Anyone aware what’s going to happen with SEFL NCD? There has been no payment of interest or update from the company

SEFL has stopped paying interest and principal because of cashflow mismatch due to covid induced lock downs. Most banks and financial institutions have declared it as an NPA account.

Banks and company are trying to reach a debt restructuring. Once in a while Catalyst, who is trustee of NCD publishes updates on it website. You can check there for more details.

https://www.catalysttrustee.com/press-release/updates-for-debenture-holders/

1 Like

seems like it is going DHFL way. Looks like a long drawn bankruptcy process, going ahead.

1 Like

just curious to know, did you buy secured or un secured NCD ?

cause they will sell their assets to pay your principal amount if you have secured NCD. right ?

if they go bankrupt.

I have secured NCD

Theoretically yes. But practically secured NCD will have right on Assets but so would be lot of secured lenders (like bank, financial institutions and so on) so you may or may not get full principal back in case of bankruptcy. However, chances of getting more money back are much higher for secured NCD holders, than unsecured ones.

Yes, you are right.

@Akash_Shah , In DHFL case didn’t they repay 100% for secured NCD ? (i’m not sure tho).

And what happened to DHFL unsecured NCDs ? How much % did they repay

No they didn’t. All secured lenders, including secured NCD holders only got around 42% payout.

However, a special exception was made for small retail NCD holders (holding less than 2 lakh) - only for such people 100% capital was paid back. Not for everyone.

Unsecured NCD holders were paid just 5%, regardless of amount of holding.

This is so bad ![]() , lots of innocent investors lost almost everything!

, lots of innocent investors lost almost everything!

1 Like

How to check secured or unsecured NCD

1 Like

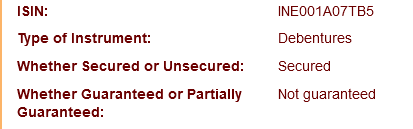

Check in NSDL India bond info

@Akash_Shah , I’ve a small question for you. In NSDL india bond info (see the below pic).

This is a NCD by HDFC.

It is a secured debenture.

What about “whether guaranteed or partially guaranteed ?”.

Why is it secured and at the same time not guaranteed ?

like if the company goes broke, won’t they sell their assets and return our initial investment ?

Or big lenders like banks/financial institutions will get re paid first and retail investors NCD is not guaranteed ?

What does it actually mean ?

Thanks in advance.

1 Like

Even mine is secured but not guaranteed.

1 Like

I observed one thing in common that only government listed securities are guaranteed.

All other things like corporate NCD etc are not guaranteed even though they are secured.

It will be clear if someone like @Akash_Shah or @ShubhS9 or @Bhuvan differentiate between guranteed and secured.

Like why is not guaranteed when it is secured ? Companies assets will be liquidated if the company goes broker. Or is it like big banks/financial institutions will be eligible for these credits first than retail ?

As far as I know, only government securities are guaranteed and secured. While corporate NCD are secured but not guaranteed.

Btw, @Akash_Shah other than NSDL website, do you recommend any other sources for this purpose ?

Thanks in advance!

2 Likes

@TradeXMaster Term “Secured” and “Guaranteed” are unrelated in term of NCD.

Term Secured refers to - your NCD payables are secured against company assets. So if company fails to pay you back, secured lender has right to make claim to company asset and recover money. This does not necessarily mean you will get all money back, because:

a) There will be multiple secured lenders (like bank, FI and others) and company asset might not be sufficient to support all claims.

b) Company promoters might have done fraud and shown inflated asset. Actually company may not even have sufficient asset as claimed (which was DHFL case)

This only means you have a higher claim than unsecured lender.

In such scenario all secured lenders will be treated equally and whatever pie is available will be equally distributed (this happened in DHFL case).

Term Guaranteed refers to - scenario where company does not have assets but still want to provide some protection to lenders (for getting better rates).

In this scenario, some other company or individual can guarantee the sum. Some examples:

- Some years back Reliance Jio raised lot of money through unsecured NCD (Since it had practically no asset) Guaranteed by Reliance Ltd.

- Zee promoters has raised lot of money for their infra business through Zee promoter acting as guarantor.

- Air India raises lot of money guaranteed by govt of India. As such no body in their right mind would lend money to AIr india (heavy losses, hardly any assets left etc.). So AIr India issues NCD guaranteed by govt India. That way people would still be willing to lend and borrowing does not show up in GoI books.

Typically this is used by comapnies with multiple subsidiaries or promoters with varied interest to get better rates on companies which are starting up or have no assets.

Again this does not mean that you will get all your money back. This only means that if Reliance Jio defaults, you can make a claim with Reliance Ltd. (which most likely will pay up)

In reliance ADAG case some of the lending was personally guaranteed by promoters, but when it came to pay up, even promoters declared bankruptcy.

Hope the difference is clear now.

Technically yes, and that’s why they earn lowest return (since risk is minimal).

But in global terms, even sovereign govt defaulting is not unheard of. Couple of years back Venezuela govt defaulted on its foreign borrowing and lenders were paid only a fraction of what it was owed.

Hope this helps.

1 Like

Hi Akash,

Like DHFL repayment 100% repayment given to small investor less than 2 lakhs did any such provision has been made to SREI small NCD holder if not please suggest how can such small investor form a group and approach company to consider. Please share contact details of administrator. Thanks.

SREI resolution plan is not yet finalized. This detail will be known once resolution plan is finalized and approved by Committee of Creditors

I don’t think anything can be done here. Everyone have to abide by CoC. In DHFL too, FD holders and Unsecured holders went to court against CoC decision. Nothing happened.

I don’t really have administrators details. You can reach out to your bond trustee to get this.

These types of NCDs are always risky. They can be even riskier than equity, since in these instruments you can end up loosing your entire amount. If somebody wants to earn interest then government bonds for long term or high rated corporate bonds should be the right choice.

1 Like

Ummm … DHFL was AAA rated almost till last day ![]()

In hindsight everything looks like a simple decision.