Context

Current regulations don’t differentiate between active and passive funds regarding entry barriers and compliance requirements.

Considering the lesser risk inherent in managing passively managed MF schemes, the proposed MF Lite Regulations intend to reduce the compliance requirement, foster innovation, encourage competition, and promote ease

of entry for the MFs interested in launching only passive schemes. the proposals related to the introduction of a relaxed regulatory framework in the Mutual Funds (MF) segment viz, “the MF Lite Regulations” for the passively

managed MF schemes are as follows:

Summary of the SEBI’s consultation paper

Eligibility Criteria for a Sponsor according to the consultation paper seeking registration under MF Lite Regulations:

1. Main Eligibility Route

Sponsor Requirements:

- Positive net worth (N/W) for the preceding 5 years.

- Positive liquid N/W exceeding the proposed capital contribution in the AMC.

- In the case of AMC control change due to share acquisition, the sponsor must have a positive liquid N/W or tied-up funds covering the higher of aggregate par value or market value of the shares.

- Net profit after tax in 3 out of the last 5 years, with an average profit of at least INR 5 crore.

AMC Requirements:

- Minimum N/W of INR 35 crore (reducible to INR 25 crore with 5 consecutive years of profit).

- N/W to be deployed in liquid assets.

- Sponsor to hold a minimum of 40% of the AMC’s N/W and maintain the AMC’s positive liquid N/W

2) Alternate Eligibility Route

If the main criteria are not met, sponsors can apply under alternative criteria:

- Adequate capitalization of the AMC with a minimum N/W of INR 75 crore.

- Initial sponsor shareholding equivalent to INR 75 crore to be locked in for 3 years.

- The combined experience of AMC’s CEO, COO, CCO, and CIO to be at least 20 years. A separate Chief Risk Officer (CRO) may be appointed.

- In case of existing AMC acquisition, specific capitalization and shareholding requirements apply

Shareholding and governance in Mutual Funds

According to current regulatory requirements, a sponsor of a mutual fund, its associate, or group company, including the Asset Management Company (AMC), cannot hold 10% or more of the shareholding or voting rights in the AMC or trustee company of another mutual fund. Additionally, they are prohibited from having representation on the board of the AMC or trustee company of any other mutual fund. Furthermore, any shareholder with 10% or more of the shareholding or voting rights in an AMC or trustee company of a mutual fund is also restricted from holding 10% or more of the shareholding or voting rights in the AMC or trustee company of another mutual fund or having representation on the board of the AMC or trustee company of another mutual fund.

SEBI’s proposal suggests the following:

- New players can launch passive MF schemes under MF Lite Regulations.

- Existing MFs can separate passive schemes into a different entity within the group.

- Resources must be segregated for passive and active MF management.

- The new entity can retain past track records of hived-off passive schemes.

- A sponsor can have up to 2 registrations for active and MF Lite.

- Existing AMCs moving passive schemes cannot launch new passive schemes.

- Shareholders with 10%+ ownership can hold the same in the new AMC.

- AMC should provide an exit option to existing investors for hived-off passive business

Role and responsibilities of trustees

- The existing roles and responsibilities of trustees regarding related party transactions, conflicts of interest, undue influence of sponsor, mis-selling, misconduct including market abuse/ misuse of information including front running, etc. are kept as per the existing MF Regulations.

- A debenture trustee can oversee multiple MFs under MF Lite but must be independent.

- The trustee of an MF Lite must be registered under SEBI (Debenture Trustees) Regulations, 1993, meeting fit and proper criteria.

- Existing trustees can be appointed for MF Lite if passive schemes are moved within the same group.

- Trustee responsibilities include safeguarding funds, ensuring compliance, and acting in the interest of unitholders.

- Specific trustee duties will be mutually decided with AMCs, with oversight over AMC activities.

- AMFI and SEBI may prescribe a standard trust deed for MF Lite.

- Trustees can request information from AMCs, sign investment management agreements, and take remedial steps if needed.

- Trustees review complaints, can initiate scheme winding up, and must inform SEBI of any detrimental acts.

- Audit and Risk Management Committees may not be mandatory for trustees.

- Trustees are not required to employ dedicated personnel.

- AMCs’ boards are appointed by sponsors, not trustees.

- Trustees must approve changes in AMC control.

- Reduced trustee roles apply to existing AMCs managing passive funds under current regulations

Restrictions on business activities of AMCs

The entities registered under MF Lite may not be allowed to do any business activity other than managing passive MF schemes as MF Lite Regulations are proposed to be lighter as compared to the same for the existing AMCs

.

Investment Management Agreement

The details of the investment management agreement in respect of the MF Lite framework shall be specified by AMFI, in consultation with SEBI.

Advertisement Code

The advertisement code details may not be needed. It is enough to ensure that ads for passive investment schemes are not misleading or promote mis-selling. Advertisements for passive schemes must follow offer documents and SEBI’s specified guidelines.

