Economics Times covered how stockbrokers use partially funded FDRs as collateral. RBI sees this as a systemic risk.

The Reserve Bank of India (RBI) has initiated a probe into funding

arrangements between some private banks and stock brokers after a lender’s refusal to

pay up as part of a share-settlement process led to a legal dispute. The central bank has

written to the Securities and Exchange Board of India (Sebi) seeking details about socalled Fixed Deposit Receipts (FDRs), an instrument that brokers place with the

clearing members of trades as collateral.

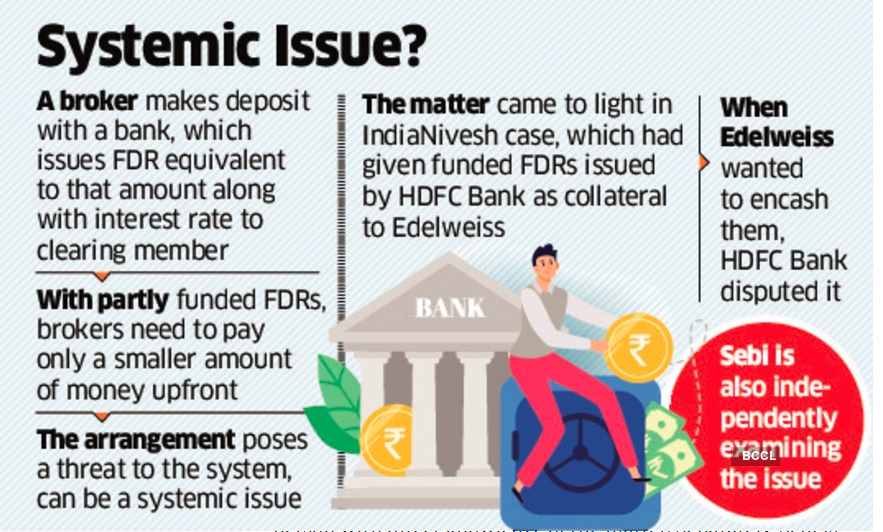

Typically, a broker makes a deposit with a bank, which issues an FDR equivalent to

that amount, along with the interest rate, to the clearing member. But regulators have

stumbled upon instances where brokers have borrowed money from banks for creating

FDRs and given that as collateral. By doing this, brokers need to pay only a smaller

amount of money upfront.

@nithin, why would a stockbroker need to get banks to fund their Fixed Deposits and then use these as collateral? Can’t a stockbroker just use a bank guarantee instead?

Today brokers allow customers intraday leverage over and above the margin in the account, and to buy stocks for delivery with more money than what is in the account - also called Margin funding (we don’t offer it at Zerodha). If customers are buying for more, the capital is being provided by the broker. Which means that the broker has working capital requirement to run this type of business.

One of the ways brokers have managed it is by getting a bank guarantee (BG) from the bank. So all the customer funds instead of directly placed at the exchange, is placed as a BG. The BG usually has leverage, so for example if broker keeps Rs 100 crores of funds with the bank, the bank gives BG for another Rs 100 crore. Now the total funds at the exchange is Rs 200 crores, the additional Rs 100 crore used by broker to give the intraday leverages or margin funding. But the bank will give this additional Rs 100 crore by taking a credit risk on the broker, so in a way it is almost like a loan. Banks give the BG because they earn from it, 0.5% to 2% of the BG amount. So for a Rs 200 crore BG (max validity 1 year), they would earn between Rs 1 to Rs 4 crores.

Anyways, back in 2016 exchanges put a restriction on maximum BG that can be taken from a bank - it was around Rs 60 odd crore for a broker per bank, which got extended to Rs 90 odd crore last year. This restriction lead to the birth of an alternate product - partially funded FDRs, which worked very similar to a BG. Banks give a short term loan (STL) on an FD parked with them, and issue the larger sized FD to be parked with the exchanges. So if Rs 100 crores is parked as an FD by a broker with the bank, the bank gives STL of Rs 100 crores and issues FD for Rs 200 crores. And yeah, with similar charges like the BG.

We have taken BGs in the past, but have had none for a while now. I don’t know if this is a systemic risk, this is essentially the bank giving a loan to a broker. I am assuming they wouldn’t give it beyond what their credit risk models would allow. With the new SEBI circular disallowing intraday leverages in phases, the only working capital requirement for the broker would eventually be only for margin funded trades. If this BG or partially funded FD route goes away, it is going to get tough for the not very well capitalized brokerage firms.

The regulatory environment for brokers has changed significantly in the last 10 years. There is something called enhanced supervision where the broker has to report individual customer wise balance and prove that it is all there. This weekly reporting will soon be daily.

@nithin

Intraday leverage is capped. But some ppl are saying that bank brokerages and some other full services broker will continue to give leverage in delivery trades using “Margin funding”. Is this true?

Is margin funding not leverage?

There is a framework for providing leverage on equity delivery trades under MTF (Margin funding). But even here, the minimum VAR+ELM has to be collected. We should have this at Zerodha soon as well.