Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- SEBI finds glitters of ₹15 lakh crore that aren’t gold

- Space II: Earning a living

SEBI finds glitters of ₹15 lakh crore that aren’t gold

On June 3, SEBI issued a 109-page interim order against Rajesh Exports Limited (REL), a gold retailer, and its promoter-chairman Rajesh Mehta. SEBI’s primary allegation is this: Between FY20-FY25, REL reported total consolidated revenues of ₹15.45 lakh crore, 99.8% of which was flat-out misrepresented.

To make sense of those numbers: REL’s annual revenue in FY25 was ₹4.53 lakh crore. That’s the same ballpark as a company like HPCL, which made over ₹4.78 lakh crore in FY26.

REL’s stock peaked at ₹1,028 in February 2023, but was trading at ₹104 when the order dropped. It hit the lower circuit right after this order. SEBI estimates that ₹12,726 crore of public investor wealth has been eroded. Over two lakh shareholders, including LIC, are left holding the bag.

But this isn’t a single allegation. Behind this number is an elaborate architecture that lays out a multi-layered scheme involving unexplained overseas revenue, questionable trades, and round-tripping through personal bank accounts, and some regulatory smoke and mirrors.

Nor has this come out of the blue. A decade ago, the Moneylife team, led by revered financial journalists Debashis Basu and Sucheta Dalal, analyzed REL’s books in their own capacity. There were reports from others that something about REL didn’t sit right.

Then, in 2024, SEBI received a cautionary email from a then-REL shareholder. That started an investigation, whose result is this mammoth order.

Let’s dive in.

Midas touch

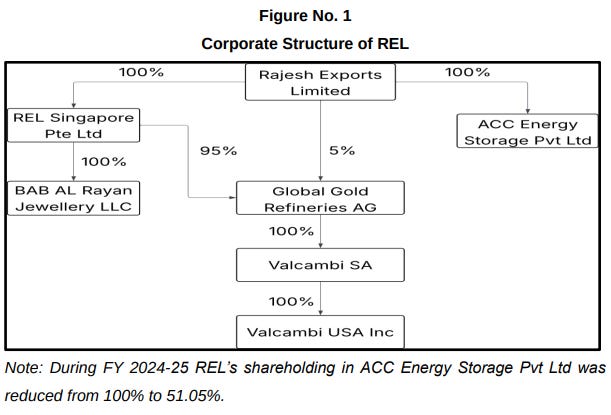

Usually, at the core of most creative financial engineering (or tricks) sits an elaborate corporate ownership structure, where one dark cave leads to another. REL, turns out, is no exception to this.

The parent REL entity owns REL Singapore, which in turn owns 95% of a Swiss holding company called Global Gold Refineries AG (GGR), while the parent entity owns the other 5%. GGR itself owns 100% of Switzerland-based Valcambi, which actually is one of the world’s largest precious metals refineries, processing over 2,000 tonnes of gold, silver, platinum and palladium annually. REL acquired it in 2015 for roughly $400 million.

