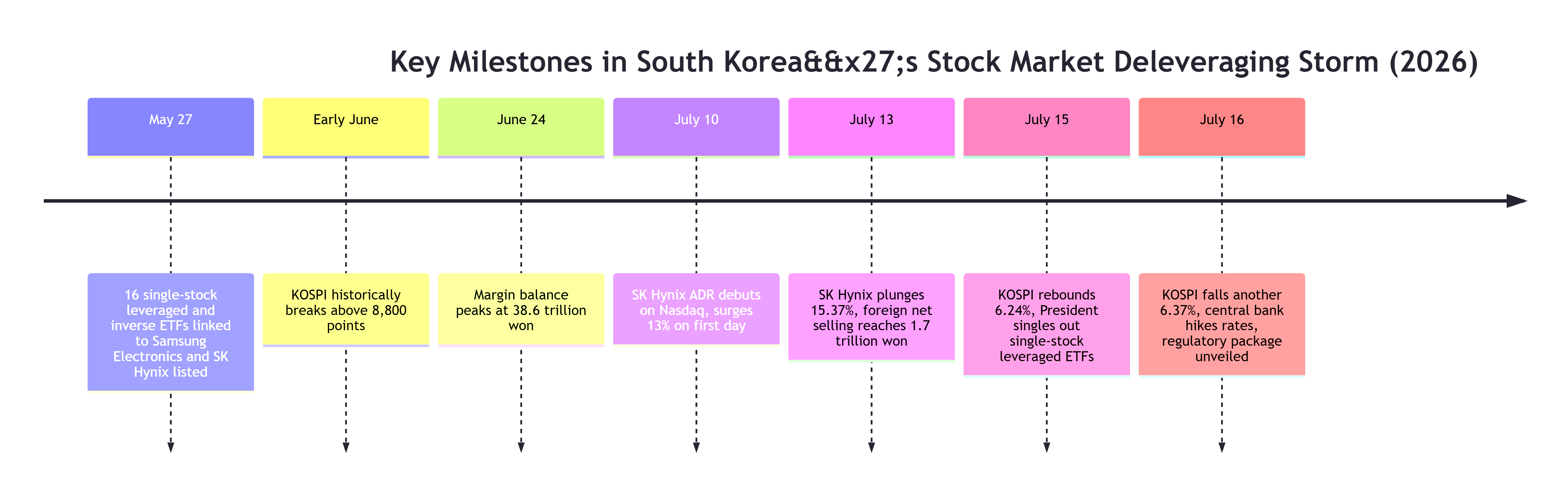

On July 16, South Korea’s benchmark KOSPI index plummeted 463.81 points, or 6.37%, to close at 6,820.60, once again breaching the psychological 7,000-point level. Just one day earlier, the index had surged 6.24%. This pattern of violent swings—plunge, rally, plunge again—has become the new normal for South Korean equities, as a full-scale deleveraging storm triggered by leveraged trading unfolds. Earlier the same day, the Bank of Korea raised its benchmark interest rate by 25 basis points to 2.75%, its first rate hike since early 2023, further tightening market liquidity expectations.

According to South Korea’s Financial Supervisory Service, as of July 13, over 1.2 million leveraged accounts across the market had triggered margin calls—equivalent to one in every 30 adults facing the risk of a blow-up. Among them, approximately 320,000 to 360,000 accounts were forcibly liquidated in full by securities firms, wiping out their principal entirely. Some retail investors ended up insolvent, not only losing all their capital but also owing additional debt to their brokers.

The epicenter of this storm is Samsung Electronics (005930.KS) and SK Hynix (000660.KS), along with their associated leveraged ETFs. As global demand for AI computing power exploded, shares of these two memory chip giants soared, propelling the KOSPI to a historic breakthrough above 8,800 points in early June, with market capitalization doubling in five months. However, when concerns about the AI frenzy emerged, the collapse happened virtually overnight.