Risk Management Committee (RMC) for oversight of risk at AMC level

As per the existing risk management framework of MFs, both the AMC and the

trustees are mandatorily required to have separate RMCs where RMCs review and suggest long-term risk solutions annually and CRO of MF is part of both RMCs, reporting to AMC boards and trustees.

As per the new proposal:

- For passive schemes with lower risks, the RMC role may be limited.

- WG suggests that the Audit Committees can handle RMC’s responsibilities.

- Proposed: Audit Committee and RMC for trustees may not be needed.

- Proposed: RMC at AMC level may be optional, with Audit Committees taking on RMC role for MF Lite.

Transactions through an associated broker

The current limit of 5% at the AMC level for the purchase or sale of securities through an associate broker may be extended to 10% in the case of an associated broker and to 25% in the case of a non-associate broker, for all entities under the MF Lite Regulations.

Simplified Scheme Information Document (Simplified SID)

As per the latest SEBI Circular dated November 01, 2023, the SID filing format has been simplified for all schemes. Considering the limited risks associated with passively managed schemes, the format for draft SID for passive schemes is proposed to be further simplified.

SEBI Suggests making fast-tracking of SIDs mandatory for passive schemes by AMCs under MF Lite Regulations.

The proposed modifications vis-à-vis the current prescribed format of SID include the following:

-

Remove non-relevant parameters such as investment strategy, instruments in which schemes shall invest, performance of the scheme benchmark, etc. from SID for passive schemes.

-

Include key parameters like tracking error, tracking difference, name of the underlying benchmark, specific attributes of target maturity debt passive schemes such as lock-in period, maturity of the target duration fund, etc. which are important parameters to be understood in the “Highlight Section”.

-

Provide a web link for additional details like NAV, and risk factors.

-

Relax separate filing of Key Information Memorandum (KIM).

Submission of trustee report to SEBI

As per the existing MF Regulations, the trustees are required to submit half yearly Trustee Report (HYTR) to SEBI in a specific format.

Submission of trustee report to SEBI may be discontinued considering the limited role of trustees in the case of MF Lite.

However, since the Board of AMC shall have the primary accountability of acting in the interests of the investors, the Board of AMC shall submit a Yearly AMC Report (YAR) in the case of MF Lite.

Section II

Section II of this consultation paper deals with the proposals about ease of compliance, relaxed disclosures, and other regulatory requirements for passive schemes under existing MFs as well as schemes that may be launched under the MF Lite registration. This will ensure uniform applicability of the proposed MF Lite Regulation and provide a level playing field across the passive MF industry.

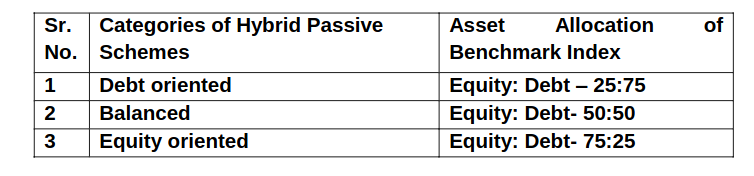

Introduction of Hybrid ETFs/ Index Funds:

The Working Group highlighted that current regulations allow passive funds to replicate either a debt index or an equity index, without provisions for replicating a hybrid index combining both debt and equity. They suggested that including this option could enhance flexibility and diversification opportunities in the passive mutual fund sector.

To begin with, only 3 sets of hybrid passive schemes shall be permitted with the following features:

The proposed framework for hybrid passive schemes is as under:

- Each mutual fund can introduce only one hybrid fund in a particular category.

- The minimum initial investment for Hybrid ETFs/Index Funds is INR 10 Crore.

- The issuer of the ETF/Index Fund must ensure that the asset allocation between equity and debt in all Hybrid ETFs/Index Funds complies with regulations at the end of each calendar quarter.

- Sectoral/Thematic funds and Target Maturity Funds cannot be used for the equity and debt components of Hybrid passive funds.

- Hybrid ETFs can reveal the indicative NAV (iNAV) at least four times daily: at opening, closing, and twice in between, with a minimum 90-minute gap between disclosures.

Investor education and awareness

As per the existing rules:

- Mutual Funds/AMCs must allocate a minimum percentage of assets for investor education annually.

- Half of this amount goes to AMFI for industry-wide awareness.

- For ETFs/Index Funds, 1 bps of daily net assets is set aside within TER.

- No such requirement for FoFs investing over 80% in domestic funds.

Considering the limited spread available in charging TER in passive funds, the requirement for setting aside for investor education and awareness may be relaxed for MF Lite.

Proposed provisions for allocating funds for investor education:

a. Domestic Fund of Funds (investing >80% in domestic passive fund) - No requirement

b. ETFs/Index Funds/Overseas FoFs investing in underlying ETFs:

- AUM up to INR 250 Cr. - No requirement

- AUM beyond INR 250 Cr. - 5% of TER for direct plans, capped at 0.5 bps of AUM.

