Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Sri Lanka’s redemption: Is debt restructuring enough?

- India’s fertilizer puzzle: Imports, subsidies, and struggles

Sri Lanka’s redemption: Is debt restructuring enough?

Moody’s, the credit rating agency, has hinted that it might upgrade Sri Lanka’s credit rating. That’s a pretty big deal. Not too long ago, Sri Lanka was in such a deep economic crisis that it couldn’t even pay its debts.

Here’s what’s happening: Sri Lanka is trying to clean up its financial mess by swapping old, troublesome debt with new, more manageable debt. Moody’s has given this new debt a better provisional rating. It’s still far from ideal—it’s deep in the “junk” category—but it’s definitely a step up from where it was.

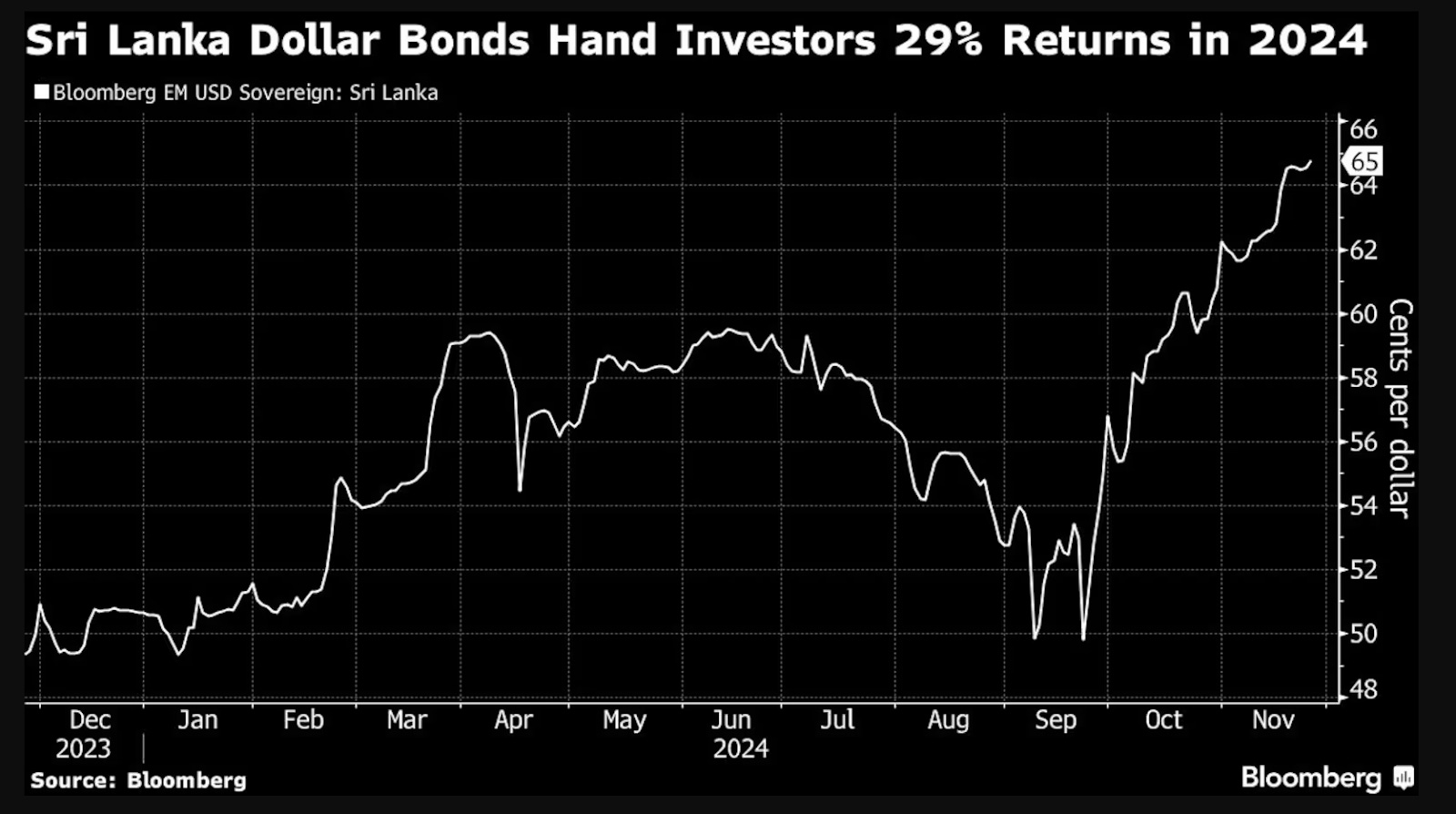

This renewed optimism around debt restructuring is also why Sri Lanka’s bonds have become an unexpected success this year, delivering an impressive 29% return. For investors, this is a sign that the market believes Sri Lanka might be on the path to stabilizing its economy, at least for now.