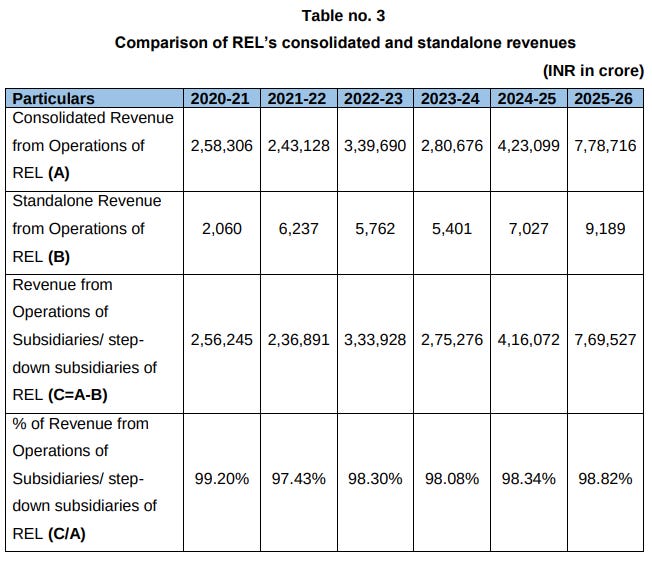

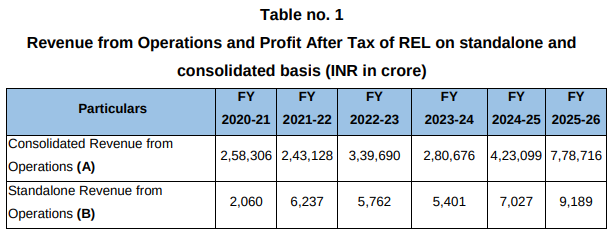

In REL’s financials, most of its consolidated revenue comes from its subsidiaries. Its standalone business barely makes 1% of revenue. Odd, but maybe not illegal.

Except, many of the discrepancies flagged by SEBI — including the biggest one — come exactly from this difference.

Worth its weight in gold?

Let’s start with the most significant discovery, which involves the Valcambi subsidiary.

Now remember, Valcambi is just a refiner . It doesn’t buy or sell gold on its own account. Banks and bullion dealers send their gold to Valcambi for processing, and Valcambi earns a fee. The gold belongs to other people.

Valcambi’s audited financials, which are prepared under Swiss law, reflected exactly this. In the calendar year 2023, Valcambi reported revenue of about ₹543 crore. In 2024, it was ₹427 crore. That’s normal for a leading business in this industry.

But GGR, the holding company one level above Valcambi, was recording something entirely different. In its consolidated statements, GGR booked the entire market value of the gold passing through Valcambi as its own revenue. For 2023 alone, that came to over ₹2.9 lakh crore. More worryingly, GGR had no actual business operations of its own.

Then, REL took GGR’s massively inflated numbers and consolidated them into its own Indian financial statements, while keeping Valcambi’s actual audited numbers hidden from the public.

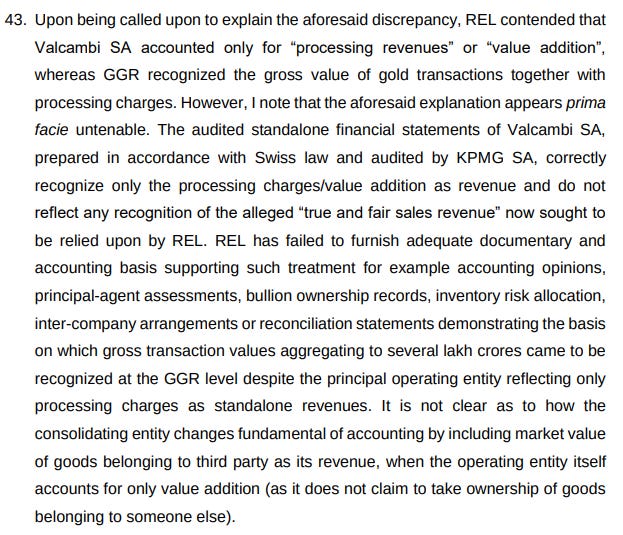

When SEBI asked REL to explain this, REL claimed Valcambi only recorded “processing revenues “, while GGR recognised the “true and fair sales revenue “. SEBI found this commercially implausible, and REL couldn’t produce a single document in support of this claim.

To add more fuel to the fire, GGR’s consolidated statements were never subjected to a statutory audit under Swiss law . They were voluntarily prepared under an internal “Group Accounting Manual “. KPMG, which is Valcambi’s auditor, specifically clarified that its opinion on GGR did not constitute a statutory audit. In effect, REL was funnelling unaudited, self-prepared numbers from a shell holding company into its audited Indian filings.

Meanwhile, REL never uploaded the financial statements of any subsidiary on its website — a straight violation of the Companies Act. When SEBI demanded the data, REL cited the Swiss Federal Act on Data Protection, claiming Swiss law prevented it from sharing corporate financial information with Indian regulators. But SEBI took this apart cleanly, stating that the Swiss law only protects personal data of natural persons , not corporate entities.

