To make Rights Issues a preferred fundraising mode, SEBI undertook a review of the existing Rights Issue process and suggested the following proposals in its consultation paper, which was released on August 20th, 2024.

Background:

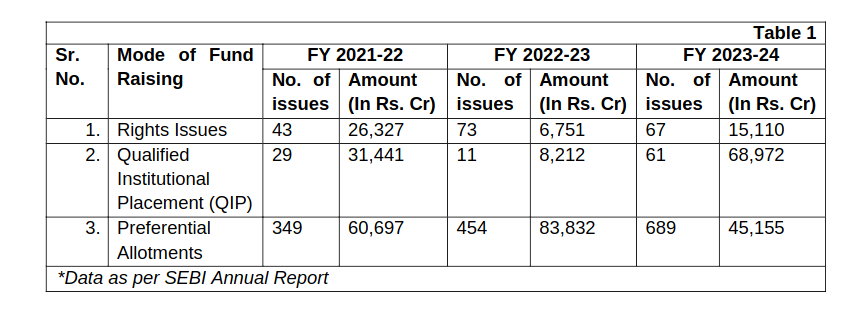

As can be observed from the above data, the amount raised through Rights Issues is lesser than the amount raised through other available modes viz. QIPs and Preferential Allotments. Further, the number of issues through Rights Issues is also substantially less than the preferential allotments due to the following reasons:

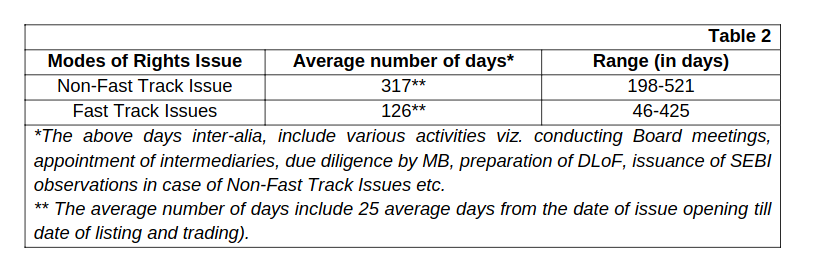

Longer timelines involved in Rights issues:

- In the preferential issue, there is an absence of a detailed document like a Letter of offer (LoF) and the company is required to disclose only brief information regarding the issue.

While the preferential issue process involves shorter timelines, the priority is given to selective investors over the existing public shareholders and this deprives the companies from participating in quick fundraising and also results in dilution of their shareholding.

Considering all the above factors, SEBI has proposed the following in its consultation paper:

Reducing the current indicative timelines of Rights Issue to T+20 working days from the date of the Board meeting approving Rights Issue till the date of closure of Rights Issue.

Discontinuing the current requirement of filing a draft Letter of Offer (DLoF) with SEBI for issuance of its observation and rationalize the content of LoF by requiring to disclose only the relevant information regarding the Rights Issue such as the object of the issue, price, record date, entitlement ratio, etc

Reviewing the role of intermediaries involved in the Rights Issue Process;

It is proposed that validation of applications and finalization of the basis of allotment which is presently carried out by the Registrar to the issue, may also be carried out by Stock Exchanges and Depositories concurrently as RTAs perform certain activities based on the information sought from the Stock Exchanges and Depositories.

As it is already proposed to simplify the content of LoF, the other ancillary activities carried out by the Merchant Bankers (MBs) such as selection of other intermediaries, marketing of the issue, availability of issue material, finalization of basis of allotment, submission of post issue report are generic in nature and can be performed by the MIIs, RTAs and Issuer. Therefore, going forward, there is no need for appointment and due diligence by MB.

Enabling Allotment to Selective Investors in Rights Issue;

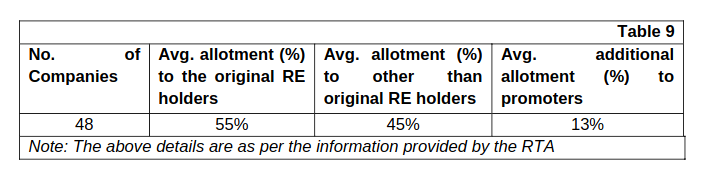

In the last 4 years, in 48 Rights Issues, on average 55% of the rights shares are allotted to original RE holders, and the remaining 45% are allotted to other than original RE holders. This 45% includes shares subscribed by renouncees, additional applications by existing shareholders, and renouncees and promoter’s undertaking to subscribe to the unsubscribed portion. Keeping these factors in mind, SEBI has proposed the following:

-

Relax the restrictions on promoters by allowing the promoter/promoter group to renounce their rights entitlement in favor of any selective investor(s) provided upfront disclosure of the details of such renunciation would be made through advertisement and such selective investor(s) would make the application through ASBA by 11:00 A.M. on the first day of the issue opening period.

-

Allowing the allotment of the unsubscribed portion of the issue to selective investor(s) at the discretion of the issuer, provided upfront disclosure of the details of such selective investor(s) would be made at least two days before the issue opening date along with advertisement as mentioned above.

You can refer to the full consultation paper here: