We don’t know what’s the truth here but generally we need to extra alert while investing in stocks like this as they say “there is no smoke without fire”

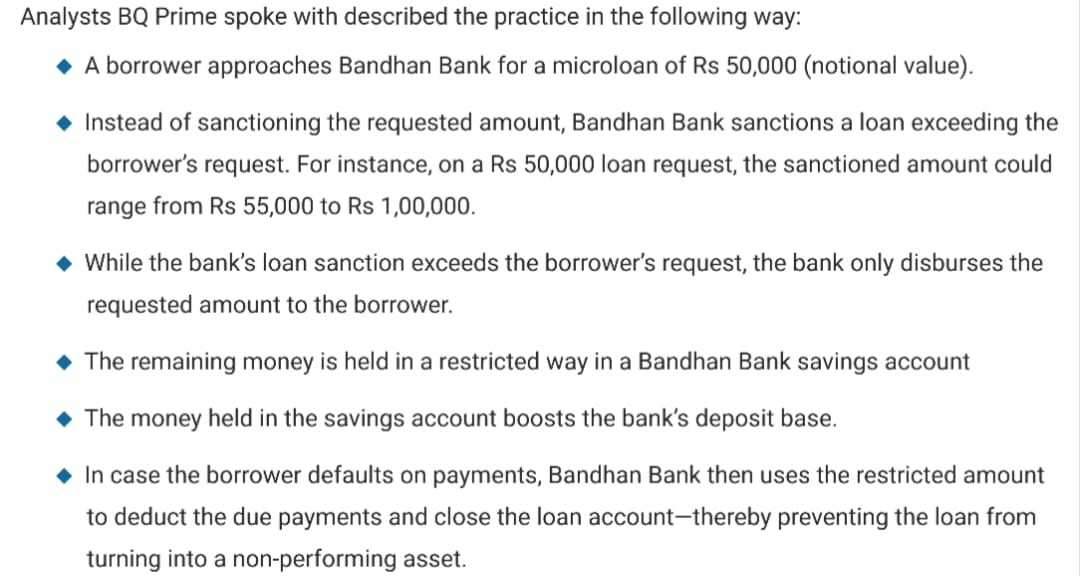

The peculiar—and somewhat brazen—growth hack

helps the bank artificially boost its deposit base

and also delay recognition of loans that have turned sour

Yes. Nice way to increase a deposit base i guess.

Even if legal, definitely sounds shady.

Also, while the bank can temporarily continue repayments of loan EMIs

from the additional amount they initially sanctioned (but not disbursed).

But, if the borrower is not repaying they loan EMIs,

then the scheme is eventually bound to fail

and the loan is officially an NPA (non-performing asset).

Hence, i fail to understand the following bit (added emphasis) in the article summary…

In case the borrower defaults on payments,

Bandhan Bank then uses the restricted amount to deduct the due payments and close the loan account

—thereby preventing the loan from turning into a non-performing asset.

How, can a loan be fully repaid (to close the loan account) by using funds sanctioned in the loan itself ?

Where does the additional payment of interest due come from? Is that something the bank writes-off? (i.e. NPA)

Fully agree, the loan cannot be closed. All this can do, is give the customer a lag that monthly insallments can be settled using this money until what is available in the SB account is exhausted, but this cannot result in loan account being closed.

Something similar which banks used to do is, evergreening of a loan, when one loan gets into default, give a new loan and close the old one. By doing this, the provisioning could be extended. I believe Yes bank Rana Kapoor was known for doing this. He used to charge exhorbitant fees for doing this. The advantage of charging fees is that the entire money is treated as income. This will increase the bottom line. This is apart from taking his own pound of flesh from the customer outside the banking system.

I am sure you are joking. It cannot be done. If they do reversal, then it will be reflected in the customer statement and there will be a hue and cry, of course, interest will hit the account for the additional drawdown by the bank. If they do back value reversal, the interest will not get hit, but this will show in the statement. Also any reversal done which crosses financial period will be an issue.

I know RMs who request people who have OD to draw and put it in the account and the accrued interest for one day is paid by the RM. This is done for RM meeting his target. But never heard Banks doing this by default.

You know I shouldn’t have said it in the first place. Sadly. That’s the reality.

You think this is done with small accounts? It’s done with the permission of the customer only.

Nah. It won’t make a difference.

Ah. Should have read this para first. I always reply line by line. Yes. This is done.

I have myself identified such things at the time of audit. As a statutory auditor it’s very difficult to track such things since the routing is done that way.

Right… your observation is correct. on the face of it, story does not add up… its fallacy to use the same loan to prepay the loan

All this can do, is give the customer a lag that monthly insallments can be settled using this money until what is available in the SB account is exhausted,

or

What Bandhan bank could do… (in theory) force client to open one interest free current/saving account with Bandhan and and use the balance in current account to reduce interest amount. This is good for customer as loan prepayment happens at faster rate and good for bank as deposit/saving number improves.