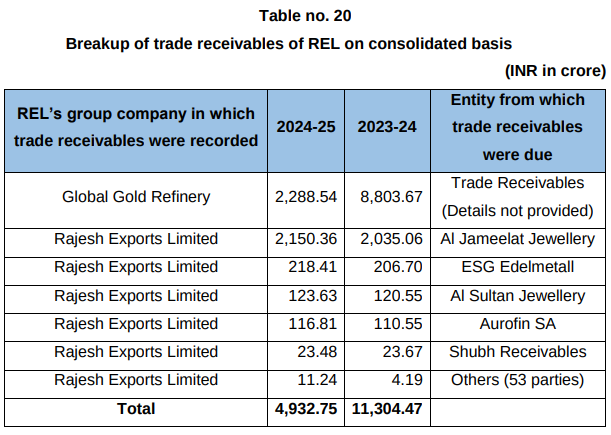

In fact, GGR sat at the centre of many of REL’s balance sheet oddities. To justify some of their massive revenues, REL claimed that their corresponding trade receivables were on GGR’s balance sheet, but SEBI found no such proof of this.

The investment mirage

Besides Valcambi, there was another similar discrepancy that SEBI found.

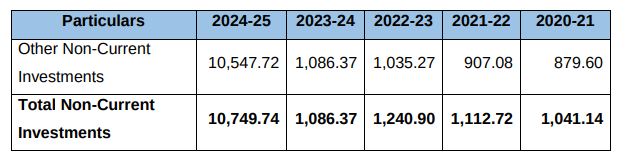

On its consolidated balance sheet, REL’s “Other Non-Current Investments” line item ballooned unexpectedly by twelve-fold within 5 years to over ₹10,500 crore in 2025. REL said that this reflected their investments in African gold mines.

It is unusual for a gold retailer, which is a relatively asset-light business, to outright purchase gold mines, which need multiple times more capital. SEBI decided to look into the statements of the REL Singapore and GGR subsidiaries, and lo and behold, they found nothing related to gold mines.

Besides this, REL also failed to adhere to basic Indian accounting laws. For instance, a parent company’s consolidated financials must exclude investments made in its own subsidiaries, or the debts owed to subsidiaries, in order to prevent artificial inflation of the size of the business. However, REL did not follow this rule, keeping ₹2,500 crore of intra-group investments in its consolidated books.

All of this gave retail investors the idea that REL was a behemoth in the gold retail business. But the truth, SEBI says, couldn’t be further from that.

Trouble at home

While the overseas consolidation created an illusion of global scale, REL was simultaneously manipulating its domestic standalone books.

Between FY22 and FY24, REL recorded ~₹11,487 crore of sales and ~₹11,488 crore of purchases with a SEBI-registered stockbroker called Affluence Shares and Stocks. These transactions made up 66% of REL’s total standalone sales.

If you didn’t notice it yet, the oddity lies in the negative difference between the sales and purchases. In sum, the transactions actually lost ₹1.82 crore. Why would anyone do this?

SEBI found that REL was never actually an Affluence client. No transactions were ever conducted with or on behalf of REL. So what were these entries?

It turns out that Rajesh Mehta, REL’s promoter, had been trading gold derivatives through his personal trading account at Affluence . REL transferred ₹7.45 crore to Mehta’s personal bank account as margin money. Mehta traded on 102 days, lost ₹3.50 crore, and the net balance was returned to REL through him. The actual cash that changed hands was less than ₹8 crore.

However, REL booked the gross notional value of Mehta’s personal derivative positions — totalling ₹11,487 crore — as the company’s own sales and purchases. No GST records existed between REL and Affluence. No board approvals were found to have authorised Mehta as a conduit.

Funnily, REL seems to have a habit of booking the gross value of assets that pass through its hands as if they were income — whether it’s gold flowing through Valcambi’s refinery, or the notional value of the derivative trades.

When confronted, REL claimed Mehta acted as a “conduit “ due to litigation with MCX. Again, SEBI found no evidence to support this.

Beyond the Affluence scheme, REL padded its standalone numbers in other ways.

For instance, it classified ₹867 crore of foreign exchange fluctuations as “Revenue from Operations “, instead of recognising them separately as non-operational revenue as per Indian law. It recorded ₹204 crore of interest from fixed deposits and mutual funds as operational revenue as well.