Source: Bloomberg

But how did Sri Lanka end up in this situation in the first place?

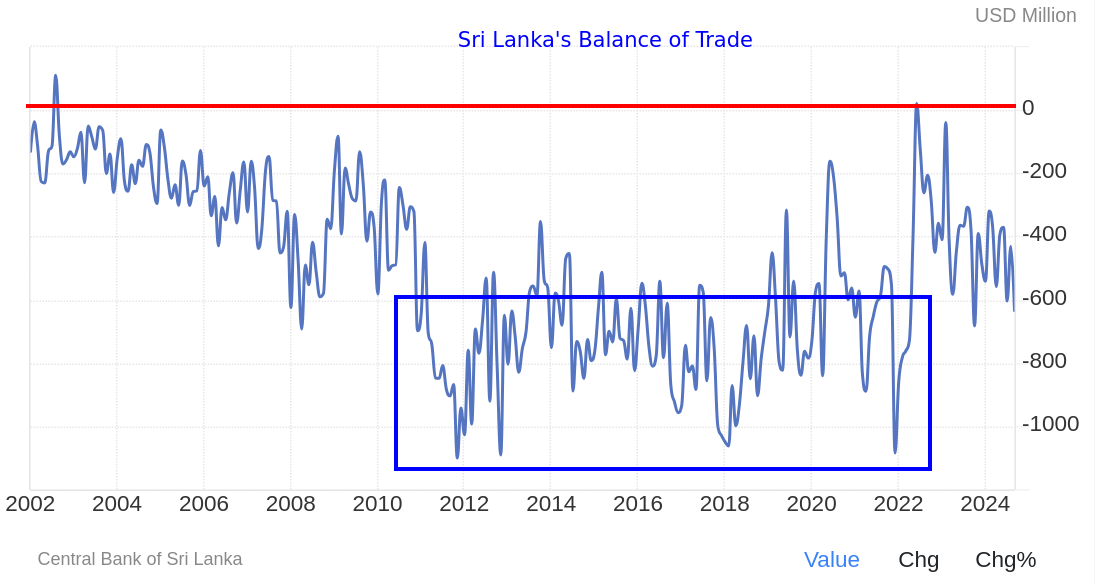

Let’s go back to 2009 when the country’s 25-year civil war came to an end. The cost of the war was massive—around $200 billion, which was five times the size of Sri Lanka’s economy at the time. After the war, the country needed to rebuild, but it got overly ambitious. Instead of focusing on increasing exports or boosting trade, Sri Lanka decided to try producing everything it needed domestically.

That might sound like a patriotic idea, but here’s the problem: it didn’t work. Exports remained flat at around $10 billion a year, while imports ballooned to $18 billion. Every year, the country was importing about $8 billion more than it exported. And how did it cover that gap? By borrowing—heavily. The debt kept piling up year after year, pushing the country deeper into trouble.

Source: Trading Economics

By 2019, Sri Lanka’s trade balance was deeply in the red, with borrowed money filling the gap. This constant borrowing drained the country’s foreign exchange reserves, making it more and more vulnerable. On top of that, paying interest on these loans was becoming a huge burden, further straining the already low reserves.

Things weren’t much better at home. In 2019, the government slashed taxes, which might sound good in theory, but it ended up costing the country over $1.4 billion in lost revenue every year. At the same time, they continued spending on freebies and welfare programs. The math didn’t add up—earning less while spending more meant the economy was living on borrowed time. All it took was one major crisis to tip it over the edge.

