To facilitate greater transparency and benefits of economies of scale to investors, SEBI recently published a consultation paper on review of Total Expense Ratio (TER) charged by AMCs to unitholders of schemes of Mutual Funds, Here are some of the key highlights of the proposals made by SEBI in this regard:

1. TER limit inclusive of all expenses and charges

In view of the underlying principle that Total Expense Ratio (TER) should be inclusive of all costs charged to an investor, it is proposed that:

-

Brokerage and transaction expenses may be included within the TER limit and the transaction wise limits prescribed for additional expenses towards brokerage may not be applicable bringing in much needed transparency in the costs charged to unitholders.

-

To save brokerage and transaction charges, AMCs can now get limited purpose membership with stock exchanges for executing trades for their own mutual fund schemes.

2. Additional commission to distributors

-

The additional commission to distributors may continue for inflows from B-30 (Beyond Top 30) cities at a fixed rate of 1% of the size of the 1st application or amount committed through SIP of the individual investor, subject to a maximum of Rs. 2000/ -

-

The provision enabling charging of additional expense of 5 bps for schemes having provision of exit load, may be discontinued

3 Discontinuation of charging additional 5 bps to the scheme having exit load

- Considering that for more than 10 years AMCs have been permitted to charge additional expenses, it is proposed that the provision enabling charging of additional expense of 5 bps for schemes having provision of exit load, can be discontinued.

4. (GST) on Investment and Advisory Fees

- Considering the overall intent of increasing transparency in expenses charged to unitholders by making TER inclusive of all charges, it is proposed that TER may be inclusive of GST on investment and advisory fees as well.

5. Review of slab wise TER structure

While the TER slabs are presently based on the AUM of the schemes, the AMCs enjoy economies of scale which is linked to their asset class levels and not schemes. The manpower for research and other core activities of AMCs

may be different for equity and debt products but every new scheme does not necessarily attract additional spending towards the core activities by AMCs.

Considering the above points:

I. The TER slabs should be at the level of the AMC and not at the scheme level.

ii.AUM of open-ended schemes, wherein slab based TER is presently applicable, may be bucketed into Equity based AUM (equity & equity related instruments) and other than equity based AUM of the AMC (other than equity & equity related instruments).

iii. Since Overnight funds of AMCs invest in securities with maturity of 1 day, TER rate derived based on allInvestments other than equity & equity related product shall be the maximum TER for Overnight funds.

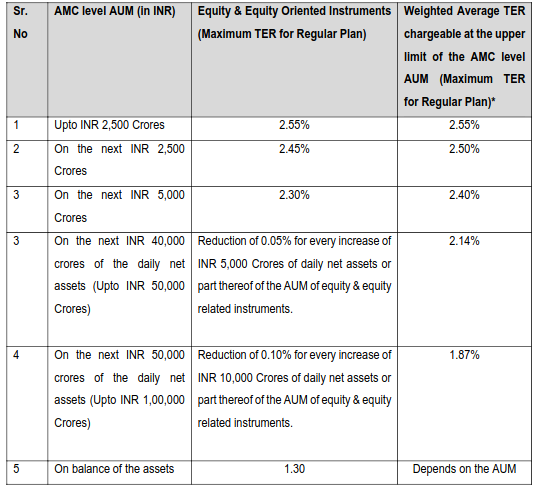

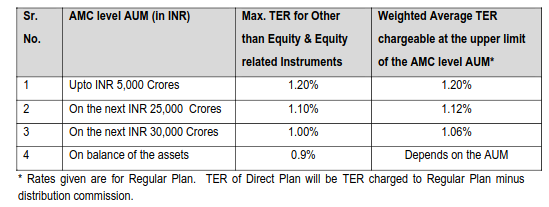

6.Revised TER limits

For equity schemes:

For schemes other than equity:

- The revision in TER is proposed for Active Open ended schemes and no change is proposed for TER of passive schemes (Index Funds and ETFs)

7. Commission/fees paid to distributors

- As transaction charges to be paid to distributors, AMCs are presently permitted to deduct transaction charges of Rs 100/- for existing investors in a Mutual Fund and Rs. 150/- for first time investors in Mutual Fund per subscription of Rs. 10,000/- and above from the subscription amount of the investor.