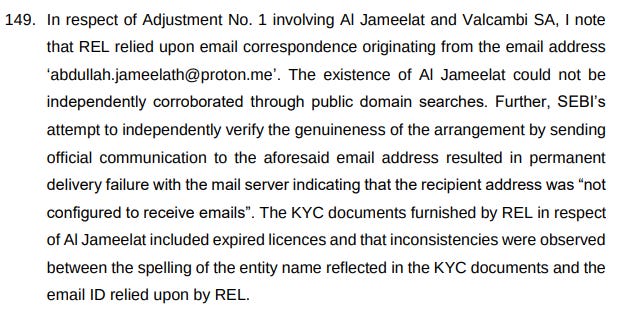

REL also erased ₹2,914 crore of long-outstanding trade receivables by “netting “ them against trade payables. To do so, they used unverifiable email correspondence, telephonic understandings, and confirmation letters, obtained only after SEBI began asking questions. For instance, the email address for one counterparty, Al Jameelat Jewellery , bounced permanently.

One-way round-trip

If the story so far has been about numbers on paper, this part involves actual cash round-tripping the company.

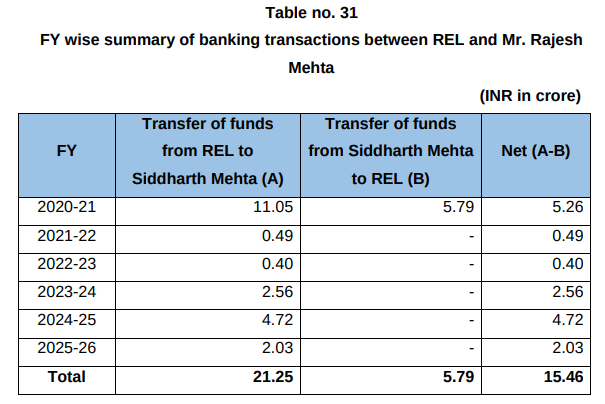

Between April 2020 and September 2025, REL transferred ₹339 crore to Rajesh Mehta’s personal bank accounts, and ₹232 crore came back. Where’s the other ₹107 crore?

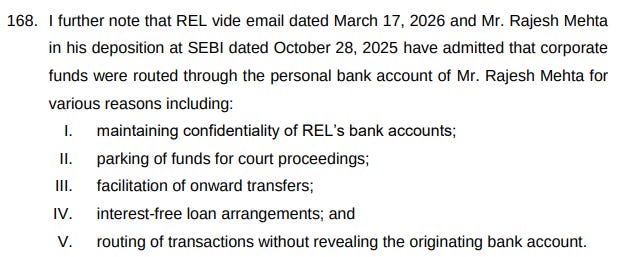

When SEBI asked why, Mehta had a myriad of explanations to give, from parking funds for court proceedings, to routing transactions without revealing the origin bank account. None of this was disclosed as related party transactions. None went through the Audit Committee. REL’s annual reports showed exactly ₹1.20 lakh per year as Mehta’s remuneration, while hundreds of crores flowed through his personal accounts.

Interestingly, ₹21 crore went to Rajesh Mehta’s son, Siddharth, who had no formal role in the company. The rationale that REL gave was that the funds paid for operational expenses through his personal credit cards . It furnished 140 credit card statements, but many of them were incomplete, with amounts that didn’t reconcile.

Then there’s Elest Pvt Ltd, a publicly-listed company that Rajesh Mehta incorporated for EV battery manufacturing, separate from REL. In fact, this company also enjoys the benefits of the PLI scheme for EV batteries. Quite odd for a gold company to make such a move.

But what wasn’t believable was Elest’s role. REL transferred ₹565.88 crore to Elest; ₹350.03 crore came back, and the rest couldn’t be explained. Despite this, REL disclosed only ₹12.60 lakh in rental income from Elest in its annual reports.

The Elest rabbit hole goes deeper. In January 2025, Elest was allowed to subscribe to shares of ACC Energy Storage, previously a wholly-owned REL subsidiary. This diluted REL’s ownership to 51% — nearly half of a subsidiary was transferred to a promoter-controlled entity .

