I need to invest 50L apart from Stocks with 10% to 12% Yearly return, any idea or suggestion ?

What is time horizon? typically more the return you want more you have to face volatility.

e.g. If you want yearly 10-12% return averaged out for 12-15 years, any index fund would do. but its avarage. few years it may be negative, few years it may be 20%.

if you want every year 10-12% return, one possible investment avenue is fixed income instruments like bonds… but for such high returns one has to compromise on rating.

goldenpi is one of the site from where you can buy fixed income instruments .You can visit website /google further to get more information.

2 Likes

thanks, and as I said earlier I don’t need exposure in stocks that include ETF and MT also. I am expecting advice on debenture and bonds.

Check bondbazaar also .

You can invest in Arbitrage PMS which has given 11.8% for last 10 years.

Arbitrage involves Stocks but it has never given negative return in a month.

But as per SEBI regulations minimum investment in 50 lakhs.

1 Like

thanks will do

Do you know any PMS? possible to suggest?

You can find basic information here GrowFolio Invest with top PMS managers

You can schedule a discovery call with them

Is arbitrage mutual fund same as arbitrage pms

Saw a video on arbitrage fund after reading your post. Sounds like a relatively risk free investment

Need to figure out if these funds give out consistent returns equal to Fds at 8.25 pretax returns as i sign and give 15g for tax purposes.

Going forward since 12 l is exempt, higher corpus of fd can be placed. 50 l at 8.25 gives a return of 412500

Wonder if there are ETFs for the same.

Thanks for your reply learnt something new

1 Like

thanks but Already have that kind of investment. If you have any other investment type other than stocks please share

You have to consider few details while investing in Arbitrage PMS.

You have to pay capital gains tax on any gains.

The hurdle rate at which they take part of profit.

Listed NCDs can be alternative but you have to look out for opportunities and usual credit risk, liquidity risk, interest rate risk are present.

Private credit and AIF’s can offer returns but carry high risk.

1 Like

It’s for Arbitrage Mutual funds, Since Arbitrage PMS uses FD and Futures it’s taxed at Slab rate.

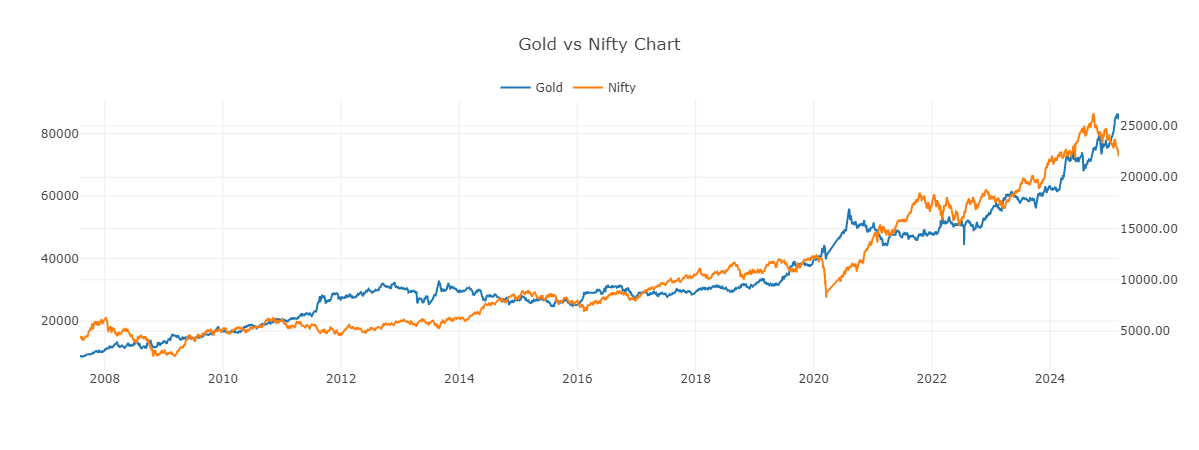

Another first for me, I never thought Gold can be a HEDGE against Nifty 50. Read the article, not convincing though as most part of the article does not say that it directlly acts as a hedge. The only reason I can think of is when markets fall, people might go for Gold investment and not as a direct hedge against nifty 50 stocks.

Is Nifty 50 and Nifty 50 equal weight a good balance - not truly hedge but does it counter balance a little when market falls.

- Look at all the crashes in stocks in past and see how gold behaved in that time. Anything that is atleast not correlated with stocks will help reduce loss, so debt too will help.

And i have heard that gold has a bit of negative correlation in such times, ie on avg they might go up a bit. Never checked this myself and i have never invested in gold ( might in future if this tests out ok). - Even Gilt 10Y might have negative correlation sometimes when equity crashes, as govt might drop yields. Not always perhaps.

- Nifty equal weighted - I think it would be very similar, certainly nowhere near equity+gold in terms of diversification. But best to test all this yourself.

1 Like

Gold is considered as hedge as its up/down are not co-related with nifty 50… rather it may be negatively co-related.

Consider when some is in withdrawal phase. it makes sense not to take out money from from nifty 50 when its going in bad patch. it will erode principle amount. if there is asset,which is fairly stable when nifty 50 is down, withdrawal can be that asset instead of nifty 50.

see

from Gold vs Nifty Chart - i am market

it may not be perfect hedge, buts it one of the best hedge to protect drawdowns in nifty50

2 Likes

Apparently not.

Here are a couple of studies [1] [2] that go into the math

to explore various statistical measures of correlation.