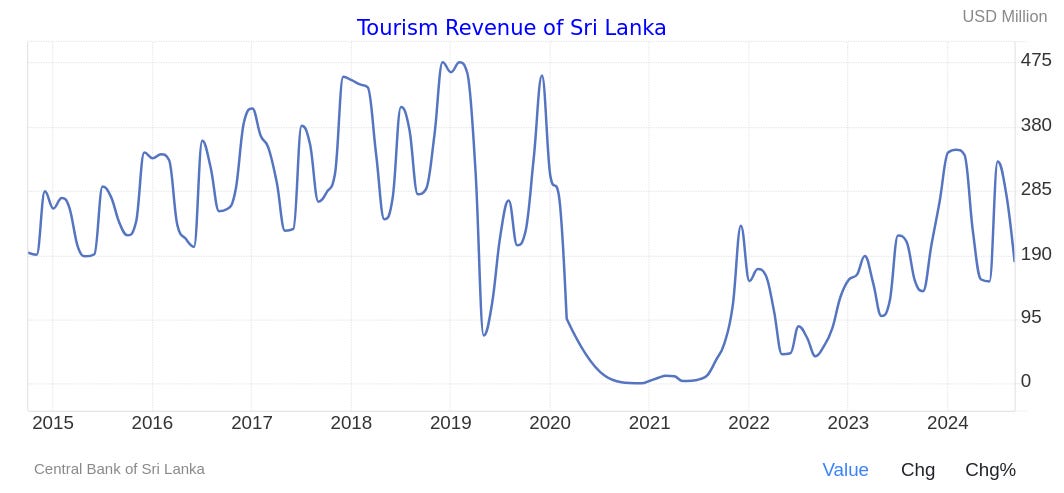

That crisis came in the form of the COVID-19 pandemic. What was already a fragile situation turned into a complete disaster. Tourism, one of Sri Lanka’s biggest sources of foreign currency, came to a standstill. With reserves already running low, the government panicked.

To save foreign currency, they started cutting down on imports of what they considered “non-essential” items. Chemical fertilizers ended up on that list. The government claimed it was transitioning the entire country to “organic farming,” but in reality, it was just trying to cut costs.

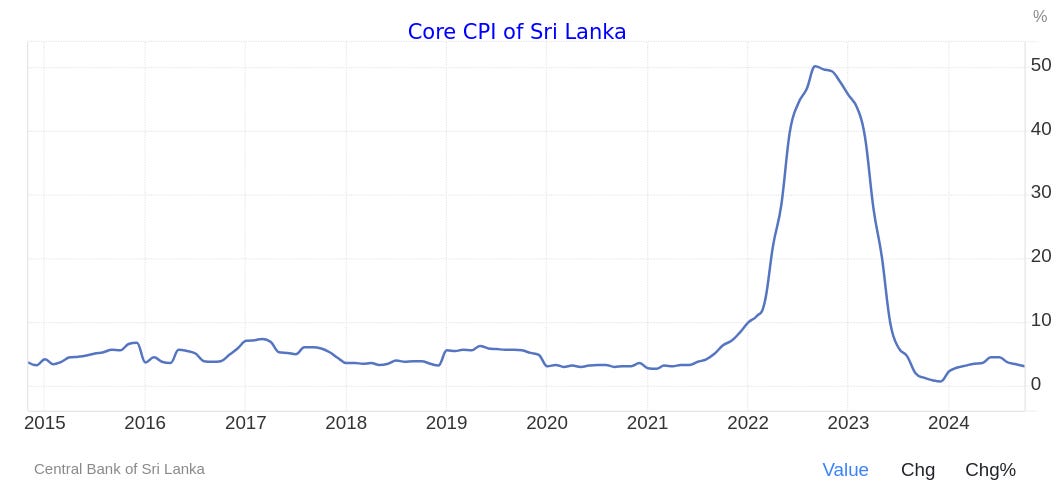

The decision backfired in a big way. Without chemical fertilizers, farmers couldn’t grow enough crops. This led to widespread crop failures, and a country that once exported food suddenly didn’t have enough to feed its own people. Food prices skyrocketed, and inflation soared to a staggering 50%. The government had no choice but to reverse the policy.

In short, Sri Lanka was running out of money, grappling with deficits, and losing foreign reserves. In its attempt to save dollars by banning fertilizer imports, it unintentionally triggered food shortages and out-of-control inflation, making a bad situation even worse.

Everything fell apart. The government had no choice but to focus on buying essentials like food and fuel instead of paying back its lenders. In May 2022, Sri Lanka officially defaulted on its debt for the first time in its history.

At that point, the country hit rock bottom and had to take action. The first step? Renegotiate its massive pile of debt. The problem was that this debt wasn’t simple—it came in many forms. Some of it was internal, owed within the country. But most of it was external, including bilateral loans from countries like China, India, and Japan, as well as International Sovereign Bonds (ISBs), which are loans from global investors.

Sri Lanka began talks on all fronts. With bilateral loans, there was some progress—China and India agreed to restructure their loans, giving the country more time to pay them back. The ISBs, however, were a tougher challenge. An initial proposal was rejected by creditors, dragging negotiations out. But finally, just two days before the presidential election, Sri Lanka managed to reach a deal.