Investment and trading in securities by the employees of the AMC(s) and Trustee(s)

The working group suggested that instead of getting approval, employees should inform about their transactions in advance. They propose that employees must give a prior intimation at least 3 working days before the transaction. Additionally, the rule to report these transactions within 7 working days will remain in place.

Portfolio Disclosure

The WG discussed current MF portfolio disclosure rules:

- Debt schemes: Fortnightly within 5 days of every fortnight

- Other schemes: Monthly within 10 working days of each month

- All schemes: half-yearly within 10 working days of the end of the half-year

Proposed changes for passive funds:

- Debt and hybrid passive schemes: Monthly within 10 working days of each month

- Equity passive schemes: Quarterly within 10 days from the close of each quarter

The separate half-yearly disclosure for passive funds may be eliminated as it’s covered in the monthly and quarterly disclosures.

Unaudited Half-Yearly Financials

The requirement for publishing unaudited half-yearly financials shall be discontinued.

However, the annual report of the schemes under MF Lite shall continue to include the above details.

Investments by passive schemes

Passive schemes may not be allowed to Invest in:

- Unlisted debt instruments

- Bespoke or complex debt products

- Securities with special features

- Inter-scheme transactions

- Short selling

- Derivatives (except for portfolio rebalancing)

- Unrated debt and money market instruments (except Gsecs, Tbills, and other money market instruments)

-

Provisions for Interval schemes, Capital Protection oriented schemes, Real Estate MF schemes, and Infrastructure Debt Fund Schemes may not apply to the MF Lite regime.

-

Stress testing for debt funds and liquidity risk management framework may remain inapplicable for passive funds under the current setup.

Tracking difference for equity-oriented passive schemes:

Current regulations mandate Tracking Error (TE) below 2% for equity passive funds and Tracking Difference (TD) disclosure. For debt passive funds, TD must be below 1.25% with TE disclosure.

The proposed change suggests introducing TD requirements for equity passive schemes. While the maximum Total Expense Ratio (TER) allowed is 1%, actual TER in such schemes is typically lower. The proposal aims for equity ETFs/Index funds to maintain TD below the lower of 1.5 times the TER or 1.25%.

Disclosure of “Debt Index Replication Factor (DIRF)” in debt-oriented passive schemes

At present, corporate debt ETFs/ Index funds comprising only corporate debt securities are considered to be replicating the underlying debt index provided Investment in securities of issuers accounting for at least 60% of weight in the index, represents at least 80% of net asset value (NAV) of the ETF/ Index Fund subject to certain relaxations in duration and rating.

Similarly, debt ETFs/ Index Funds based on G-sec, T-bills, and SDLs are also considered to be replicating the underlying index subject to certain relaxation in the duration of the portfolio w.r.t its benchmark. Therefore, the debt-oriented passive schemes are not required to fully replicate the underlying index.

As per the proposal, Debt-oriented passive schemes may also be mandated to disclose the “Debt Index Replication Factor (DIRF)” of the underlying index by the portfolio along with the TE and TD on AMC’s website.

For this purpose, 100% replication at the individual issuer level shall be achieved if the portfolio has the same issuer in the exact same percentage as is the case for the Index.

DIRF shows how closely the portfolio mirrors the index at the issuer level. It calculates replication based on individual issuer weights compared to the index, aiming for transparency in replication accuracy.

Introduction of close-ended debt passive schemes

Currently, target maturity debt passive schemes exist where the fund’s index matures on a specific date and the fund expires.

These schemes are open-ended, allowing investors to subscribe or redeem at any time.

- Proposal: Introducing the option to launch close-ended debt passive schemes.

Categories of schemes under MF Lite Regulations

The WG was of the view that there can be two approaches towards allowing the passive schemes to be launched under the MF Lite Regulations. The two approaches are proposed as under:

Approach 1:

Implementation of Approach 1 will be gradual and will involve SEBI listing domestic equity passive indices whose quantitative threshold/ AUM exceeds a minimum threshold of either INR 10,000 Cr. or INR 5,000 Cr. or with no threshold.

Overseas indices allowed as per the consultation paper can also be included in Phase 1.

Only specific target maturity and target duration debt passive schemes meeting certain criteria will be considered in Phase 1.

AMFI, in consultation with SEBI, will prescribe the list of equity and debt indices for this approach.

Approach 2:

The implementation may not be phased, and all current ETFs, Index funds, and domestic and overseas FoFs investing in a single ETF/Index fund can be included in the MF Lite regime.

New equity passive schemes can be launched with indices not in existing schemes, subject to a list prescribed by AMFI in consultation with SEBI.

For debt passive schemes, the existing rule requiring AMFI to list indices, as specified in the Master Circular on Mutual Funds, will continue to apply.

You can read the full SEBI Consultation paper here :