Then came a bizarre case of circular funding. Elest sent ₹147 crore to ACC Energy, and ACC Energy returned ₹112 crore the same day . ACC Energy later invested ₹262 crore back into Elest.

This helped engineer a dramatic escalation in Elest’s valuation. In April 2021, Rajesh Mehta bought 15 crore Elest shares at ₹10 per share. Three months later, REL subscribed to 1 crore shares at ₹200 per share. By late 2023, FPIs were paying ₹3,000 per share.

Only guilty when caught

None of this would have survived scrutiny if the underlying data had been made available. But, as per SEBI, REL went out of their way to ensure a lack of transparency.

In December 2024, while investigating REL, SEBI appointed BDO India as the forensic auditor. But REL refused them access to their systems and accounts. For foreign subsidiaries, it hid behind Swiss data protection laws. Even where ledgers were produced, narration columns were only partially visible and corresponding account names were missing.

Out of a selected sample of ₹7,021 crore in purchases, REL provided complete documentation for 2.03% of the sample value. For sales samples totalling ₹12,217 crore, only 35% could be verified.

When SEBI demanded customer-wise sales lists, REL provided three different submissions at different stages of the investigation, and they all contradicted each other. Sales figures for the same customers seemed to vary by hundreds of crores. When confronted, REL asked SEBI to simply “ignore earlier submissions and rely only upon the latest data ”.

What happens now

This is an interim order, not a final adjudication. Rajesh Mehta is barred from dealing in REL securities until further orders. A new forensic auditor will be appointed. REL has 30 days to hand over a massive tranche of withheld data.

REL has responded with a five-point clarification calling the order “interim,” claiming its revenues are correct, and attributing the issues to a “communication gap”. The stock hit lower circuit the morning after.

All of this started with one shareholder emailing SEBI in March 2024. What SEBI found blew open the lid on a can full of worms.

Space II: Earning a living

If you were to switch to another tab, at this very moment, without paying anyone or asking permission, you can pull up a satellite photograph of almost any point in India. The Americans give their imagery away. So do the Europeans. Their pictures are a few days old and a little coarse — but they’re free, and they cover the entire planet.

Who, then, would actually pay for the same thing?

In our first part of this series, a few weeks before this, we looked at how a growing number of Indian companies were trying to compete with those free services, beaming in data from space. Space had finally opened up to Indian business five years ago. The law had changed, our space institutions were reconfigured, and a new generation of ambitious private companies now dreamt of owning and operating their own satellites.

But the fact that they can now legally participate in space only opens the way to a harder one: how do they actually make money?

The most expensive way to take a picture

Last time around, we spoke about Mission Drishti. A Bengaluru startup, GalaxEye, had managed to get the 190 kilogram satellite — the largest an Indian private company has ever built — into orbit.

This was the culmination of years of work. Its payload — the “OptoSAR”, or an optical camera paired with an advanced radar that can see through clouds — had consumed most of the company’s five year-long existence. It needed years of testing and redesign, with many discarded prototypes by the wayside, before it would reach anywhere near space. Through that entire period — well before their maiden space voyage — Galaxeye had to pay years of salaries to highly qualified space scientists.

They had to make sure their satellite would survive being shaken, baked in direct sun, frozen in cold space, and starved of air, all to prove that it could handle a launch and the emptiness of space. They couldn’t do this in any ordinary garage. They needed specialised equipment, in buildings that were built for this purpose. Much of this was only possible because of outside support from other organisations — including ISRO, through the doors IN-SPACe opened.

Putting their satellite together, though, was only the first step. Then, they had to get to orbit.

A shared ride on a SpaceX rocket — despite being the cheapest on earth — runs to several thousand dollars per kilogram. For a satellite the size of Drishti, the launch bill alone would run into the millions. And then, before the rocket even leaves the pad, there’s insurance. There’s a very real chance that the whole thing ends in a fireball. And so, you need to pay a premium worth a tenth or more of the satellite’s value upfront.

This is now over. Drishti is in space. That doesn’t mean the costs cease, though.

Now, they need to talk to the satellite from earth, and constantly monitor its behaviour. This either requires ground stations of their own — which cost millions of dollars apiece — or rented time on someone else’s by the minute. The data the satellite sends down must be stored and processed, and the more data a satellite generates, the higher those compute costs go.

And then, on top of it all, is a layer of permissions: the right to use radio spectrum, licences to sell imagery, clearances to handle sensitive data, and so on.

This is the story of any space-faring company. This is not an ordinary business. It involves many years of investment, without a rupee in revenue to show for it. Its output, on the other hand, is often just a stream of data with a dashboard. Its only customers are those that actually have the capacity to use that data.

Finding uses is easy; building markets is hard

This makes space a weird business. It is not that their output isn’t useful : space data can tell you incredible things, which would all be massively helpful on the ground. A satellite can spot stressed crops well before the damage shows up on the ground. It can predict major environmental disasters well before they occur. It can tell you things like whether a mining project is risking land subsidence. All of these things have direct commercial value.

And yet, being useful doesn’t mean you will get paid.

A farmer, for instance, would find a satellite’s data enormously useful in all sorts of ways. But farmers don’t contract with space companies. Most regular folk don’t. Chances are, they wouldn’t know what to do with it if they did. The only avenue for selling that data might be to a government agency, or an insurance company that provides crop insurance. These are the only entities with large enough budgets to onboard a space company as its vendor, where their data feeds can simply become one more recurring expense, slotting into existing processes.

If you’re a space company, this is the sort of customer you’re looking for.

Finding such a buyer, however, isn’t easy. For one, there’s just too much free satellite imagery out there. According to one study, the imagery coming out of America’s Landsat program creates over $25 billion a year in value. That is a tremendous resource to have for free. But anyone entering the space business needs to have a value proposition that trumps that. Your data needs to have something extra — it must be sharper, more specific, or more easily available — for it to make a business case better than free archives.

More importantly, for that value to be realised, it needs to integrate into decision-making . Nobody buys data for its own sake. People buy intelligence , to the extent it helps them take better calls — like better decision-making on pricing loans, or better algorithms to settle insurance claims. Unless satellite data is incorporated into those workflows seamlessly, it isn’t really a saleable product.

And so, much of the work of building a space business has less to do with building satellites, and more with the unglamorous labour of integrating their output into software people were already using.

One big customer

Invariably, most space companies chance upon the same answer to this issue: finding an anchor customer — often the government — that can cover most major costs.

That’s the case even in the United States — arguably the world’s most mature space market. In May 2022, for instance, the National Reconnaissance Office, the part of the US government that runs spy satellites, signed massive contracts with three of the world’s biggest commercial imaging companies — Planet, BlackSky, and Maxar. Of these, a single company, Maxar, was given a commitment worth up to $3.24 billion over ten years, with an annual guarantee of $300 million in the first five years. Effectively, a single government agency backstopped an entire industry.

The industry’s economics simply demand such a structure. This business is so expensive, and customers are so hard to land, that your fortunes can depend on whether you can secure one of a handful of government contracts.

Once you do, things can stabilise quickly. A satellite costs roughly the same whether one customer uses it or fifty. If you have one large, committed buyer, everything else can fall into place.

But getting there isn’t easy. The commercial earth-imaging companies that bagged NRO contracts didn’t do so out of nowhere. First, they had to raise money, build constellations, and operate them over years. It was only once they had a track record that they could graduate to these marquee contracts. Maxar, for instance, had been supplying imagery to the NRO for over a decade before the deal fell into place.

That makes space an ugly business. You need to spend your first many years climbing a steep cliff, carrying out rocket science in the face of astronomical costs. Only then does stability arrive. Take Planet, arguably the world’s best known commercial earth imaging company. It was founded in 2010, but only touched profitability fifteen years later, in 2025. For every company that survives this long voyage, many others — capable, space-faring enterprises — die before they can get there.

What India is building

In recent years, ever since the sector was liberalised, India has seen a fascinating new crop of pioneering space companies emerge to the fore. Before they become stable, profitable giants, however, they must first climb that cliff.

