Objective

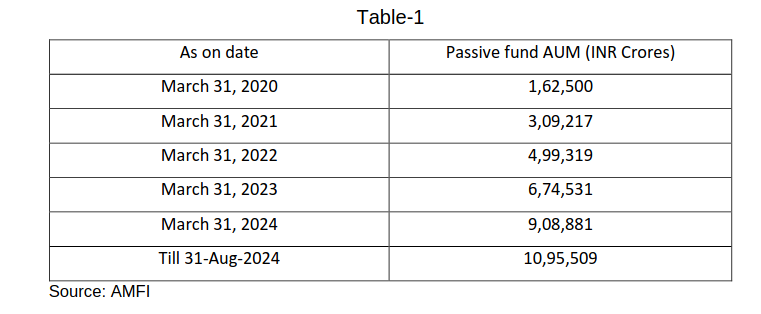

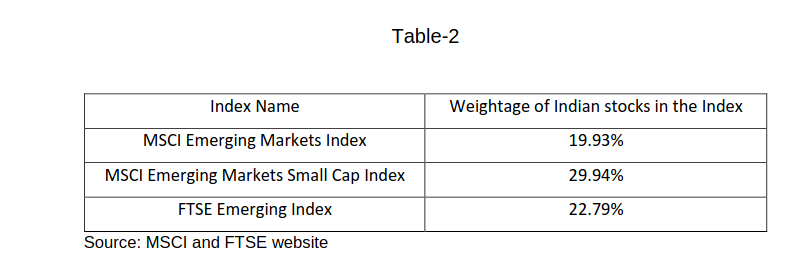

Passive fund investing has grown a lot in India and worldwide, with Indian stocks becoming more important in global indices. However, the Indian market doesn’t allow trades to be done at the exact closing price, causing issues for passive funds and their investors. To fix this, global funds have suggested introducing a Close Auction Session (CAS) to set accurate closing prices, similar to other major markets. This paper shares a proposed plan for CAS and asks for public opinions on how useful and practical it would be for India’s markets.

Current practice in Indian Markets

In India, the closing price of stocks is based on the Volume Weighted Average Price (VWAP) from the last 30 minutes of trading. While this method ensures a fair price, it doesn’t allow buyers and sellers to trade at the exact closing price.

Growth in passive investing

With the growth of domestic passive funds and Indian stocks in global indices, international fund houses highlight that the current closing price method causes price volatility and incomplete large orders, increasing tracking differences, especially on major event days like index rebalancing and derivative expiries.

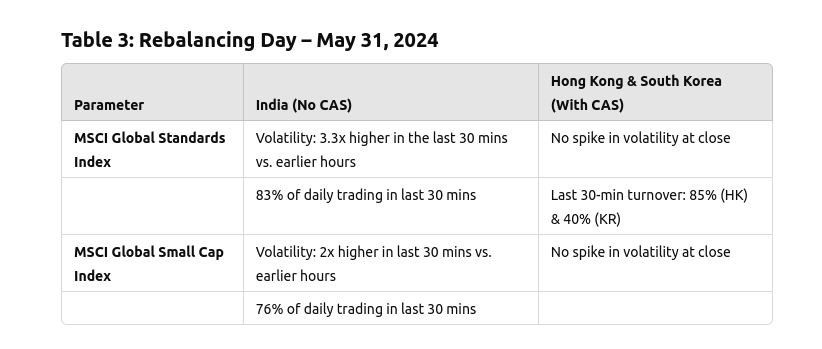

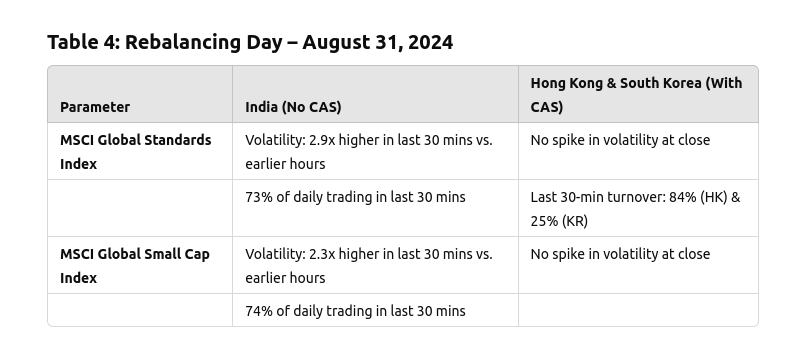

Analysis of volatility of stocks on Index rebalancing days

Key Issues:

- Volatility: The last 30-minute VWAP-based closing price leads to significant price volatility across stocks.

- Tracking Differences: Passive funds face increased tracking differences, especially on major event days (e.g., index rebalancing and derivative expiry).

- Order Completion: High risk of large orders remaining unfulfilled during volatile periods.

Observations on Volatility:

-

NIFTY 50 Stocks:

- MSCI Rebalancing Day (May 31, 2024): Volatility during the last 30 minutes was 1.8 times higher than during earlier trading hours (09:15–14:30).

- FTSE Rebalancing Day (June 21, 2024): Volatility was 1.5 times higher during the same period.

-

Indian Stocks in MSCI Global Standard Index:

- May 31, 2024: Last 30-minute volatility was 3.3 times higher than earlier hours.

- August 31, 2024: Last 30-minute volatility was 2.9 times higher.

-

Indian Stocks in MSCI Global Small Cap Index:

- May 31, 2024: Last 30-minute volatility was 2 times higher than earlier hours.

