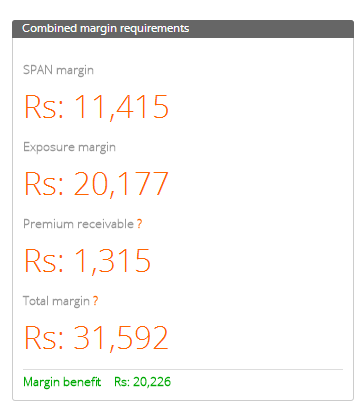

If I buy an at-the-money NIFTY put and a NIFTY future, both with same expiry, say April 2014. I then sell an ATM NIFTY call with same expiry. I am essentially trying to setup a put-call-futures parity condition, which is a hedged position. I expect the margin for such a position to be significantly low, but when I calculate the same using the SPAN calculator, I get the total margin for this position as Rs. 31,592 (for strike price of 6700). Can anyone please explain why the margin should be so high even for such a hedged position?

You do get a margin benefit, if you are looking at the SPAN calculator, it is around 20k lesser than what would be required if the positions weren't hedging each other.

Coming back to the question, on if the risk or maximum loss is fixed for this strategy, then why charge even so much?

The reason is because there is an execution risk to this strategy. There is no way to control if you will enter or exit all the 3 positions at once. What if you exit the long Nifty future first, and then market suddenly bounces? The short calls can then create an unlimited loss. The margins charged by the exchange would be after factoring in all such risks.

Thanks for such a quick response Nithin. It does make sense. But I need three further clarifications for the same situation:

a.) In a hypothetical scenario, where all 3 positions can be entered and exited at once, would the SPAN margin be zero?

b.) Is this hypothetical scenario achievable using algorithmic trading?

c.) SPAN is calculated over a time frame, which is definitely longer than a few seconds. But NIFTY options (and futures) being so liquid, it is inconceivable that the 3 positions cannot be closed within seconds of each other (please correct me if I am wrong in assuming this). Then how is SPAN margin calculated in this case? Maximum loss over the next few minutes shouldn’t be so high as per my understanding. Kindly clarify.

Thanks for your time.

-Shivam

a. Yep, if there was a way that the spread was trading in itself, SPAN would be significantly lower. Do check out calendar spreads on NSE, these spreads trade directly on the exchange, you could buy or sell them directly instead of placing 2 orders to buy and sell different month expires of the same future contract. The margin benefit you get is almost 85%.

b. The only way to achieve this scenario is if the strategy itself starts trading, like the way calendar spreads on futures trade on NSE.

c. SPAN margins usually are calculated based on worst possible one day move and not over the next few minutes. It is not about being able to exit 3 positions at one time, but what if a trader decides not to? There has to be enough margin blocked so that even if the trader doesn’t exit all positions at once or any such incident happens, there is enough margin to cover for the risk of the remaining positions.

I tried looking up the NSE website, but where exactly is the calendar spread option? Also, if I want to implement the same in ZT, can I do it? I am assuming I can still manually do it, but ZT will consider it 2 separate orders rather than a single order as NSE would interpret it.

Hi Nithin,

Is it possible to say block only the required(maximum loss possible) margin when all the positions are hedged and as soon the user tries to come out of one position, to block more margin(Actual margin required for Non-hedged position)? In this way, we can account for the execution risk. Yes, then there is a rick of not having enough margin when user tries to exit, but we can have negative margin or we can Reject the order saying not enough margin available…

I guess currently it is not there. But, can you please consider including this kind of a feature. It would be such a boon for hedged traders especially with less captial…

my uncle in US says the margin is not needed but only net premium required for bull call spread or bear put spread. but here in india ZT asks margin like futures for sell leg . it is basic risk management not letting the user to place long leg unless margin or short leg is covered. it is nicely done in even comission free robinhood trading. wish ZT has similar thing!

Hi Nitin, i have a question on margin requirement , i am selling a yesbank 20pe of feb2020 and the lot size , and if it reaches 20 i would like to those shares at 20.

So in worst case i need 20*8800 as margin but the margin calculator shows 283000 instead of 176000

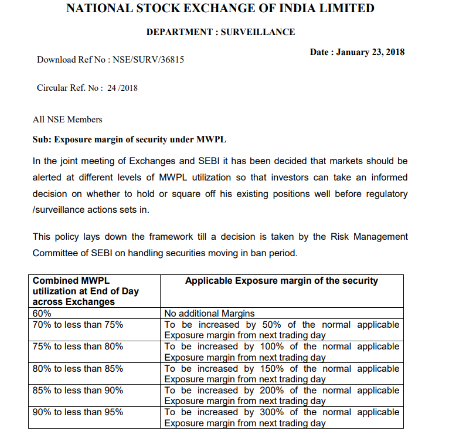

For options shorting exposure margin is calculated as below

"The exposure margins for stock options

For option contracts on individual Securities:

The higher of 5% or 1.5 standard deviation of the notional value of gross open position in futures on individual securities and gross short open positions in options on individual securities in a particular underlying. The standard deviation of daily logarithmic returns of prices in the underlying stock in the cash market in the last six months is computed on a rolling and monthly basis at the end of each month.

For this purpose notional value means:

For an options contract - the value of an equivalent number of shares as conveyed by the options contract, in the underlying market, based on the last available closing price."

Copied from NSE site, can check that for more info on margins.

That way of calculation gives exposure margin of around 30%, also as yesbank is under ban due to MWPL limit it has higher exposure based on the slab of MWPL it fall.

Can download full circular from here, no 31685.

Hence it is charging much higher exposure, you logic is theoretically correct but practically exposure is charged based on various other factors, hope this answered your query.

If I sell 1 lot of Nifty May future and buy 1 lot of 9600 CE (May) then Margin required is 50,605 approx.

I have only 60K in account, how can I enter this strategy?

Should I buy 9600 CE first and then sell future or other way round.

Because if i sell Future first then the margin for selling is 1.37 lakh so I would not be able to execute it.

Can anyone tell me is my assumption correct

Pls look at how tastytrade in usa executes the option strategy and how they mitigate the risk try to impliment that it would be great-they have some great system

I have question,

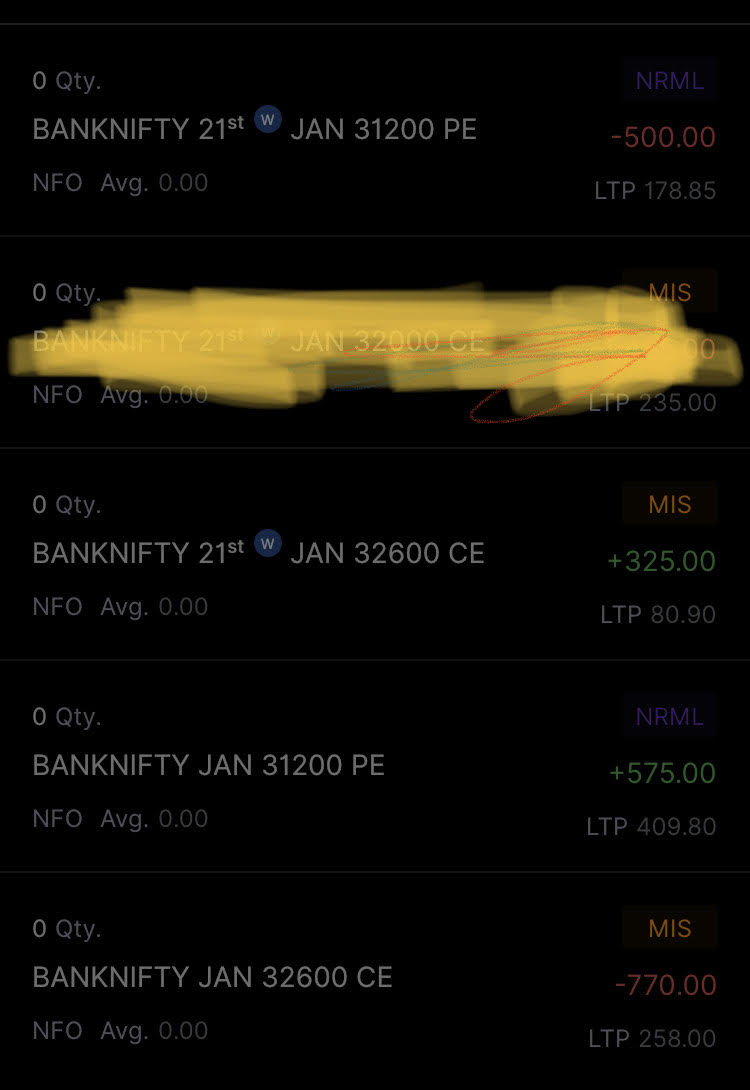

today i have done Double Diagonal Calendar in mis order, after trying to carry forward position and failed due to margin requirement, pls answers this ?? my position completely hedge, pls find attached screen shot of my position tdy i have done, ignore yellow color position that was intraday,