Their capabilities are world-class. Many of them have come up with innovations that are global firsts — like Galaxeye’s OptoSAR, or Agnikul’s 3D printed cryo-engines — and have managed to get these into orbit. The data they generate is fascinating. Now, however, comes the challenge of turning those early successes into a business.

There are some nascent signs, however, that they might make that climb.

Last August, IN-SPACe — the body that now authorises private space activity — awarded the country’s first contract to build a national fleet of commercial imaging satellites.

It did not go to a single company. Instead, it pushed four pioneering space companies to form a consortium: Pixxel, KaleidEO, PierSight, and Dhruva Space. Together, these companies shall build a constellation of twelve satellites in the next five years, a project that shall cost them more than ₹1,200 crore. Each of these companies come with complementary abilities: radar sensing, different types of optical imaging, building the platform, and so on. They’re all coming together in a single mission, with no firm owning the whole stack.

The consortium, with IN-SPACe officials

The contract comes with a national mandate, and the government committed as a priority customer. It is the closest thing to a stable foothold the industry has found, so far.

Only, so far, this is nothing like the NRO’s guaranteed multi-billion dollar contracts. There’s no guaranteed check-size for the consortium. In fact, the government offered a repayable loan of up to ₹350 crore to get the project started, but the consortium refused the financing — relying on the backing of funders instead. Ultimately, the consortium will have to build the markets that will make the project viable.

For now, these companies are still finding ways to bridge the gap. Galaxeye, for instance, has signed up with NSIL to distribute the data its satellites generate — using the government as an extended sales arm. Others are opting to sell the picks-and-shovels the industry needs instead. For instance, Dhruva Space — one of the four members of Pixxel’s consortium — builds and sells the satellite platforms and ground systems other operators need.

For all that, though, it’s still early days.

What’s working, and what’s still a bet

That is where, five years in, India’s fascinating new private space industry sits.

It is currently assembling a world-class technological backbone, and making its maiden forays into space. At this nascent moment, it shows a lot of promise.

But space is hard, and so is the space business. The world’s leading space companies took decades to find their footing. That will be true of India as well. These companies all have a long ascent, where revenues will be scarce. They will require patient investment that can wait around for years before the results show up.

There’s an old Roman saying: per aspera ad astra . Through hardship, to the stars.

These companies are clawing their way through hardship. Some day, we hope, they reach the stars.

Tidbits

- India launches a new price stabilization scheme for airline fuel aimed at shielding carriers and passengers from a surge in global fuel costs. The price of aviation turbine fuel (ATF) is now fixed at ₹86.32 per litre for up to three years, taking the effective selling price to ₹115 in Delhi and Mumbai. Those not opting for the scheme can buy it at the international rate of ₹142 per litre.

2.Source:* Business Standard - The CDSCO has flagged the continued detection of banned antibiotics, including chloramphenicol and nitrofurans, in Indian shrimp exports. With major markets like the US, EU, and Japan rejecting consignments linked to over 40 aquaculture farms, the regulator has directed state authorities to tighten surveillance on veterinary drugs to protect India’s seafood export industry.

4.Source:* Business Standard - RBI has increased the investment limits for Non-Resident Indians (NRIs), Overseas Citizens of India (OCIs), and other non-resident individuals to invest in the Indian stock market without requiring SEBI registration. The move is designed to simplify access to Indian equities and attract greater foreign capital by reducing compliance hurdles for overseas individuals who want exposure to listed shares without registering as FPIs.

6.Source:* Economic Times

- This edition of the newsletter was written by Manie and Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaAjay Srivastava on India’s place in the fracturing global trade order

The rules-based world trade order as we know it is fracturing, with weaponized tariffs and every country scrambling to secure its place in the new paradigm. We recently spoke to Ajay Srivastava, founder of the Global Trade Research Initiative and a former Indian Trade Service official, to make sense of how India is navigating this high-stakes shift. Our conversation dives deep into what Trump’s tariffs actually mean for global trade, why Bangladesh massively outperforms India in garment exports despite fewer resources, why India’s software giants haven’t made a serious bet on AI, and the broken links in India’s textile supply chain. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()