In July, SEBI had released a consultation paper to tighten the rules for trading in the F&O segment on the back of a massive surge in speculation in the markets and to safeguard retail investors.

SEBI has now released a new circular on what all changes will be made and when these will come into effect.

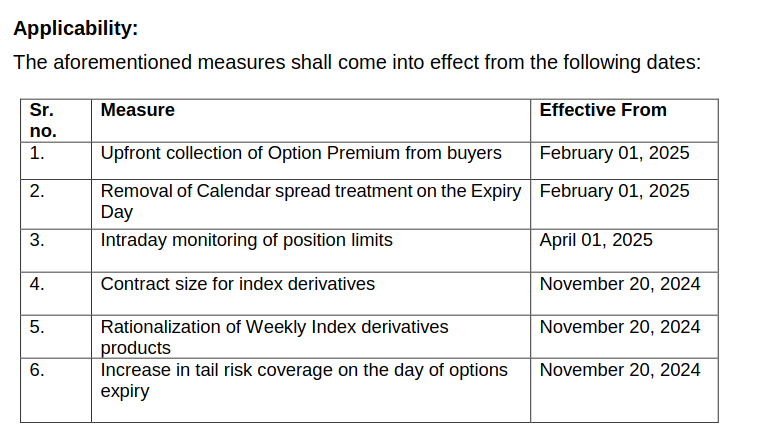

Upfront collection of Option Premium from options buyers

To avoid undue intraday leverage to the end-client, and to discourage any practice of allowing any positions beyond the collateral at the end-client level, SEBI has decided that the upfront margin collection requirement from option buyers shall also include net options premium payable at the client level.

Applicability: Starting from February 01, 2025

Removal of calendar spread treatment on the Expiry Day

Considering the huge volumes witnessed on the expiry day as compared to future expiry days, and the enhanced risk that it represents, SEBI has decided that the benefit of offsetting positions across different expiries (‘calendar spread’) shall not be available on the day of expiry for contracts expiring on that day.

For example: Let us assume the monthly expiry is on the 29th (current month), 30th (next month), and 31st (far month) respectively, then calendar spread positions involving positions expiring on the 29th (current month) and 30th (next month), or 29th (current month) and 31st (far month), shall not be provided calendar spread treatment on 29th (current month expiry). However, calendar spread positions involving positions expiring on the 30th (next month) and 31st (far month) shall continue to receive calendar spread treatment on the 29th (current month expiry).

Applicability: February 01, 2025

Intraday monitoring of position limits

To address the risk of position creation beyond permissible limits, SEBI has decided that existing position limits for equity index derivatives shall also be monitored intra-day by exchanges. For this purpose, Stock Exchanges shall consider a minimum 4 position snapshots during the day.

Applicability: April 1st, 2025

Contract size for index derivatives

In 2015, SEBI set the value of Rs. 5 lakhs and Rs. 10 lakhs as a stipulated contract size for index derivative contracts.

Given that broad market values and prices have increased by around three times in the last 9 years, the lot size will be fixed in such a manner that the contract value of the derivative on the day of review is within Rs. 15 lakhs to Rs. 20 lakhs.

Applicability: Starting from November 20, 2024

Limiting Weekly Expiry Contracts:

Stock exchanges will only be allowed to offer weekly expiry contracts on one benchmark index.

Applicability: Starting from November 20, 2024

Additional risk coverage on Expiry day:

Keeping in view the heightened speculative activity around options positions on expiry days, SEBI has decided to increase the tail risk coverage by levying an additional ELM (Extreme Loss Margin) of 2% for short options contracts.

For instance, if weekly expiry on an index contract is on the 7th of the month and other weekly/monthly expiries on the index are on the 14th, 21st, and 28th then, for all the options contracts expiring on the 7th, there would be an additional ELM of 2% on 7th.

Applicability: November 20, 2024

You can check the full circular here:

Interesting reads:

- @deepak.shenoy tweet thread