This is similar to what banks offer for home loan variation. Home saver/ home max gain.

So should be perfectly legal… if this is the structure.

BTW for that matter I discovered terms and conditions of a nationalized bank offering home save/max gain highly corrosive/misleading. if one of the largest bank can get away with misleading T&C for home loans, everything else looks fair.

When a home loan is granted, a customer is supposed to open a SB account as well - Is this not the practice. If not how will the funding to the loan account happen i.e repayment of EMI. The emi will be a standing instruction - is it not.

Few years back, dont remember which bank, they allowed, interest offset by the amount of credit balance in the funding account. There was no actual settlement to the loan, all the customer need to do is just keep funding the SB account and maintain it and the system will automatically offset the balance for interest purposes. I think it was Federal Bank, not sure. This was great for customer whos salary etc comes to the account and earns only small interest rate and remain in the bank account for longer period.

Then this is legit. Why should the bank take the burnt if some RM or Branch manager is doing this. Also there is no reversal, Customer transfer on 31st from OD to SB account and then does another transfer from SB to OD on the 1st. Both the transactions are done by the customer. Accrued interest gets debited for one day but the RM or whoever settles it off record.

This is something which Karvy tried I guess, convince the demat holders who never did any transaction to lend their shares for a fee. Dont remember the modus operandi but remember something like this. The greedy investors to get the additional fee agreed and then got into trouble.

Opening SB account is not mandatory. My father has home loan with BOB but no SB account with them. Bank has taken post dated cheques of his HDFC account for EMI payments and encash a cheque every month.

This is just an observation, do cheque clearing happen same day? If so then there is no issue, in the past it would take one to two days for the cheque to be cleared and this could lead to additional interest on the loan.

I think currently bank does image clearning and hence settlement happen on the same date.

I thought the lending bank would insist on SB account when a loan is given.

Bob did insist on sb account but my father resisted and the branch officials finally gave up and asked for PDCs for the entire 180 month loan term. For that he got 10 cheque books of 20 leaves each and wrote the cheques. HDFC levied some charges for issuing multiple cheque books at the same time which I’m not aware of.

Bob puts up cheque on last working day of month and usually it gets cleared in 2-3 days.

Think about this - 180 month term loan.

On an average 2 days it takes to clear the cheque i.e 2 days x 180 months = 360 days.

Your father is paying extra interest for 360 days as the payment mode is cheque (clearing delays). If he had an account with BOB, he could transfer the money by IMPS or NEFT to bob account and the same day, the Standing Instruction will settle the dues and loan outstanding will be reduced.

Not sure if the above calculation is correct but you could think in this direction.

You’re right. But he has some bad experience with Bob earlier in his young age so he is not ready for it. He reluctantly took loan from there as the builder who sold us apartment had tie up with only Bob that time. Later he got PNB, Allahabad Bank, LICHFL as well on board but that was only after our deal was done.

It’s legit. But doesn’t it give wrong picture to the investors? Deposits grown by 20 precent. Advances also grown by 20 percent. Bank is growing and all of it.

Agreed. When Corporate Customers have payments (small corporates), close to the year end, they try to delay it so that their balance sheet show better cash position. This happens.

What was concerning was I thought the Banks at the management level, were using their systems to draw the undrawn portion crediting it to the account and then reversing it.

During March I got 5 calls on one single day from one bank to park some money before the year end. Each one did not know that the other was calling and everyone said she/he was my RM. I felt angry and sad. Called up the branch manager and he said that the target is so high that the staff will call anyone.

I pity the branch manager, they even go personal and say “Can you please help me” in moving float balance from other bank to their bank. RMs who are very close relationship will customer will seek to transfer the unused OD balance, but the RM will be the slave of the customer as he can use it against him

Most of the businesses have some or the other shady element but how the market perceives is what matters for an investor. It will take a decent amount of time before investor confidence is back in banks like bandhan.

I haven’t detected anything like this before. So I will believe it’s not done. Why doubt everything in the system.

This is normal for me too. Not just year end, I get calls every month end also. I did help them couple of times because I had extra funds in my trading account and month end was Saturday. So I withdrew the funds on Friday from zerodha, it hit the account on Saturday and Monday I withdrew all back to trading account. For doing this they treat me like God. So I can imagine the pressure they have to meet targets.

FY end also they asked me but I told them, 31st was Friday, and even if I place withdrawal request it will come only on 1st April.

yes… many banks offer this kind of home loan with different names like max gain, super saver. This facility is good for business class also where in current account money is used to reduce interest burden leading faster prepayment.

My guess is Bandhan bank would be offering similar facility for business loan. Its win win for both bank and customer and (should be) legal. Again its just guess… we do not know what is truth. Anyhow the as @cvs pointed out the allegation itself is bizarre, we can always run our imagination horses to come up with theories what could have actually happened.