We have witnessed many investors using NAV just like a stock value to choose a fund for their portfolio.

New mutual fund investors are often puzzled by NAV (Net Asset Value).

“Is it like a stock price?”, they ask.

“It is very similar in essence but totally different!”

NAV is the price of 1 unit of a mutual fund. It is like the price of one unit of a stock.

But with a difference. What is NAV?

Mutual funds collect money from investors (you) and invest them in various assets like stocks, bonds etc.

These funds are divided into units and when you invest in a mutual fund, you are given units of mutual fund which is based on the NAV of the Fund.

The NAV is one unit that represents per unit price of the assets held by a mutual fund on a particular day. It measures how much each unit of a mutual fund is worth.

But the more important question today is, should Mutual Fund Investors use NAV to make investment decisions?

Absolutely NOT.

Newer mutual funds have lower NAV than older ones and many new investors mistakenly pick a newer mutual fund because the NAV is lower.

When a mutual fund launches a New Fund Offer (NFO) where generally the price of a mutual fund unit is Rs.10, many investors believe that it is low NAV of the mutual fund unit. However, it is the price of a unit which the investor has to pay for a mutual fund unit, and not a Net Asset Value of the Fund. A lot of investors believe that a fund with a lower net asset value is cheaper and hence, a better investment. In truth, it is not an indicator of mutual fund performance. A lower value alone does not make a fund a better investment or vice versa, it should not be the only determining factor to choose a mutual fund.

What you should look at the time of investment is long term performance records of the scheme

So how does one actually use a NAV?

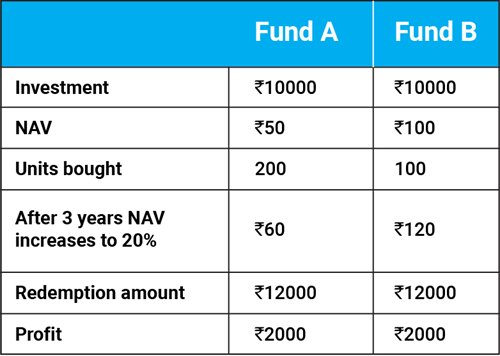

If you invested ₹10000 in the beginning in Mutual Fund A & B, and the NAV is Rs. 50 for Mutual Fund A and Rs. 100 for Mutual Fund B. You would have gotten 200 units and 100 units for Scheme A & B respectively.

Assuming over the years, both the funds NAV increases by 20%, because the fund manager has picked up good investments and improved the value of the fund’s portfolio.

After the increase in NAV, if you sold these units, you would have gotten back ₹60 X 200 = ₹12000 back for Scheme A and ₹120 X 100 = Rs. 12,000 from Scheme B.

So you would have made a profit of ₹2000.

This table shows how choosing schemes on the basis of low NAV does not mean higher profits.

The above table is for illustration purpose only.

How is NAV calculated?

Mutual Funds are bought & sold at their NAV.

NAV = Assets – Liabilities/No of units

NAV of Mutual Fund Scheme changes every business day, since market value of securities it holds changes every trading day.

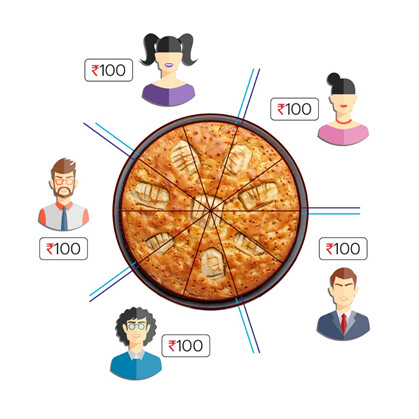

Suppose on your birthday, four of your friends pitch in Rs. 250 to get a birthday cake costing Rs. 1000.

Suppose the cake was cut into 10 slices, five people (four friends & you) would get 2 slice each which means the unit cost of one slice of cake is Rs. 100.

The above graph is for illustrative purpose only.

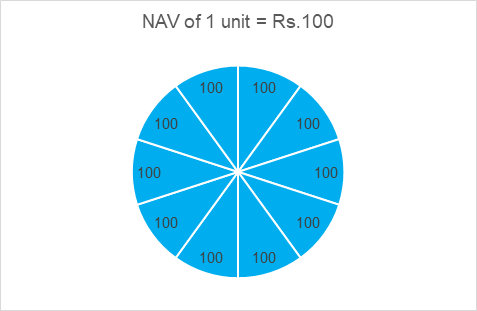

If the same example were to apply to a mutual fund. Let’s assume there’s a mutual fund scheme with total assets under management (AUM) of Rs. 1000 with 10 outstanding units. The fund had 5 investors who held 2 units each. Thus the NAV of the fund comes at Rs.100 (Rs. 1000 AUM divided by 10 outstanding units).

Thus, while purchasing a mutual fund scheme, the NAV of the fund is of little significance. High NAV should not be a deterrent and low NAV should not be a preference while buying a mutual fund.

The increase or the decrease of NAV just indicates how the fund has performed over the period.

Therefore, a higher NAV means the mutual funds’ investments have prospered really well or the mutual fund has been around for a long period. The investors should focus on the mutual fund’s performance and the returns generated while investing in a mutual fund scheme.

Instead of the NAV, it is a wiser move to base your investment decision on your risk profile, the time horizon of your investment and your financial goals.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.