SEBI recently published a consultation paper seeking suggestions from the public on the regulatory framework for Micro, Small & Medium Real Estate Investment Trusts (MSM REITs). Some highlights from the SEBI consultation paper ![]()

How does ownership of fractional real estate work?

- In the past 2-3 years, lot of web based platforms started offering fractional ownership of real estate assets like warehouses, shopping centres, conference centres for an amount as low as 10-25 lakhs.

For example, there is a premium office space at a prime location in Mumbai worth Rs. 100 crores. The said office space is already pre-leased by a large multinational corporation(MNC), ensuring a steady cash flow and capital appreciation in the long term.

However, an individual investor with only Rs. 20 lakhs will not be able to invest in this property. Fractional Ownership Platform(FOPs) enable individuals to pool the investible amounts (subject to a minimum amount) with other individuals and jointly own such officespace. As a result, individual investors can invest in the Rs. 100 crore valued office space with an investment of just as low as Rs.20 lakh.

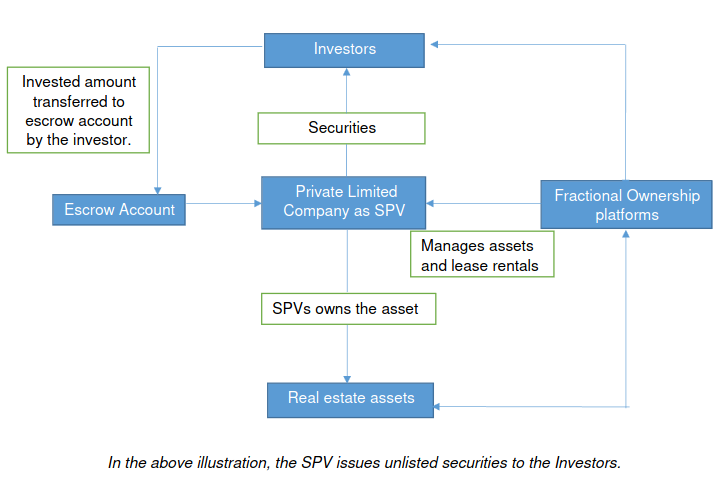

The transaction structure of an FOPs is as follows:

-

The property is first identified by the Fractional Ownership Platform (FOP)

-

The identified property is listed on the website of FOP seeking expression of interest from the public with a token amount ranging from Rs. 10,000 to Rs. 1 lakh.

-

On receipt of 100% expression of interest, the placement memorandum to subscribe to the securities issued by the private limited company ie. SPVwhich will purchase the real estate asset or which own the real estate asset

are forwarded to the investor. -

The investor transfers the amount to the escrow account

-

The investors are allotted the securities

Current Issues:

-

Ambiguous and opaque mode and manner of completion of the purchase/acquisition of the real estate and of issuance of the securities may lead to independent review oversight.Moreover, in case of any infirmity, investors may not have recourse to legal remedies.

-

The lack of standard, uniform selling practices and lack of independent valuation,or of diligence of information or materials provided to potential investors could result in investors falling prey to mis-selling.

- As KYC / AML norms are not applicable to their activities, It represents a risk in combating misuse of identity credentials, could result in camouflaging source of funds and money laundering and represents a risk to the financial system.

- Power of Attorney (POA) structures create a binding liability of the FOP with the owners, who are restricted from independently dealing with their own stake. There is also lack of liquidity if one wants to exit their own stake.

-There is a lack of uniformity of disclosures regarding:

-

The valuation of the real estate.

-

Disclosures made to the investors at the time of soliciting investment.

-

Property title diligence and property title documentation.

-

Lease, rental or tenancy documents and terms arrived at with the lessees/renters/tenants.

-

Continuing disclosures including of receipts of lease payments, due payment of outgoings (including property taxes, electricity or water charges), cancellation or suspension of leases,potential offers for purchase of property by third parties, status of lease renewals, etc

- Disclosure and managing of potential, perceived or actual conflict of Interest by the FOPs/ developer/ tenants etc

Proposed Scope of Regulation:

Cap on total expense:

- To further safeguard the interest of the investors, it is proposed that SEBI will specify the cap on total expense ratio for MSM REITs.

