Summary by ChatGPT

The thread argues that the recent ₹25,500 crore borrowing by the Shapoorji Pallonji (SP) Group is less about raising money and more about betting that regulatory pressure will eventually force a resolution over its stake in Tata Sons.

Key points

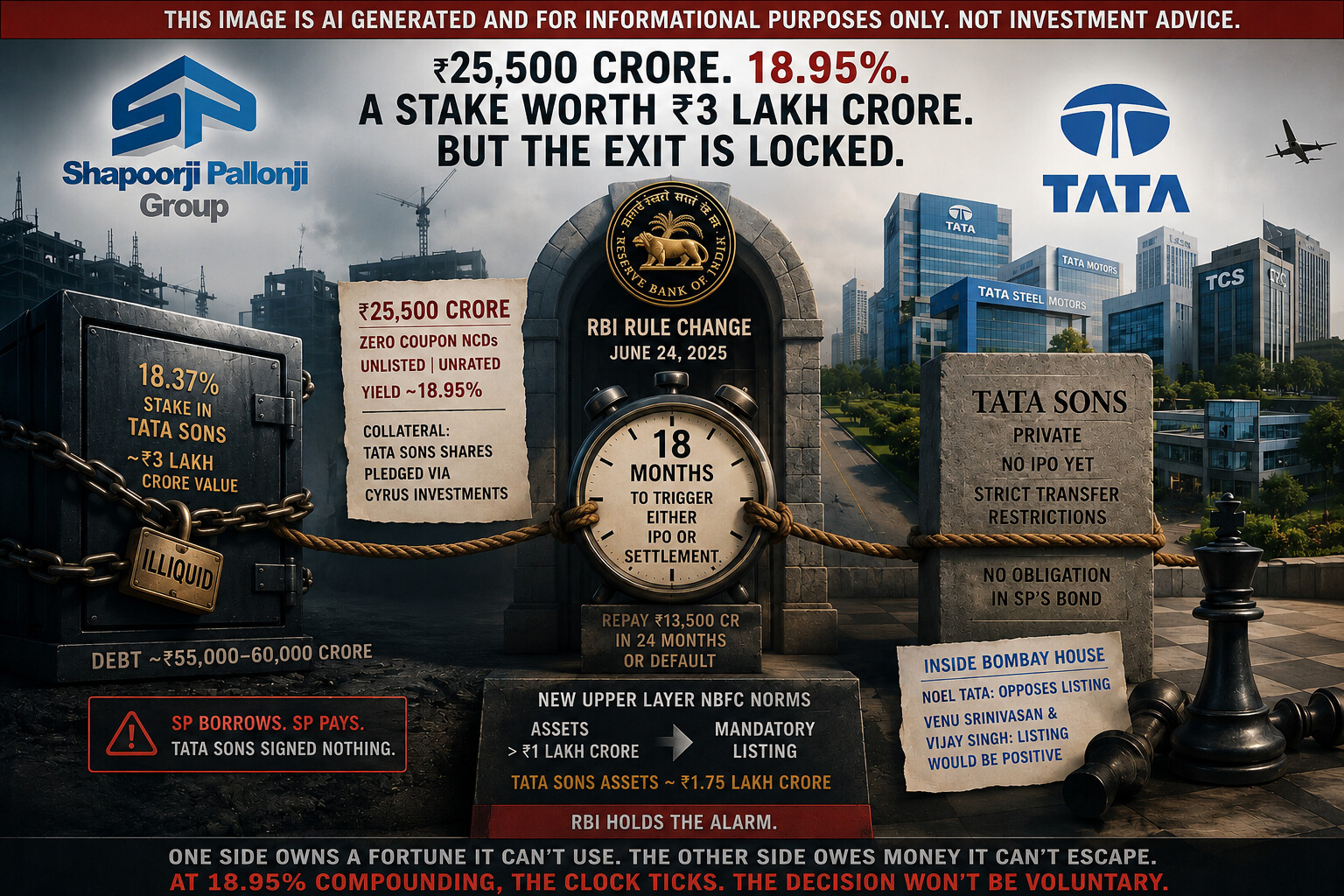

- SP Group owns 18.37% of Tata Sons, a stake worth roughly ₹3 lakh crore, but it is illiquid because Tata Sons is a private company with restrictions on share transfers.

- Despite the stake being worth several times its debt, SP cannot easily monetize it, so it has repeatedly borrowed against it.

- SP has now issued ₹25,500 crore of zero-coupon, unlisted, unrated NCDs with an implied yield of about 18.95%, using its Tata Sons stake as collateral.

- Such a high yield suggests lenders perceive significant risk.

- The bond requires that within 18 months either:

- Tata Sons announces an IPO, or

- SP reaches a settlement with Tata regarding its ownership.

- SP must also repay ₹13,500 crore within 24 months, failing which it would default.

- Importantly, Tata Sons is not a party to these bond terms. If no IPO or settlement occurs, **SP—not Tata—faces the consequences.

Why lenders are willing to finance it

The thread argues the confidence comes from recent RBI regulatory changes, not from any commitment by Tata.

According to the author:

- The RBI’s revised framework for Upper Layer NBFCs now primarily classifies companies with assets exceeding ₹1 lakh crore as Upper Layer NBFCs.

- Since Tata Sons reportedly has standalone assets of around ₹1.75 lakh crore, the author believes it is difficult for Tata Sons to avoid being classified.

- Upper Layer NBFCs are generally required to list on a stock exchange.

- Tata Sons had previously tried to avoid listing by surrendering its NBFC licence, but that application remains pending.

- A later RBI clarification reportedly broadened the interpretation of “public funds”, which the author believes further weakens Tata Sons’ ability to avoid listing.

Possible outcomes

The thread suggests two realistic scenarios:

- Tata Sons lists, allowing SP eventually to monetize its stake.

- Tata buys out or restructures SP’s stake, keeping Tata Sons private while giving SP liquidity.

The author considers the second outcome more likely.

Internal dynamics

The thread also claims there are differing views within the Tata Group:

- Noel Tata is said to favour remaining private.

- Venu Srinivasan and Vijay Singh have reportedly expressed that a listing could be beneficial.

Bottom line

The thread’s central thesis is:

SP Group isn’t forcing Tata Sons into an IPO. Instead, it is borrowing at a very high cost because it believes recent RBI regulations have increased the probability that Tata Sons will eventually have to either list or negotiate a settlement.

A note of caution

Some parts of the thread are analysis and inference rather than established fact. In particular:

- Whether the RBI’s revised framework will ultimately compel Tata Sons to list remains uncertain.

- Tata Sons’ pending application to surrender its NBFC licence could materially affect the outcome.

- The specific bond covenants and their interpretation have not been publicly confirmed in full.

So, while the financing itself is real, the thread’s conclusion—that RBI pressure makes an IPO or settlement increasingly likely—is a well-argued hypothesis, not a confirmed outcome.