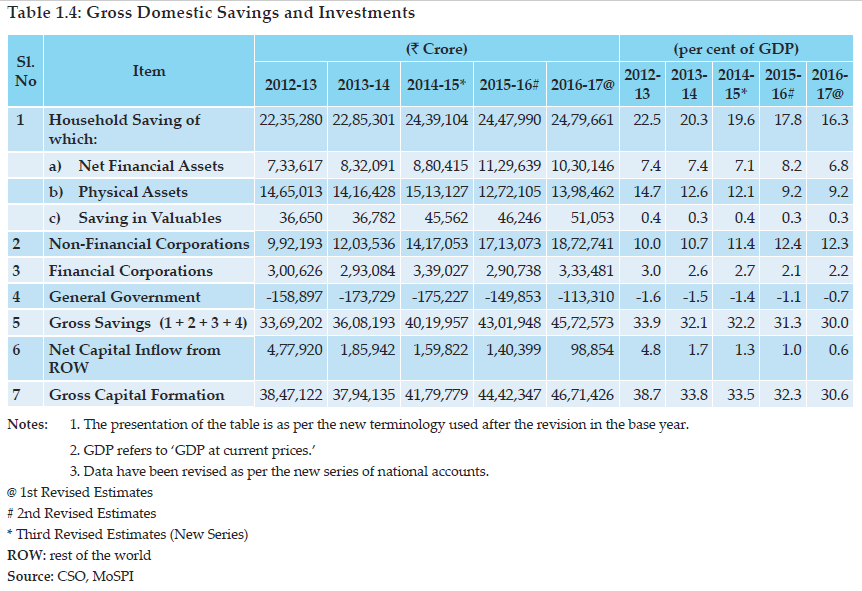

- During 2016-17, gross saving is estimated at 45.7 lakh crore as compared to 43.0 lakh crore during corresponding previous year.

Others

-

Retail investors can now seek redressal where they have suffered an opportunity loss in an IPO due to SSCBs failure to make bids, process ASBA etc

-

SEBI revised provisions relating to Transfer of listed specified securities and decided that requests for effecting transfer of listed specified securities shall not be processed unless the securities are held in the dematerialized form with a depository.

-

Non-resident Indians (NRIs) have been permitted to participate in the exchange traded currency derivatives market to hedge the currency risk arising out of their investments in India. In this regard, guidelines with respect to trading by NRIs in exchange traded currency derivatives market and permissible position limits were specified.