Investor rights:

Right to approve/ remove the Investment Manager,auditor, principal valuer, seek winding up of the scheme, change in investment strategy etc.

Related parties to any particular transaction shall not participate in voting on th\at specific issue.

An annual meeting of all investors is mandatory to be convened to discuss all the relevant matters.

Valuation of assets:

To ensure that the underlying assets of a MSM REITs are valued accurately, a full valuation including a physical inspection of the properties shall be carried out by an independent valuer and NAV of each scheme shall be declared on a quarterly basis for each scheme.

Further, for any purchase of a new property or sale of an existing property, a full valuation shall be required to be undertaken by the valuer.

For any property to be bought/sold >102% or <98% of the value of property as assessed by the valuer respectively, approval from unit-holders shall be required wherein votes cast in favor of the resolution shall be at least 3 times the number of votes cast against the resolution.

Disclosures:

Minimum disclosures will be specified for the annual and half yearly reports to be sent to the investors.

Property wise disclosure of lease rental income along with comparable lease rental income of other similar properties should be disclosed in the offer document for each property proposed to be acquired by the MSM REIT. The above comparable disclosures shall be certified by an independent registered valuer or any other intermediaries specified by SEBI from time to time.

Mandatory registration and regulation of FOPs under REIT Regulations:

All entities will be required to register with SEBI for operating as MSM REIT in the manner specified by SEBI, and shall apply for registration to SEBI in the specified format.

Persons/Entities which either do not meet the eligibility criteria as specified or do not register within the given timelines shall be required to wind-up their operations and cease to operate.

Skin in the game for sponsors:

MSM REIT shall be set up as a Trust and have full control and hold 100% equity in all SPV(s).

The Sponsor(s) shall be clearly identified in the application of registration and in the offer document and shall have at least five years experience in real estate industry as either a developer or a fund manager.

The sponsor shall hold a minimum of 15% of the total units of the MSM REIT for each scheme for a period of at least 3 years from the date of listing of units of a scheme.Any holding of the sponsor exceeding the minimum holding, shall be held for a period of at least one year from the date of listing of such units.

The Sponsor shall have a net worth of at least Rs. 20 crores. Out of the same, an amount of Rs. 10 crores shall be in the form of positive liquid net worth. The

Investment Manager of MSM REIT shall have a net worth of at least Rs. ten crores.

Issue size:

For coming with initial offer of a scheme, the size of the asset proposed to be acquired should be at least Rs. 25 crores and should not exceed Rs. 499 crores

At least 95% of the schemes AUM shall be invested in completed and rent generating real estate properties at all times. The balance five percent can be deployed in liquid assets which are unencumbered.

Distributions made by the scheme of MSM REIT and/or SPV:

SPV to MSM REIT: at least 95% of net distributable cash flows of the SPV shall be distributed to the scheme of MSM REIT.

MSM REITs to unitholders: 100% of net distributable cash flows of the MSM REIT shall be distributed to the scheme wise unitholders.

Fund raising:

- The MSM REIT Scheme shall raise funds from at least 20 investors that are unrelated to the Sponsor, its related parties and its associates.

No Debt:

- MSM REIT Schemes shall not be allowed to raise debt

Minimum and Maximum subscription amount:

The minimum subscription size to the units of a MSM REIT Scheme shall be Rs. 10 lakhs and the unit size shall be Rs. 10 lakhs.

The maximum subscription to an MSM REIT Scheme from any Investor (other than sponsor(s), its related parties and its associates) shall not be more than 25% of the total unit capital.

Benefits of the proposed Regulatory framework:

-

The standard KYC requirements will be applicable while registering clients

-

The Net worth and deposit requirements prescribed for Sponsor and manager will ensure that these platforms have a sound and stable financial health.

- The applicability of code of conduct mandated for Managers will ensure fairness in their dealings with clients.

-

They will be subjected to regulatory inspection and oversight,providing more confidence to investors and hence, will have the potential to attract more investors.

-

Regulated entities in the financial services sector would be able to undertake distribution of MSM REIT.

-

Artificial limitations on the number of investors and creation of SPVs to overcome the limitations will be eliminated.

- Retention of the business potential and opportunities for the FOPs