The key milestones of this storm are as follows:

The “Negative Compounding Effect” of Leveraged Products

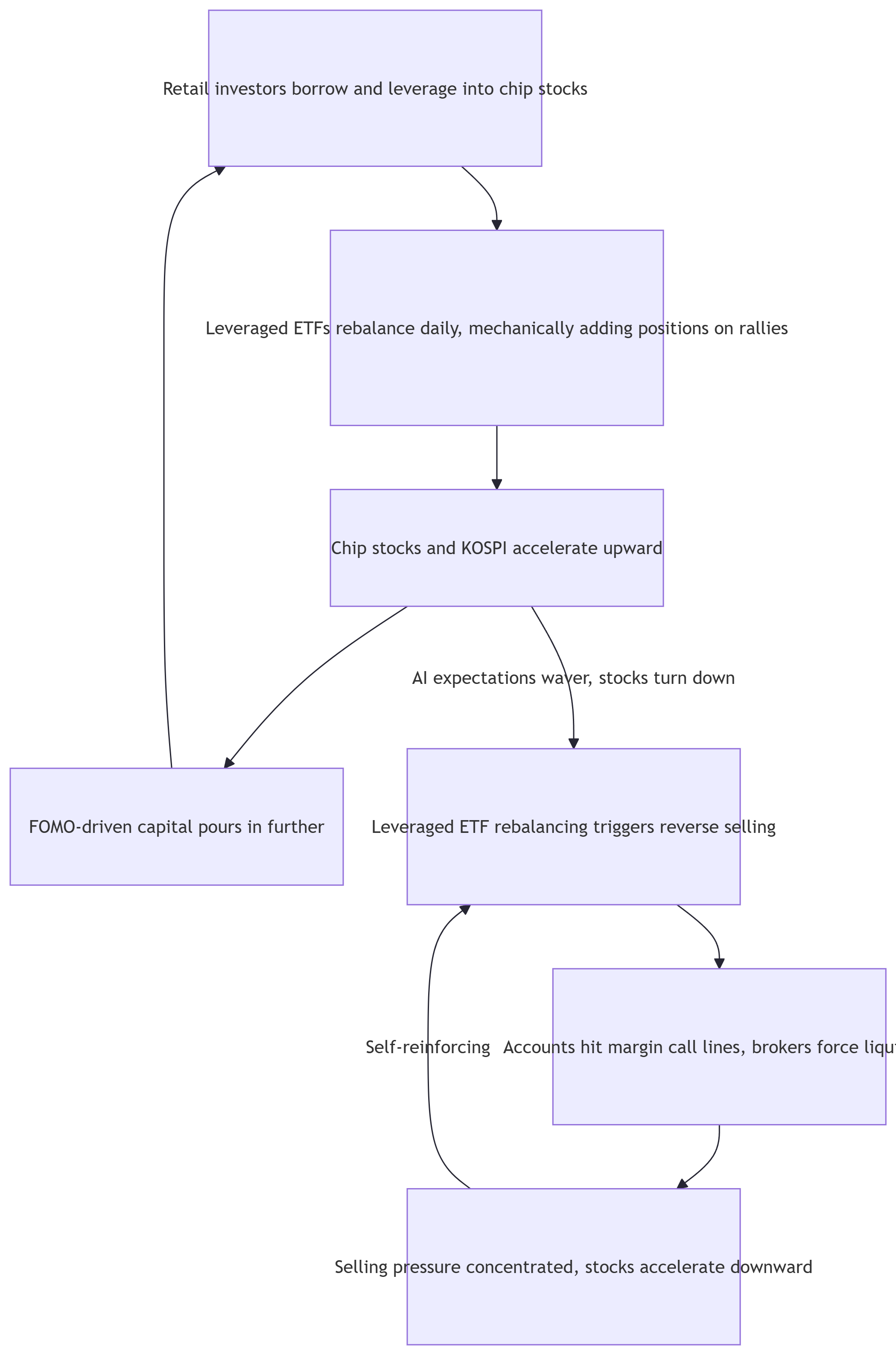

Single-stock leveraged ETFs, which South Korean retail investors have been frantically chasing, became the amplifier of this crisis. These products require daily rebalancing—buying more when prices rise, selling when they fall—which fuels rallies on the way up and accelerates selling pressure on the way down. Even more dangerous is the “negative compounding effect” that occurs during declines: even if the underlying stock eventually returns to its original price, long-term holders of leveraged products can suffer far greater losses as their principal is steadily eroded.