- August 31, 2024: Last 30-minute volatility was 2.3 times higher.

Analysis of Tracking Differences for Passive Funds on Event Days

Key Findings:

- Domestic Passive Funds:

- NIFTY 50 Index Fund:

- Average tracking difference on rebalancing days (June 2023–July 2024): 0.76 basis points (bps).

- Average tracking difference on other days: -0.12 bps.

- NIFTY Midcap 150 Index Fund:

- Average tracking difference on rebalancing days: -1.46 bps.

- Average tracking difference on other days: -0.09 bps.

- International Passive Fund (Tracking MSCI, FTSE, and S&P Indices):

- Average tracking difference for Indian stocks on rebalancing days: -3.29 bps (July 2023–July 2024).

- Average tracking difference on other days: -0.19 bps.

- Notably, the fund experienced tracking differences across all trading days.

International benchmarking

Major markets worldwide, including those in the Asia-Pacific region, use a closing auction mechanism (CAS) to determine closing prices. An analysis of index rebalancing days (May 31, 2024, and August 31, 2024) showed that markets with CAS experienced no spikes in volatility for stocks added or removed from MSCI indices. In contrast, India, which lacks CAS, observed significant volatility during the last 30 minutes. However, on non-rebalancing days, India’s volatility during the last half-hour was comparable to earlier trading hours, highlighting the specific impact of event days on the current system.

Analysis of Liquidity Patterns in Jurisdictions with CAS:

A study of Hong Kong and South Korea (May–June 2024) shows that the last 30 minutes of the Continuous Trading Session (CTS) before CAS still attract stable trading volumes, accounting for 9%–14% of daily turnover. On event days, such as index rebalancing and derivative expiry, CAS sessions saw a significant surge in trading activity, indicating their ability to centralize liquidity during critical periods without negatively impacting regular trading hours.

Trading Patterns During Index Rebalancing in India:

An analysis of trading during the last 30 minutes on MSCI India Index rebalancing days (February 29, 2024, and May 31, 2024) shows that Foreign Portfolio Investors (FPIs) dominated, contributing 56%–60% of gross traded value in affected stocks. Proprietary and retail investors accounted for 17% and 11%, respectively, while domestic mutual funds contributed 8%–9%. Introducing CAS in India could shift liquidity from CTS to CAS, as FPIs and mutual funds are likely to prefer trading at the CAS-determined closing price. Over time, CAS could stabilize liquidity and centralize trading volumes on event days.

Analysis of Reference Prices and Closing Prices around rebalancing days

An analysis of reference prices (set by CTS) and closing prices (determined by CAS) around MSCI index rebalancing days in Q2 2024 shows significant differences on the rebalancing day. Across various jurisdictions, the average difference between the reference price and closing price ranged from 0.61% to 4.04%. In the 7-day periods before and after rebalancing, the average difference was smaller, ranging from -0.2% to 0.5%. This highlights the role of CAS in capturing significant price adjustments during rebalancing, ensuring more accurate closing prices compared to CTS.

Summary of Proposals for Introducing CAS

The Securities and Exchange Board of India (SEBI) proposes implementing a Close Auction Session (CAS) to determine the closing price of stocks in the equity cash segment. Key aspects include:

-

Introduction of CAS:

- CAS will replace the current VWAP-based method with a call-auction mechanism.

- Initially applied to stocks with derivatives to ensure liquidity.

-

Timing:

- A 15-minute session from 3:30 PM to 3:45 PM.

-

Design Options:

- Four-Stage Design:

- Reference Price Calculation (1 minute).

- Order Input Period (6 minutes).

- No Cancellation Period with Random Close (4 minutes).

- Trade Confirmation and Matching (4 minutes).

- Three-Stage Alternative:

- Reference Price Calculation (1 minute).

- Order Input with Random Close (10 minutes).

- Trade Confirmation and Matching (4 minutes).

- Four-Stage Design:

Table 5: Four-Stage CAS Design

| Session No. | Session Purpose | Start Time | Duration |

|---|---|---|---|

| 1 | Reference Price Calculation | 3:30 PM | 1 min |

| 2 | Order Input Period | 3:31 PM | 6 min |

| 3 | No Cancellation Period with Random Close | 3:37 PM | 4 min |

| 4 | Trade Confirmation and Order Matching | 3:41 PM | 4 min |

Table 6: Three-Stage Alternative Design

| Session No. | Session Purpose | Start Time | Duration |

|---|---|---|---|

| 1 | Reference Price Calculation | 3:30 PM | 1 min |

| 2 | Order Input Period with Random Close | 3:31 PM | 10 min |

| 3 | Trade Confirmation and Order Matching | 3:41 PM | 4 min |

-

Price Limits:

- Stage 1 (Order Input): ±5% of Reference Price.

- Stage 2 (No Cancellation/Random Close): Limited to highest bid and lowest ask at the end of Order Input.

-

Equilibrium Price:

- Determined based on maximum executable volume.

- In cases of ties, preference is given to the price closest to the Reference Price or the Reference Price itself.

-

Order Execution:

- Limit orders are prioritized over market orders, with execution following price-time priority.

-

Integration with CTS:

- Unexecuted CTS orders can carry over to CAS but are treated as limit orders within CAS price limits.

-

Post-Close Session:

- Discontinued, as CAS will fulfill the need for trades at the closing price.

You can check the full consultation paper from SEBI here: