Shivam,

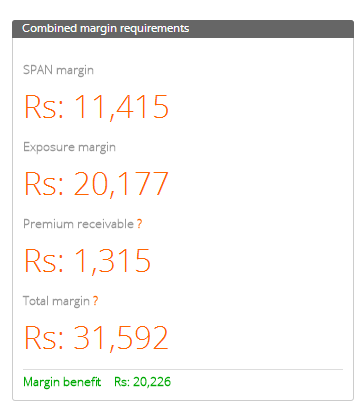

You do get a margin benefit, if you are looking at the SPAN calculator, it is around 20k lesser than what would be required if the positions weren't hedging each other.

Coming back to the question, on if the risk or maximum loss is fixed for this strategy, then why charge even so much?

The reason is because there is an execution risk to this strategy. There is no way to control if you will enter or exit all the 3 positions at once. What if you exit the long Nifty future first, and then market suddenly bounces? The short calls can then create an unlimited loss. The margins charged by the exchange would be after factoring in all such risks.

Hope this clarifies,