So, what’s the deal? Sri Lanka is swapping its old bonds for three new types: Macro-Linked Bonds (MLBs), Governance-Linked Bonds (GLBs), and Step-Up and Past-Due Interest Bonds. Here’s how they work:

- MLBs : These bonds are tied to how well Sri Lanka’s economy performs. If the economy does well, bondholders get higher payouts. If it underperforms, they get less.

- GLBs : These are linked to governance reforms, like meeting IMF targets for tax revenue. If Sri Lanka follows through on these reforms, the government pays less. It’s like a reward for doing the right thing.

- Step-Up Bonds : These start with lower interest payments that gradually increase over time, giving the country some breathing room to recover in the short term.

These new terms are much more manageable for Sri Lanka, especially given the fragile state of its economy.

Meanwhile, because the government paused debt payments during the negotiations, its foreign exchange reserves have started to recover. Tourism is also picking up—not back to pre-COVID levels yet, but enough to provide some much-needed support to GDP and forex reserves. Inflation has also stabilized, though prices are still painfully high for most people.

Source: Trading Economics

Source: Trading Economics

It’s not perfect, but it’s a step in the right direction for a country working to rebuild.

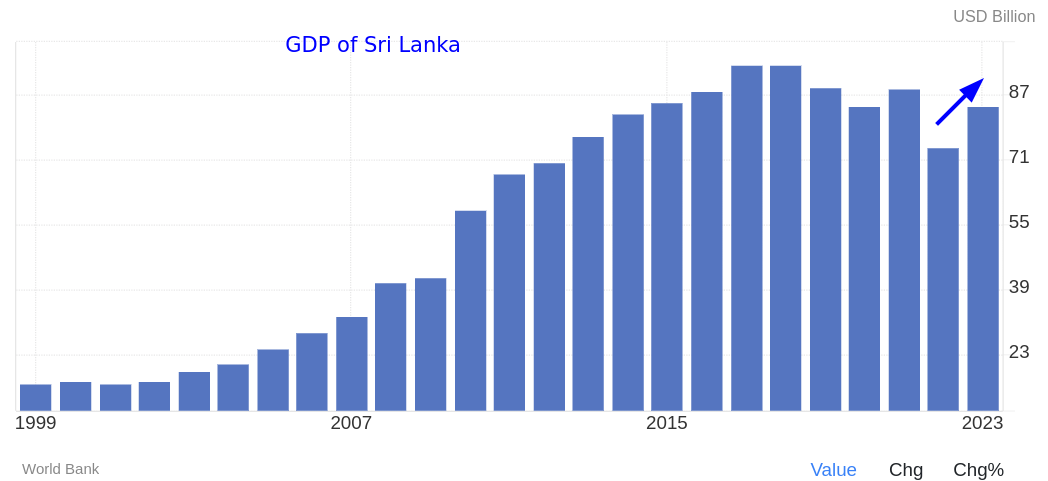

All of this suggests that the worst may be over for Sri Lanka’s economy. GDP growth is starting to stabilize, which is a welcome change after the chaos of the past few years.

Source: Trading Economics

But here’s the reality: this is just the first step. There’s no guarantee that the country will truly turn the corner. Sri Lanka is still on life support. The debt restructuring and the temporary relief from lenders can only do so much. The bigger issues—the structural problems we talked about earlier—are still unresolved.

Sri Lanka is still a net importer, running massive trade deficits. The government’s fiscal deficits are just as worrying, and there’s no clear plan to tackle either of these. On top of that, we’re already seeing signs of backtracking on critical reforms. For example, while the country had opened up its power sector to private players, the new National People’s Power (NPP) government has reversed those reforms.

Without addressing these deep-rooted issues, Sri Lanka risks falling back into another crisis. The debt restructuring gives the country some breathing room, but time alone won’t fix things if the fundamental problems remain. Structural changes are the only way forward.

There’s still a long road ahead, and it’s going to take a lot of tough decisions and hard work to get there.

India’s fertilizer puzzle: Imports, subsidies, and struggles

The Indian government has announced steps to increase the domestic supply of Di-ammonium Phosphate (DAP) fertilizers. This comes in response to disruptions caused by the Red Sea crisis, which impacted fertilizer imports. Since India imports 60% of its DAP, these measures aim to ensure a steady supply and reduce dependence on foreign sources.

Why is DAP so important? And how does it fit into the bigger picture of Indian agriculture?

