Key Objective ~ Summary of the consultation paper

SEBI aims to address risks from sudden price movements causing Out-of-The-Money (OTM) options to turn In-The-Money (ITM) near expiry, which trigger unexpected physical settlement obligations. The proposal seeks to shift ITM single stock options into futures one day before expiry to reduce these risks. Read the consultation paper here.

Background

1. Past Measures and Challenges:

- In 2017, the Do Not Exercise (DNE) facility was introduced to address negative payoffs caused by Securities Transaction Tax (STT).

- Physical settlement for single stock derivatives became mandatory in 2018.

- A change in STT computation in 2019 resolved these issues, leading to the discontinuation of DNE by 2021.

2. Key Risk Identified:

- When an OTM option turns ITM on expiry day, holders face unexpected cash or securities obligations for physical settlement, which can disrupt the settlement process.

3. Interim Measures:

- In 2023, SEBI introduced a Net Settlement Mechanism to combine cash and derivative segment obligations and reduce risks.

- However, this mechanism doesn’t address contracts turning ITM due to price changes during the last 30 minutes (VWAP) of trading.

Need for Review

Key Challenges:

-

Settlement Price Fluctuations:

- The VWAP of the last 30 minutes determines whether options are ITM or OTM.

- This can cause sudden shifts, leading to unpredictable settlement obligations.

-

Net Settlement Limitations:

- While effective during the trading day, it doesn’t mitigate risks from VWAP-based ITM conversions at market close.

-

Risk Concerns:

- Delivery Margins:

- Margins are applied only to ITM options, not OTM options.

- Sudden shifts from OTM to ITM can lead to large, unprepared obligations.

- Systemic Risk:

- Speculative trading or misunderstandings near expiry could increase systemic market risks if obligations are not met.

- Delivery Margins:

Analysis of data between April and September 2024

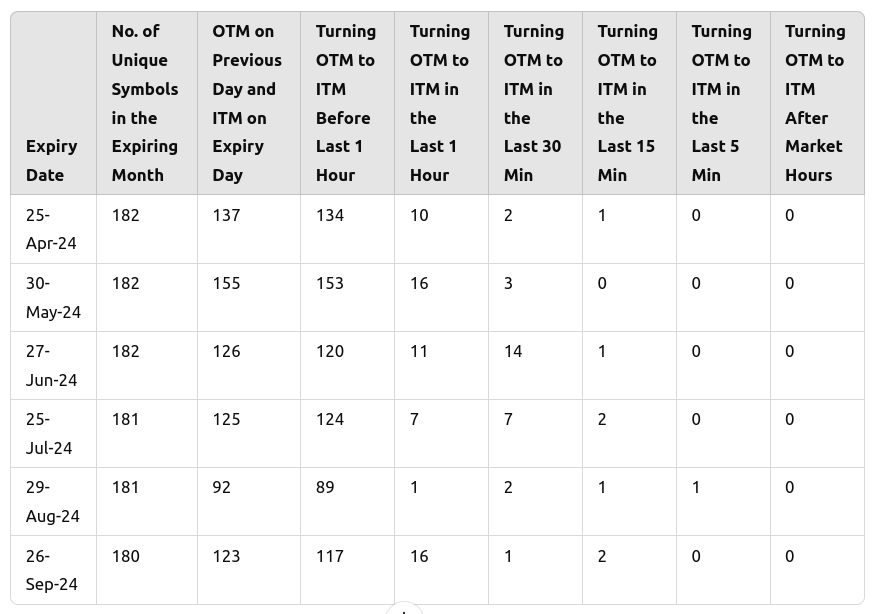

Symbol Wise Data:

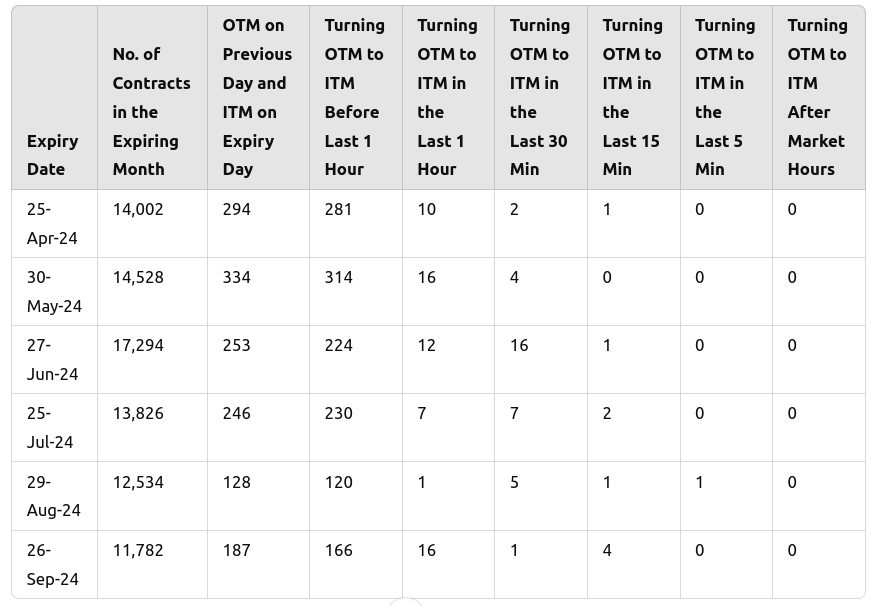

Contract Wise Data:

Observations from the above data:

-

Data Analysis (April 2024 - September 2024):

- No instances of OTM options turning ITM after market hours based on VWAP.

- 10 contracts turned OTM to ITM in the last 15 minutes before market close.

-

Implications:

- While the data shows few occurrences, the theoretical risk of last-minute or post-market ITM conversions cannot be ruled out.

- Such scenarios could lead to systemic risks, especially if delivery obligations trigger defaults by Trading Members (TMs) or Clearing Members (CMs).

-

Proposal Evaluation:

- The DNE facility was considered for options turning ITM due to VWAP settlement price but deemed insufficient to address the issue.

- A key concern is that options ITM at 3:00 PM may turn OTM at expiry, leaving clients with unnecessary stock positions in the cash segment.

-

Request for Re-evaluation:

- The Brokers Forum suggested SEBI revisit the matter, as the current proposals do not fully address the risks or practical challenges of managing last-minute OTM to ITM transitions.

SEBI’s Proposal

1. ITM Options to Futures:

- ITM single stock options will convert into stock futures one day before expiry (E-1).

- These futures can be closed or settled through delivery on expiry day (E).

2. Settlement Mechanism:

- Conversion rules:

- Long ITM calls → Long futures positions. - Long ITM puts → Short futures positions. - Short ITM calls → Short futures positions. - Short ITM puts → Long futures positions.

- Futures will open at the strike price of the exercised options and expire on expiry day (E).

3. Margin Adjustments:

- Delivery margins will apply from E-4 to E-1, as ITM options will convert to futures on E-1.

- Futures will already have sufficient margins on expiry day (E).

You can check the full consultation paper here: