- Can we take delivery of short options (In equity it is not allowed)?

- How safe is selling strangle strategy, and how is it safe (I’m not considering theta here) (Any premium can grow infinite, but when it reduces, it can reduce max. by 100%, Suppose call rises by 200% in a time period, but put reduces only 50%, then how can I make profit by selling option strategy, am I not supposed to take a long position, since both the legs are changing together)

- We expect the premium to fall down with time to make profit, am I right?

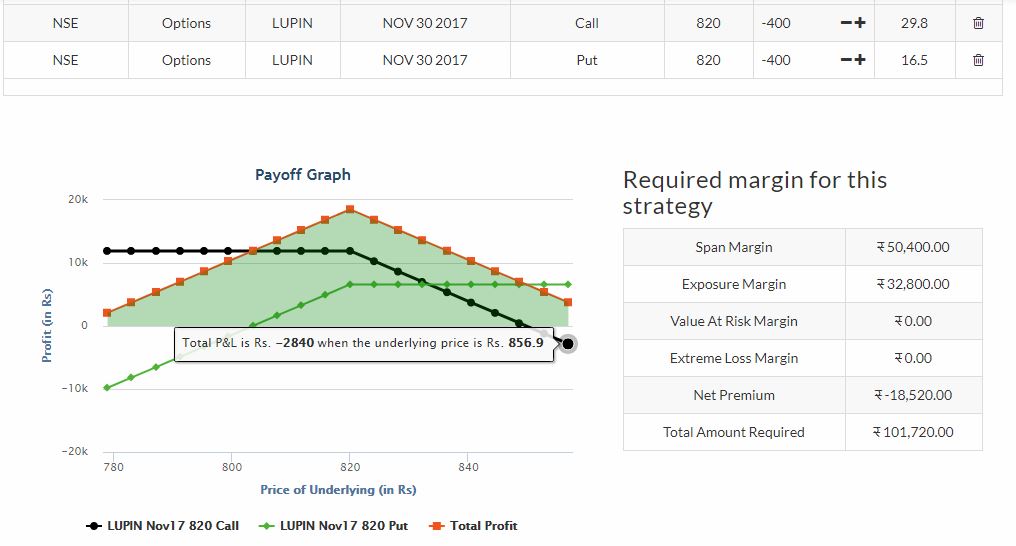

- is it possible to book only profit, without risking a single penny because I saw a payoff chart where there was no loss, whatever is the direction of the market

In the above payoff graph there is no loss up to a certain limit, no matter what is the direction of the market, Is it possible?

it will be helpful, If @nithin can reply

1 Like

@ASHISH_SINGH it is about selling STRANGLE…

1- Selling STRANGLE is LIMITED PROFIT with UNLIMITED RISK

2- Usually seller will sell OTM- call+ OTM put and expects the prices to settle between these strikes (call & put which has been sold)

3- Limited profit = which actually has been received by selling PUT+CALL- OTM and when option expires in between the strikes,

4- Same expiry to be used in this strategy,

5- Unlimited loss in case any of the sold call/put breach strike prices,

6- break even will be UPPAR BAND>>> strike price of call option+ total prem recd & LOWER BAND >>>>strike price of put option- total prem recieved…

THE STRATEGY TO BE USED WHEN RANGE BOUND EXPECTATIONS HAVE BEEN BUILT AND THE UNDERLYING EXPIRES IN BETWEEN CALL&PUT STRIKES…RISKY STRAGETY

Hey Ashish,

1) Can we take delivery of short options (In equity it is not allowed)?

Not sure what you meant here. NSE equity options are all cash settled. There is no concept of delivery

-

How safe is selling strangle strategy, and how is it safe (I’m not considering theta here) (Any premium can grow infinite, but when it reduces, it can reduce max. by 100%, Suppose call rises by 200% in a time period, but put reduces only 50%, then how can I make profit by selling option strategy, am I not supposed to take a long position, since both the legs are changing together)

A: Safety is a relative concept, as you already know. It is really a question of risk and reward.

Let us say NIFTY is at 10300. Let us consider three trade ideas:

| Straddle | Strangle 1 | Strangle 2 | |

|---|---|---|---|

| Option 1 | 10300 Put | 10200 Put | 10100 Put |

| Premium 1 | 100 | 60 | 30 |

| Option 2 | 10300 Call | 10400 Call | 10500 Call |

| Premium 2 | 100 | 60 | 30 |

| Total Premium | 200 | 120 | 60 |

| Profit Range | 10100-10500 | 10080-10520 | 10040-10560 |

As you can see here, the most aggressive trade is the Straddle. Since you have 200 Rupees premium, on expiry, you have a 200 point safety cushion from a sold strike. So you wont lose money till it moves 200+ point

Similarly, the other two are safer, because they give you a bigger safety cushion. But they are not as profitable. So the safer a trade, the less profitable it gets.

If you sell a straddle or strangle, and a huge move happens, it will make losses. And unlimted losses, theoretically

How to limit losses on Strangles and Straddles

Trade butterfly or condors.

In a butterfly when you sell a 10300 Call and put, you also buy a 10200 Put + 10400 Call, or 10100 Put + 10500 Call to limit losses

In a condor when you sell a 10400 Call and 10200 put, you also buy a 10100 Put + 10500 Call to limit losses.

But of course, in both butterfly and condor you will not have as high premiums as straddle and strangle because you will need to pay for the protection on buy options

3) We expect the premium to fall down with time to make profit, am I right?

Yes, you are totally right on this one. So if you sold a strangle, sat 10100 Put and 10500 Call, if NIFTY eventually ends between 10100 and 10500, you will make the full premium. And for each day it stays in this range without moving much, the premium will erode, thanks to theta.

4) is it possible to book only profit, without risking a single penny because I saw payoff a payoff chart where there was no loss, whatever is the direction of the market

Nope. It won’t happen. It will happen in the following situation:

You sell options, stock does not move much (means slight movement) AND

a) volatility decreases OR b) time passes

So yeah, when the spot largely stays at the same place, you can make money on time value or decrease in vol. But that is NOT rissk less because you always have a risk of spot moving, or vol increasing

In other words, if the money you lose by stock movement is compensated by theta or vol decline, you will make money

1 Like

Whats your opinion on the above given payoff graph?

if some is again has to buy call+put to cover its short strangle then there is no point to go for STRANGLE…rather exiting at the point in time when certain losses occured…

The payoff chart seems to be correct but it it not showing the complete picture. Lupin above 866.3 [820+(29.8+16.5)] and below 773.7 [820-(29.8+16.5)] will start making a loss in this strategy.

Yes, I agree

My doubt is, If it is trading within the specified range of 780 to 850, then is the above graph practically possible?

That’s why I mentioned the same in my question

Oh okay. Actually, this graph is on expiry basis. As price keeps fluctuating within this range before expiry, you will notice MTM loss or profit depending upon many factors(like volatility change, price moving towards the breakeven points or price moving back to the strike prices from the breakeven points, etc).

Can we backtest straddle/strangle in Pi

If yes, then how?

Options Oracle by Pasi is a great free tool that does that.

1 Like

@ASHISH_SINGH Can you tell from where did u make this payoff graph and margin calculation. If possible can you share.

Upstox has a options strategy builder (https://upstox.com/tools-and-calculators/option-strategy-builder/) and that is the one being used here. It takes prices from previous closing price.

If you need a much more accurate payoff graph, with recent price I suggest you to checkout zerodha varsity options strategy module