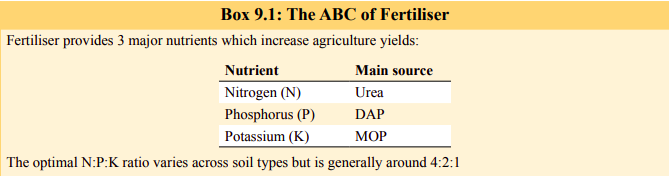

Fertilizers add three key nutrients to the soil: (a) Nitrogen, (b) Phosphorus, and (c) Potassium. Each type of fertilizer serves a specific purpose. For example, DAP contains 18% nitrogen and 46% phosphorus, making it essential for the early growth of crops. It’s especially important for Rabi crops like wheat and mustard.

Source: India Budget

India relies heavily on imports for fertilizers, particularly those based on potassium and phosphorus. This dependence makes us vulnerable to global price changes and supply disruptions. That’s why the government is working to boost local production. But achieving self-sufficiency isn’t easy. India has long struggled to meet its own fertilizer needs.

This challenge traces back to the Green Revolution of the 1960s. Back then, the government introduced high-yield seeds, better irrigation, and fertilizers to increase farm productivity. Since fertilizers were expensive, subsidies and price controls made them more affordable for farmers. These efforts were a game-changer, helping India achieve food security after years of shortages. But over time, this system also led to inefficiencies.

India spends nearly ₹2 lakh crore every year on fertilizer subsidies, making it one of the highest spends in the world. These subsidies help keep fertilizers affordable for farmers, but they also create some big problems.

Here’s how it works: subsidies go directly to fertilizer manufacturers, covering the costs they incur beyond a fixed price. This system creates an odd incentive — the less efficient you are, the more subsidy you get. As a result, it discourages companies from modernizing or becoming more efficient.

Farmers, on the other hand, overuse cheap urea because it’s so affordable. This throws off the ideal balance of nutrients in the soil, known as the N:P:K ratio of 4:2:1, and harms soil health. Over time, this has led to significant nitrogen pollution in the soil.

The low price of fertilizers has also created unintended consequences. Fertilizers meant for Indian farms are often diverted for industrial use or smuggled to neighboring countries like Nepal and Bangladesh. For instance, a 50kg bag of urea costs farmers just ₹266, while its production cost is around ₹3,000. The government pays the difference through subsidies. This price gap not only strains public finances but also fuels black-market activities, where urea is sold at much higher prices.

Meanwhile, businesses in the fertilizer sector are heavily impacted by government controls. Everything from production and distribution to the chemical composition of fertilizers is regulated, leaving no room for product innovation or differentiation. On top of that, the huge subsidy burden often leads to delayed payments by the government, creating financial uncertainty for companies in the industry.

All this makes it tough for private companies to succeed in the fertilizer industry. A big chunk of India’s fertilizer production is handled by public sector units (PSUs), while the rest of the demand is met through imports.

India is actually the largest fertilizer importer in the world. While domestic production covers most of our urea needs, we rely heavily on imports for other fertilizers. About 60% of our Di-ammonium Phosphate (DAP) comes from countries like Morocco, Jordan, and Saudi Arabia. When it comes to Muriate of Potash (MOP), we import 100% of our supply, mostly from Canada, Belarus, and Russia.

This heavy dependence on imports makes us vulnerable to global supply disruptions. For example, in 2021, China stopped exporting fertilizers, which caused major supply issues in India. The Ukraine war has also disrupted our potash imports entirely. While the government has started joint ventures and is trying to boost domestic production, progress has been slow.

These issues create supply shortages, unstable availability, and higher prices for farmers, adding to the industry’s challenges.

India is in a tough spot. The agriculture sector is full of economic imbalances that create constant problems. At the same time, it’s stuck in old patterns, and as we saw with the farm laws, making changes isn’t easy. For now, all we have are temporary fixes to keep things going.

Tidbits

- Honda Motorcycle and Scooter India have entered the EV market with two new models: the Activa E and the QC1. The company is aiming to sell 100,000 units in the first year. With a strong network of 6,000 outlets, Honda plans to grab 50% of key EV markets. Bookings for these models will open in January 2025.

- In the US, the economy grew by 2.8% in Q3, thanks to strong consumer spending and stable corporate profits. While inflation and high borrowing costs remain challenges, steady business investments show confidence in long-term growth.

- India’s imports from China revealed an $18 billion mismatch in trade data, caused by valuation differences and reporting inconsistencies. This highlights the need for stricter trade monitoring and better regulatory practices.

- On November 17, a record 505,000 people flew domestically in India, boosted by the peak wedding season. Airlines are reporting an 80-90% surge in demand this November, with charter flights and international honeymoon destinations especially popular.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.