Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and video on YouTube.

You can also listen to The Daily Brief in Hindi.

Today on The Daily Brief:

- Will Swiggy hit a sixer like Zomato?

- Are India’s semiconductor dreams becoming a reality?

- Will our groceries become expensive?

Will Swiggy hit a sixer like Zomato?

Swiggy, the popular food delivery giant, is gearing up for one of the most talked-about IPOs in India’s startup scene. If you’ve been keeping an eye on the market, you know this is a big deal—especially after the IPOs of Zomato and Paytm.

Swiggy is looking to raise ₹3,750 crore by issuing new shares, with additional shares being sold by investors like Prosus and Accel, bringing the total IPO size to over ₹10,000 crore.

But the big question is: how does Swiggy stack up against its main rival, Zomato? What makes Swiggy different?

Let’s break it down.

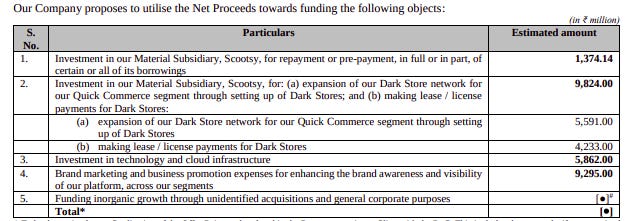

Swiggy plans to use the funds from its IPO for a few key projects. First, they’re setting aside ₹982 crore to expand Instamart, their quick-commerce service that promises grocery deliveries in under 30 minutes. This means a major push into opening more dark stores, which are small warehouses designed for speedy deliveries.

On top of that, another ₹930 crore will go towards marketing and brand promotion. The message is clear: Swiggy is doubling down on grabbing more market share, especially in the competitive quick-commerce space.

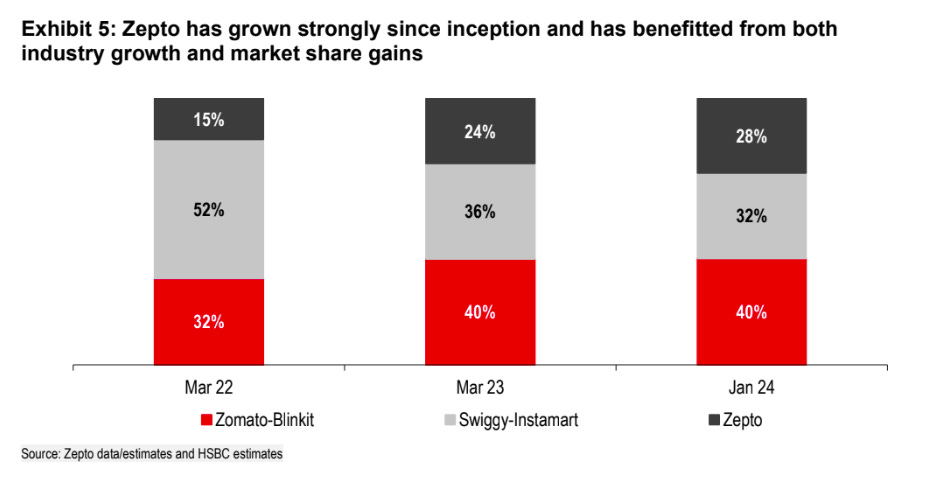

Interestingly, Swiggy was the first major player to jump into quick commerce in India with Instamart. That early start should’ve given them an edge, right? But then Zomato shook things up by buying Blinkit, which now holds about 40% of the market, compared to Instamart’s 32%. Zepto also joined the race, adding even more competition.