It is proposed that payment of upfront commission by investor directly and transaction costs deductible from investments of investors , may not be permitted.

8. Expense Ratio of Fund of Fund(FoF) Schemes

- To facilitate AMCs to launch FoFs on low cost international funds, it is proposed that:

For schemes investing only in international funds,the TER over and above the weighted average of the TER of the underlying scheme(s) shall not BE 2 times higher than the weighted average TER levied by the underlying scheme(s) and others cost including distribution commission of not more than 50 bps but excluding AMC Management Fees.

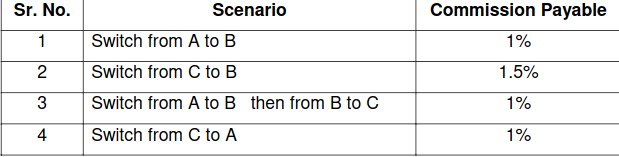

9. Switch Transactions and Distributor Commission

To discourage churning / mis-selling by distributors, it is proposed as under:

- In the case of a switch transaction, the distributor shall be entitled to lower of the commissions offered under the two schemes of any switch transaction.

For example, if the distribution commission offered by AMC for Scheme A is 1%, Scheme B is 1.5% and Scheme C is 2% the entitlement of commission for switch transaction will be as under:

- Mandate one of the following:

I. The commission to distributor should be in increasing trend with the first year’s commission not being more than 25% committed to the distributor for first three years, OR

Ii. The commission paid to distributor should be equal for all years.

10. Exit Load

It cannot be denied that the early redemption by investors from the scheme has an impact on other holding investors and exit load discourages early exit from the scheme. Also, it is observed that Mutual Funds generally charge one to two percent as exit load. In view of the same and considering that exit load is credited back to the schemeIt is proposed that:

The exit load of an open ended scheme may be lowered to a maximum permissible limit of 2%

11. Issue and Redemption expenses of the scheme

MF Regulations may be appropriately amended to state that any expense other than those specified in MF Regulations, including initial expenses of launching schemes, shall be borne by the AMC or Trustees or Sponsors.

To amend the MF Regulations to clarify that after the announcement of winding-up of the scheme, Only recurring expenses can be charged to the scheme/investors) which pertain to winding up of a scheme.

12. Performance based TER

The underperformance of regular plans of schemes is higher as compared to direct plans. As per the data, more than 22% of the regular plans of schemes have underperformance of more than 1.25%(equivalent to max. tracking difference permissible for debt ETFs/Index Funds)

As any significant underperformance of the fund versus its benchmark is not in the interest of unitholders and AMCs outperforming the market may find merit in charging unitholders with performance linked TER, the concept of variable TER based on performance of the schemes can be thus explored in the following ways:

Approach A:

During the period in which the investor remains invested, the base expense ratio may be charged to the investor. At the time of redemption, the management fees may be charged if the return of more than the indicative rate is generated or annualized returns received by the investor are above the hurdle rate. The maximum management fees may also be specified to discourage fund managers from taking imprudent risk in order to earn higher Fees.

Approach B: Higher expense limit for performance based TER may be fixed and TER inclusive of management fees is charged to the investor.

The TER charged by the schemes in such cases should be based on the schemes’ performance during the previous year.

At the time of redemption by the investor, if AMC fails to generate return above the Indicative returns for investor or the annualized returns for the investor is below the hurdle rate fixed in advance, the AMC may retain base TER as may be applicable and return the remaining expenses charged to the investor, along with the redemption amount.

- It will be optional to the AMCs to offer such a scheme(s).

13. Financial inclusion of women in Mutual Fund space

-

To encourage more participation from women, An additional commission to distributors may be fixed at 1% of the investment amount of the 1st application or amount committed through SIP of the woman investor at industry level, subject to a maximum of Rs. 2000/- per investor.

-

As similar incentive is also available for B-30 city investors, it shall have to be ensured by AMCs that the proposed incentive for women investors is extended only in those cases where B-30 incentive is not given.