Anyway, if we think about it,

we wouldn’t want to invest in something

inversely/negatively correlated with NIFTY50

as doing so would negate any potential gains from NIFTY50, right? ![]()

Instead what we actually want is…

Pretty much this.

In times of extreme volatility that trigger equity drawdowns,

gold and gold-backed assets tend to hold their value.

Looking at this plot,

specifically the area under the curves,

and seeing how they are very similar,

i wonder whether most folks would be

- happier investing mostly in gold/gold-backed assets

- and using NIFTY50 to hedge some of the risk’s associated with a gold portfolio.

Risks like 3, 7, 15, 20, 24 of this list…

24 Types of Risk

- Losing money – The possibility of permanent loss is the main form of risk.

- Falling short – Not having to make necessary payouts or income to live on.

- Missing opportunities – Not taking enough risk.

- FOMO (Fear of Missing Out) – Jumping on the bandwagon of risky investments for fear of living with envy.

- Credit – The risk that a borrower will be unable to pay interest and repay principal as scheduled.

- Illiquidity – The inability to sell when you need the money.

- Concentration – The risk of not being diversified when sectors drop in value.

- Leverage – Losses are magnified when investments decline in value by using borrowed money.

- Funding – The need to make a capital call when a loan comes due.

- Manager – The risk of picking the wrong one.

- Overdiversification – The standards of inclusion may drop leading to the potential of lower risk-adjusted returns.

- Volatility – This introduces an emotional component that may result in a permanent loss from selling too soon.

- Basis – This applies to arbitrageurs who go long one security and short another based on one being cheaper than the other and common patterns repeating themselves and yet something goes awry where the relationship breaks.

- Model – Excessive belief in a model’s efficacy can lead to excessive risk taking.

- Black Swan – Just because something hasn’t happened doesn’t mean it won’t happen. This is the statistically inconceivable event that materializes.

- Career – If rewards are shared asymmetrically then it may not be in a money manager’s best interest to take risks where there could be short term pain, but long-term pain for fear of losing clients or his or her job.

- Headline – This is when losses are big enough that they can potentially generate media attention.

- Event – Tends to apply to bondholders when the equity owners leverage up the company and put the bonds at more risk.

- Fundamental – Assets or companies underperform in the real world.

- Valuation – Overpaying for an investment.

- Correlation – Being less diversified than expected. Everything goes down much to the surprise of an investor.

- Interest Rate – The risk that higher rates can lower the value of fixed income securities and other yield-oriented investments.

- Purchasing Power – The risk that cash received in the future will be eroded in value due to inflation.

- Upside – The risk of being under-exposed to very good economic and financial events that occur in the future.

Source : Howard Mark’s “Risk Revisited Again” memo .

Thoughts? ![]()

- As a trader, i dont care too much about day to day correlation. When i test, i would look at different types of crashes and see how gold holds together preferably from 1990s or earlier. But i guess we can see and it looks well in recent years. ofc there is no guarantee, and crashes are a limited sample.

- Negative correlation is the holy grail for reducing risk. But these things shift around, so i wouldn’t increase risk depending on correlation to reduce risk ( hopefully sentence made sense).

Obviously if its 1:1 then we dont make money, but if both instruments make money in long run, that wont happen. - Gold only ? - Dunno, things change, i wouldn’t depend on 1 thing, even equity. If central banks stop purchasing gold, it will probably stop rising. Or maybe some other reason. Gold can crash too. Even 100 year data would still not be enough for me to consider anything crash proof, but just searching over it seems to suggest it may have fallen > 50% in past.

Because gold is doing well recently, there will be a bias towards it too.

Also INR helps, so that is good for gold. If USD gets weaker than INR for any reason ( dont see it but wont depend on it), then again gold will probably struggle. Anyway, i have never invested in gold. So there is that.

No idea if this is accurate, but in 2008 gold seemed to have crashed too. Nice ![]()

When everyone wants liquidity and people are selling everything and going to cash, not much one can do.

Its low in priority for me, so not looking at it yet. Ray Dalio i think suggests Equity + Debt + gold + commodities ( dunno exactly )

I think we are drifting away from original thread…

Actually its other way round. Astute investor will look for negative or weak correlation.

There is bit theory behind it, which says if we select asset class with no correlation and re-balance portfolio based on some trigger either you will have lower drawdowns at same returns or slightly better returns . Refer to modern portfolio theory by Harry Makowitz

yes… nothing is perfect including modern portfolio theory!. It does not protect from systematic risks in which entire financial machinery fails.

yes its individual choice. For someone who is dependent on investments as primary source of income in immediate future, its one of the avenue to protect from larger drawdowns in early years of withdrawal (squence of returns risk)

yah… but for Indian mutual fund investor Indian equity+ debt +gold+ foreign equity basket is available

New Funds will have an option to use derivatives including commodity derivatives, i think upto 25%. They could probably come up with some sort of all seasons funds, dunno. Shorting also could be used to improve, but we will need to have trust in ability of Mutual funds.

Hopefully, in few years we could have same confidence as say we could have in Prashant Jain or Naren or per perhaps PPFAS or even index funds.

yeah, also esp in retirement having better than debt but not as maniacal as 100% equity would be a good option. Need to increase real returns, debt don’t give that much. 1% vs 4-5% could be a lot different. Equity + debt is ok, but we should try to do better.

I trade, so from my pov, i want to try active stuff over passive for now.