Margins Calculator showing 39k , But at a time i have in may account 72k,

Hi Zerodha ,

Please advise, if we have a hedged Futures position which was achieved with margin benefits via Zerodha Basket by having first Long Put ITM Option and then Long Futures , all same month expiry and same lot… below are the 3 questions

if we exit the Long Futures first either due to GTT stop loss / stop profit or manual exit and then 2nd Long Put ITM Option manually-- no margin shoot up or penalty right?

But if we exit the Long Put ITM Option first manually (once Futures targets are achieved) and then immediately exit the Long Futures – for few minutes there will be margin requirement increase because Long Futures will become naked and for those few minutes will there be any margin penalty?

This 2nd scenario is incase the Long Put ITM Option is very less liquid then we need to exit Long Put ITM Option first because if it do not exits then we have to maintain the Long Put ITM Option and Long Futures till expiry so that both gets netted off with each other, ofcourse with some loss or may be some profit but at least no physical settlement obligation?

Incase any hedged Long Futures position with Long Put ITM Options – how the net off happens it happens automatically and next day after the current month expiry the trading account will have the final some loss or may be some profit?

Right, the margin wouldn’t shoot up in this scenario and there won’t be any penalty.

Yes, there can be margin penalty. Exchange now takes 4 snapshots of positions during market hours to check whether adequate margins are maintained. If it is taken at this moment, there will be peak margin penalty.

So it is best to always first exit high margin (Futures, Short Option) position first and then long option position.

Right, the obligation will be netted-off and you won’t have to give or take delivery of underlying shares.

The net-off happens automatically, you don’t have to do anything. Any profit/loss you make will be available for trading from the next day.

Q1) In case of hedged position Long Futures NRML hedged with Long Put ITM Option NRML – if the price starts falling freakingly so I will be covered by Long Put ITM Option NRML however to recover some more loss if I Short Call OTM Option in intraday not NRML - will it nullify the Long Put ITM NRML and my Long Futures NRML will become naked and hence the margin requirement will shoot up or this will not happen, or intraday will not affect the NRML hedged pair?

Q2) Long Put ITM Option NRML was 1st row and Long Futures NRML was 2nd row at the time of entry - so which leg order was executed first during position making, doesnt have any issues on the physical net off, this still holds good?

Q3) Whenever in any hedged position like Long Futures NRML with Long Put ITM Option NRML if we buy another Long Put ITM Option NRML and then sell the old one, will not sell till the new option is bought, will this also shoot up any margin for few minutes or no affect will happen as for few minute Long Futures will be over hedged only, please advise?

Q4) Whenever in any hedged position like Long Futures NRML with Long Put ITM Option NRML if we buy another Long Put ITM Option NRML and then sell the old one, the funds released by selling the old Long Put ITM Option NRML comes immediately and 100% to trading account and they can be used for same day any Intrday F&O / CNC and for Overnight F&O / CNC, please advise?

Q5) M2M of Futures gets in the trading account funds same T day by end of day , meaning before next day market opening and then they can be used for Intraday and overnigth for both F&O and CNC?

Q6) If we dont use Basket Order and first buy the Long Put ITM Option NRML same stock same month expiry via GTT or manual and then second we buy Long Futures NRML same stock same month expiry via GTT or manual will the margin reduction benefit be available for Long Futures NRML or its available only in Basket Order?

Q7) What happens in case of CTM 3 strikes rule - Call Options will become CTM which are 3 strikes below the expiry day stock price and 3 strikes above the final stock price as CTM Put Options. will they be also liable for physical settlement Long (call or put) and Short (call or put) positions both?

. it is basic risk management not letting the user to place long leg unless margin or short leg is covered. it is nicely done in even comission free robinhood trading. wish ZT has similar thing!

. it is basic risk management not letting the user to place long leg unless margin or short leg is covered. it is nicely done in even comission free robinhood trading. wish ZT has similar thing!

keeping my fingers crossed it happens asap

keeping my fingers crossed it happens asap