SPIVA (S&P Indices Versus Active funds) just published an update on the performance of actively managed mutual funds against their benchmarks for the first half of 2022.

S&P Indian published the SPIVA (S&P Indices Versus Active funds) scorecard which compares the performance of actively managed Indian mutual funds with their respective benchmark indices. This report studies the performance of three categories of actively managed equity funds and two categories of actively managed bond funds over the 1, 3, 5, and 10-year periods.

2022 hasn’t been a great year for equity markets. Russia’s invasion of Ukraine, rising inflation and central banks around the world hiking interest rates to tame the inflation. All these factors have had an adverse impact on stock markets.

As of 12th October 2022, the benchmark index Nifty 50 is down around 2.5% since the start of the year and about 8% from highs made in November 2021 and down by over 15% from highs and around 10.5% for the half-year ending 30th June 2022.

Look at how the active mutual funds performed

-

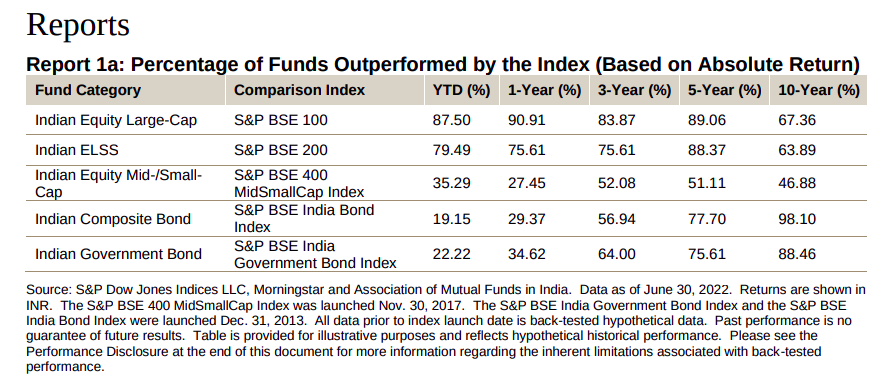

In the first six months of 2022, 87.5% of Large-Cap active funds underperformed the benchmark S&P BSE 100 Index.

-

79.5% of the ELSS funds underperformed the benchmark index, the S&P BSE 200 Index. The long-term performance remained a bit better but still, over 60% of ELSS funds underperformed over a 10-year period.

-

The MidCap and SmallCap funds seem to have fared well in the short as well as long run, although they come with much more volatility. In the first six months of 2022 with 35.4% of the actively managed funds underperformed the benchmark, S&P BSE 400 MidSmallCap Index

-

Coming to Composite Bond Funds, in the first half of 2022, the underperformance was the lowest among all other categories. However, as we look at the longer period, the underperformance keeps increasing. Over a 10-year period, almost 100% of the funds underperformed their benchmark, the S&P BSE India Bond Index.

-

We can see a similar theme play out in Government Bond Funds. In the first half of 2022, around 22% of actively managed government bond funds underperformed the S&P BSE India Government Bond Index benchmark index. Over the long run, however, fewer and fewer funds managed to beat the benchmark. Over a 10-year period, around 90% of funds underperformed.

Taking a look across different years;

First-half 2022;

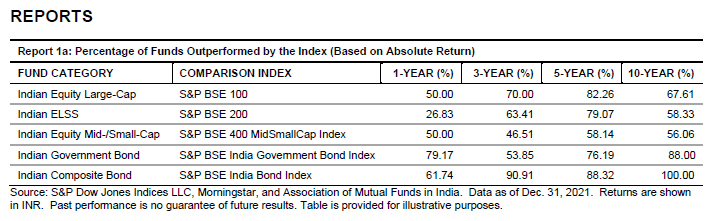

As of December 31, 2021

You can read the full report here:

You can read this post to check 2021 report:

Takeaways

-

It makes no sense to invest in active large-cap funds anymore. Investors are better off investing in either Nifty 50/Sensex or Nifty 100 index funds or ETFs. The reason is that after the scheme recategorization, SEBI clearly defined the universe for large, mid and smallcap funds. Largecap funds can only invest in the top 100 stocks by market cap, so it’s very very hard to generate any meaningful alpha.

-

Some active funds will always beat the benchmarks, and you’ll only know this in hindsight. It’s very, very hard to identify funds/managers that will beat the benchmark in advance. This is the key reason why index funds and ETFs make a lot of sense.

-

As the Indian markets continue to grow and deepen, these numbers will only get worse and worse.

-

It’s absolutely clear from the longer-term numbers that index funds or ETFs should be the core part of a portfolio. You can always use active funds or smart beta funds as a satellite part of your portfolio to generate some outperformance. Check this out for an intro to core and satellite approach to asset allocation .