Alright, here we go!

I have been trying to wrap my head around the topic of SGB taxation for a long time, though I don’t own any SGB.

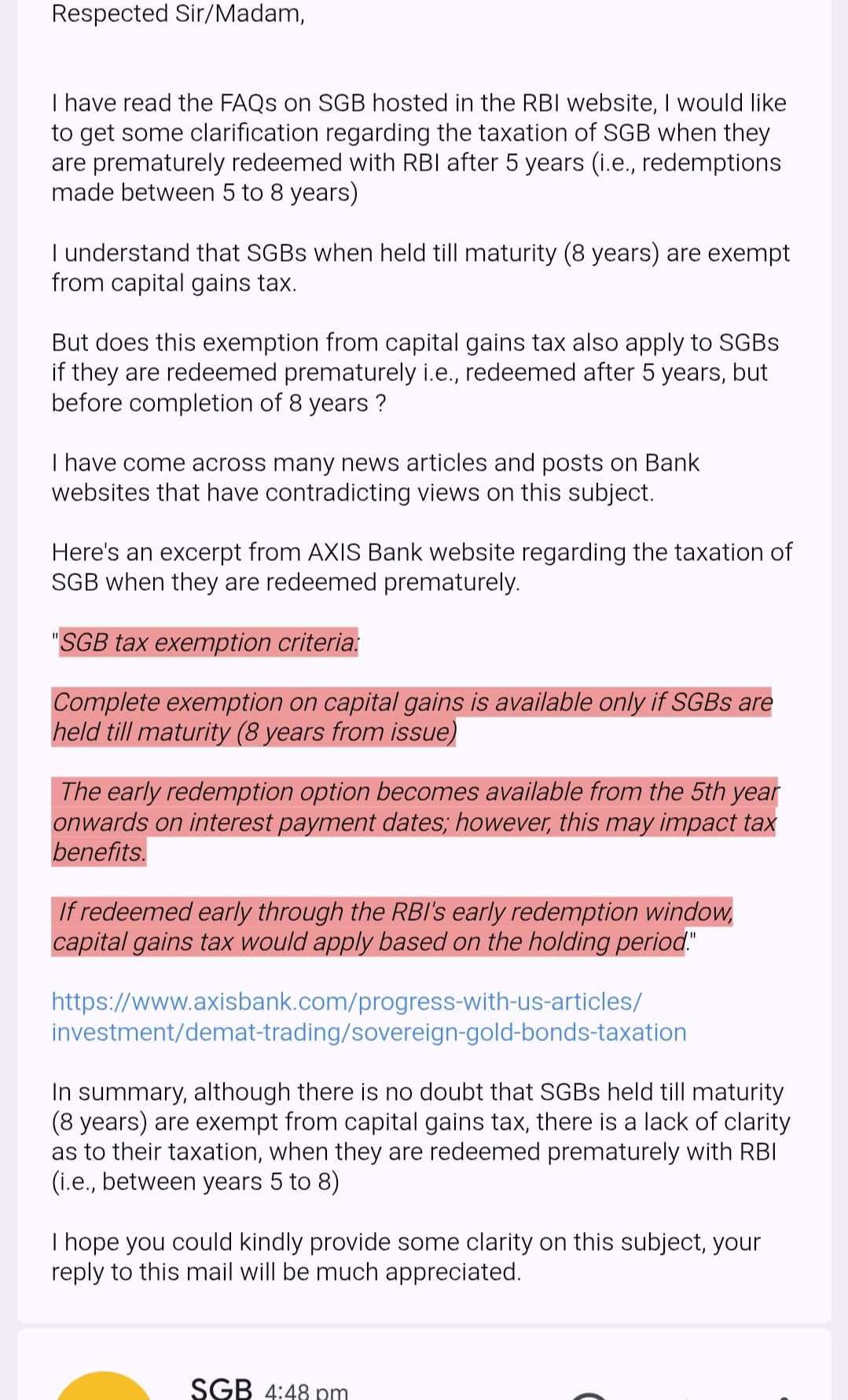

I have been reading many articles/posts/threads/FAQs and what not on SGB’s taxation. More precisely, when the capital gains tax arising on redemption are exempt.

Unfortunately, after going through most of the contents on this topic, I couldn’t arrive at a conclusion as to when the SGBs are fully exempt from capital gains tax. This is because, there are contradicting views on this, some 1 2 say that redemption with RBI at any time after 5 years (premature redemption) are tax-exempt, while others 3 4 say that the capital gains are exempt only if they are held till maturity and redeemed at the end of 8 years.

So, there seems to be no unanimous opinion/interpretation as to when the capital gains arising on SGB redemption are exempt from tax.

I was hoping that the RBI’s FAQs on this topic would provide some indisputable clarity, however, the answers seem ambiguous, as it simply states “The capital gains tax arising on redemption of SGB to an individual has been exempted”.

IMO, the only clue here is the word redemption (which i interpret as redemption on maturity i.e., 8 years). I say this because, the FAQs seem to differentiate redemption from premature redemption.

They could have mentioned that the capital gains tax arising on both redemption and premature redemption are exempt from tax, but they didn’t. IMO the word redemption can’t be considered to also include premature redemption in its definition.