Take SK Hynix as an example. The stock has fallen nearly 40% from its June all-time high, while its 2x leveraged ETF has plunged more than 66% at its worst. On July 13, SK Hynix tumbled 15.37% in a single day, its largest one-day drop in 18 years. According to Bloomberg data, foreign investors net sold 1.7 trillion won (approximately $11 million) worth of KOSPI stocks that day, with the bulk concentrated in SK Hynix. Notably, SK Hynix’s American Depositary Receipts (ADR) had just debuted on the Nasdaq on July 10, surging 13% on its first day, with some capital subsequently shifting from the Seoul market to the ADR, further intensifying selling pressure on the local stock.

According to statistics compiled by the Maeil Business Newspaper, forced liquidation volumes in South Korea’s stock market began surging in May, with forced liquidation amounts from May through July 14 reaching 2.3 trillion won (approximately $1.55 billion). Data from the Korea Financial Investment Association shows margin balances rose from 27.4 trillion won in early January to a peak of 38.6 trillion won on June 24, before rapidly retreating to 34.7 trillion won. From the market peak on June 22 through July 14, the total value of South Korean investors’ margin accounts shrank by 20.9 trillion won (approximately $14.1 billion).

The Shattered Wealth Dreams of Retail Investors

In this leveraged frenzy, the wealth dreams of countless ordinary people have turned to dust. A 39-year-old office worker poured approximately 80 million won (approximately $54,009) of housing funds into semiconductor stocks and leveraged ETFs and is now sitting on paper losses of roughly 18 million won (approximately $12,152). He admitted that if stock prices fail to recover, his wedding plans may have to be postponed. Lee Seung-ho, a 24-year-old university student, used margin loans to amplify his principal to 300 million won (approximately $202,533), only to see nearly all of it evaporate in the market pullback.

Some extreme cases have even turned criminal. On July 13, a man in his 20s in Busan stabbed a financial YouTuber in his 40s multiple times before fleeing. Police stated the suspect was a subscriber to the YouTuber’s channel who, after following the influencer’s stock investment analysis, bet his entire life savings and ended up trapped with catastrophic losses.

Regulators Step In, Deleveraging Underway

Faced with mounting leverage risks, South Korean regulators moved swiftly. On July 16, South Korea’s Financial Services Commission announced a package of measures targeting single-stock leveraged ETFs: suspending new single-stock leveraged product listings until the market stabilizes; raising the minimum margin from 10 million won to 30 million won (approximately $6,751 to approximately $20,253), with only cash accepted as collateral; and increasing the minimum trading unit for single-stock leveraged products from 1 share to 20 shares to curb small-scale high-frequency trading.

| Regulatory Measure |

Before Adjustment |

After Adjustment |

| New single-stock leveraged product listings |

Permitted |

Suspended until market stabilizes |

| Product marketing and promotion |

Permitted |

Suspended |

| Minimum margin |

10 million won |

30 million won, cash only |

| Minimum trading unit |

1 share |

20 shares |

| Mandatory investor education |

2 hours |

Add 1 hour advanced course |

| Market maker tracking error cap |

3% |

2% |

| Such rapid intervention is unusual. According to the Korea JoongAng Daily, since the 16 single-stock leveraged and inverse ETFs linked to Samsung Electronics and SK Hynix were listed on May 27, South Korea’s stock market has triggered the “sidecar” circuit breaker mechanism 19 times, with 37 triggers year-to-date, as violent swings have earned the market the nickname “Roller Kospi.” The head of the FSC’s capital markets bureau admitted at a press conference that introducing restrictive measures just over a month after product launch was “extremely unusual.” |

|

|

A day earlier, South Korean President Lee Jae-myung directly named Samsung Electronics and SK Hynix single-stock leveraged ETFs, demanding relevant authorities “swiftly and properly formulate supplementary measures.” Financial Supervisory Service Governor Lee Chan-jin immediately responded that he would take responsibility.

However, regulators also emphasized that this round of volatility is not entirely caused by single-stock leveraged ETFs—during the same period, global memory chip stocks such as Micron Technology and Kioxia experienced even greater volatility than SK Hynix, reflecting a global market reassessment of the semiconductor cycle outlook.

Wu Qicong, assistant researcher at the Chongyang Institute for Financial Studies at Renmin University of China, analyzed that South Korea’s leveraged trading frenzy is driven by three factors: wealth anxiety stemming from high housing prices and education and retirement costs, government policies encouraging capital to flow back into the stock market, and the lowered barriers to leverage through mobile trading and margin lending. “Essentially, this is the result of anxiety, policy, and financial innovation layered on top of each other.”

Goldman Sachs noted in a related report that this sell-off was significantly amplified, primarily because newly listed single-stock leveraged ETFs experienced rapid deleveraging, triggering a self-reinforcing chain of liquidations that became clearly disconnected from fundamental drivers. Goldman identified KOSPI 6,800 as the most important technical support line, and the July 16 close happened to hold right at this threshold.

Deleveraging Is Far From Over

Despite the regulatory measures now in place, market participants widely believe the deleveraging process is far from complete. Li Yujie, head of Hong Kong and overseas strategy research at Huatai Securities Research Institute, noted that as of July 15, the absolute size of leveraged ETFs had fallen by more than 50% from the June 25 peak, but the decline in size mainly came from net asset value shrinkage due to falling underlying stock prices, while product shares merely slowed their expansion rather than experiencing a significant pullback. “This means the structural foundation for leverage may still exist, and we have yet to see clear signs of contraction.”

Wu Qicong also believes that “the current deleveraging still carries a strong passive character. Only when margin balances decline while forced liquidation amounts continue to fall and investor account funds stabilize can we say the market is truly approaching the completion of risk clearance.”

Notably, the violent volatility in South Korea’s stock market has already produced spillover effects. On July 16, Japan’s Nikkei 225 index plunged 1,915.97 points, or 2.79%, to close at 66,835.54. In the US market the previous day, Micron Technology (MU) tumbled 8.02%, SanDisk fell 8.12%, and the SOX semiconductor index dropped more than 2%.

In contrast, TSMC (2330.TW) reported on the same day that its second-quarter net profit surged 77% year-on-year to NT$706.56 billion (approximately $21.9 billion), a record quarterly high, with its stock price bucking the trend to rise 1.23%. However, this positive news failed to stabilize South Korean semiconductor stocks, indicating that the sell-off in South Korea’s market stems more from a self-reinforcing cycle of internal leverage liquidation rather than fundamental deterioration.

Why Are South Korean Retail Investors So Reckless?

The roots of this crisis lie in the resonance between deep-seated “gambler’s mentality” in South Korean society and national policy direction. Over the past few decades, South Koreans’ wealth has been highly concentrated in real estate, with property accounting for 75% of household wealth and stocks just 9%. The South Korean government sought to channel funds from the real estate market into equities to fuel strategic industries such as semiconductors and AI, launching a series of reforms including the “Corporate Value-Up Program.”

When global AI infrastructure construction exploded and Samsung Electronics and SK Hynix became core suppliers of HBM high-bandwidth memory, the South Korean government saw an opportunity to draw capital back and expand the domestic stock market. Locally domiciled leveraged ETFs, previously strictly prohibited, were given the green light, going from proposal to product launch in less than four months.

However, capital did not flow evenly across the entire capital market but became highly concentrated in a handful of AI winners. With Samsung and SK Hynix together accounting for more than half of KOSPI’s total market capitalization, the entire South Korean stock market mutated into a massive “one-sided betting machine.” An extremely violent positive feedback loop took shape: AI chip stocks rise, the index hits new highs, retail investors fear missing out, they pile in with leverage, and chip stocks go to the moon. But in reverse, when stock prices fall, the stampede triggered by leverage liquidation is equally ferocious.

Wu Qicong cautioned that if South Korea’s stock market continues to deleverage, risks could spill over to SK Hynix ADRs and transmit to Micron Technology, SanDisk, and other global memory chip companies. However, South Korean market volatility alone is insufficient to trigger a global stock market crash. “Only when South Korea’s deleveraging coincides with a global downgrade in AI investment expectations, concentrated fund redemptions, and exchange rate pressures can localized risks potentially escalate into systemic risks.”