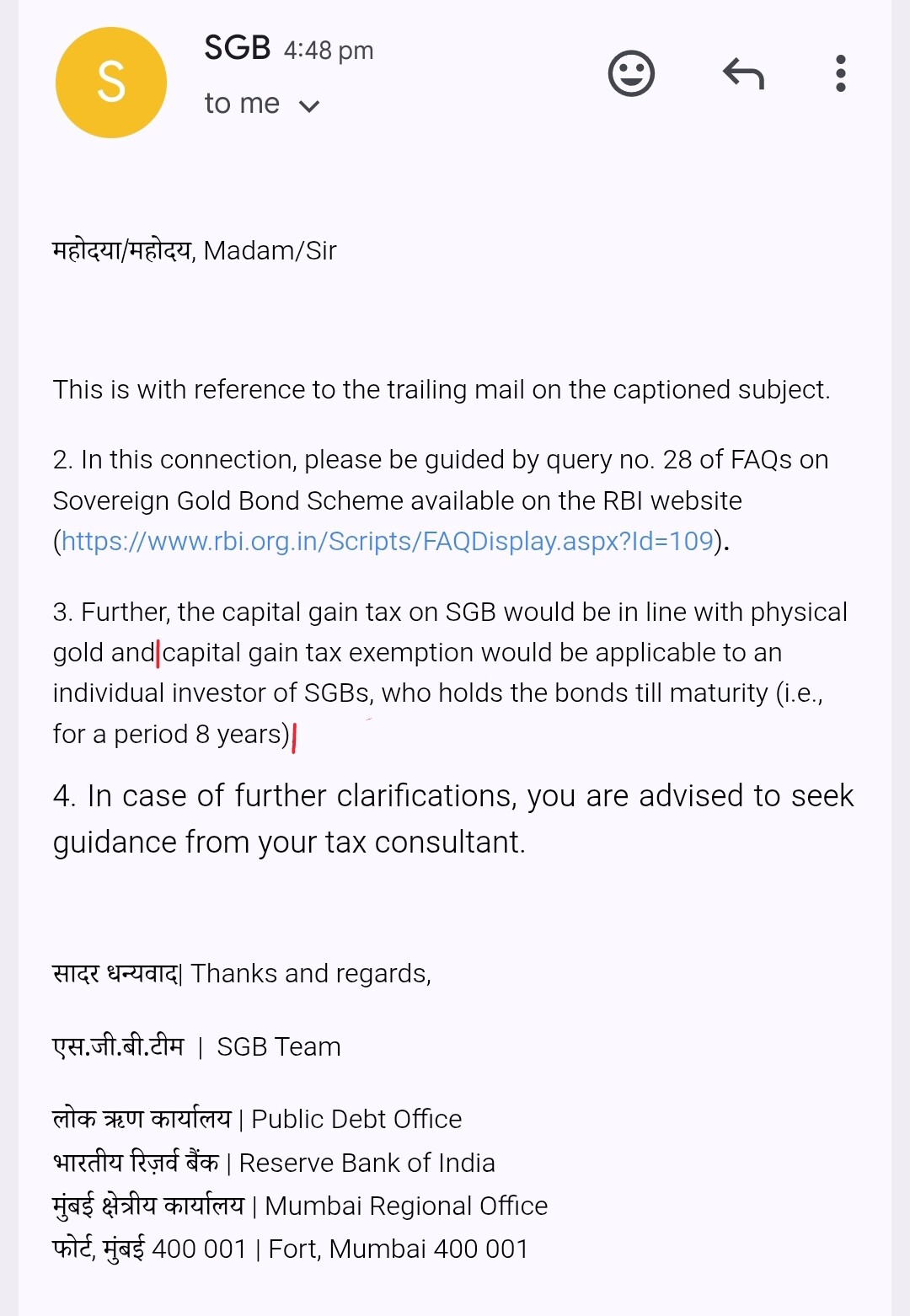

Anyway, since I was not getting any clarity on this topic, i decided to reach out to RBI’s SGB team which was created to address any queries on SGB, and this is the reply i received.

As per their reply, it is certain that the capital gains tax on redemption of SGBs are exempt only if they are held till maturity (8 years), and therefore any premature redemption with RBI between years 5 to 8 would be subject to tax.

PS:

With regards to OP’s query of buying from the secondary market and holding for a term less than 8 years, although redemption with RBI on maturity is exempt from tax, i believe such exemption is available only if the person is the primary investor of the SGB, who subscribed to the SGB directly with RBI. I say this because, the holding period too matters, anyone buying from the secondary market will have a holding period of less than 8 years, the word held till maturity normally implies that you bought it on day one and held till the due date, and only the primary investor gets the certificate of holding.

IMO, anyone purchasing from the secondary market will not be eligible for any tax exemption, because the holding period is not something that gets transferred from one person to another, we need to consider the holding period of each individual to determine if the bonds were held for 8 years. Buying from secondary market and redeeming on the due date/maturity date doesn’t mean the bonds were held till maturity, they are simply redeemed on maturity, not held till maturity.

We can’t just hold a bond for any period less than 8 years and still enjoy tax exemption simply by being the last person holding the bonds and redeeming it with the RBI.

Unfortunately, since i didn’t read OP’s query while drafting the mail to RBI, I couldn’t include this query in my mail.