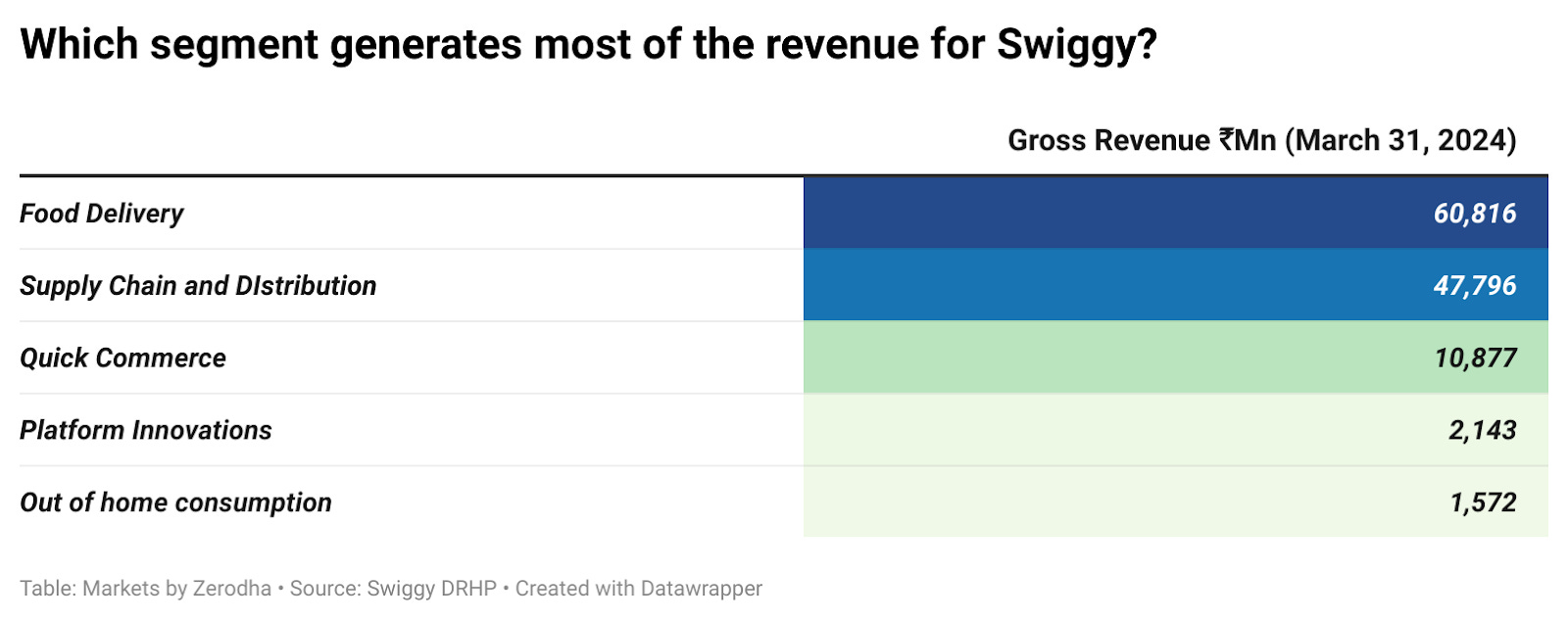

While Instamart has boosted Swiggy’s presence, it’s only their third-largest source of revenue. On the other hand, for Zomato, quick commerce has become their second-biggest money-maker, largely thanks to Blinkit’s rapid growth.

Looking at the bigger picture, Swiggy and Zomato have diverse business models, but their revenue sources differ a bit.

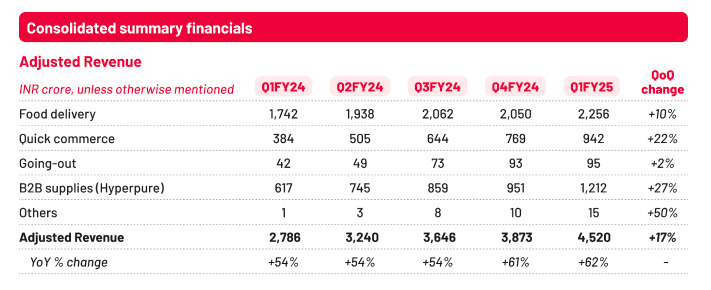

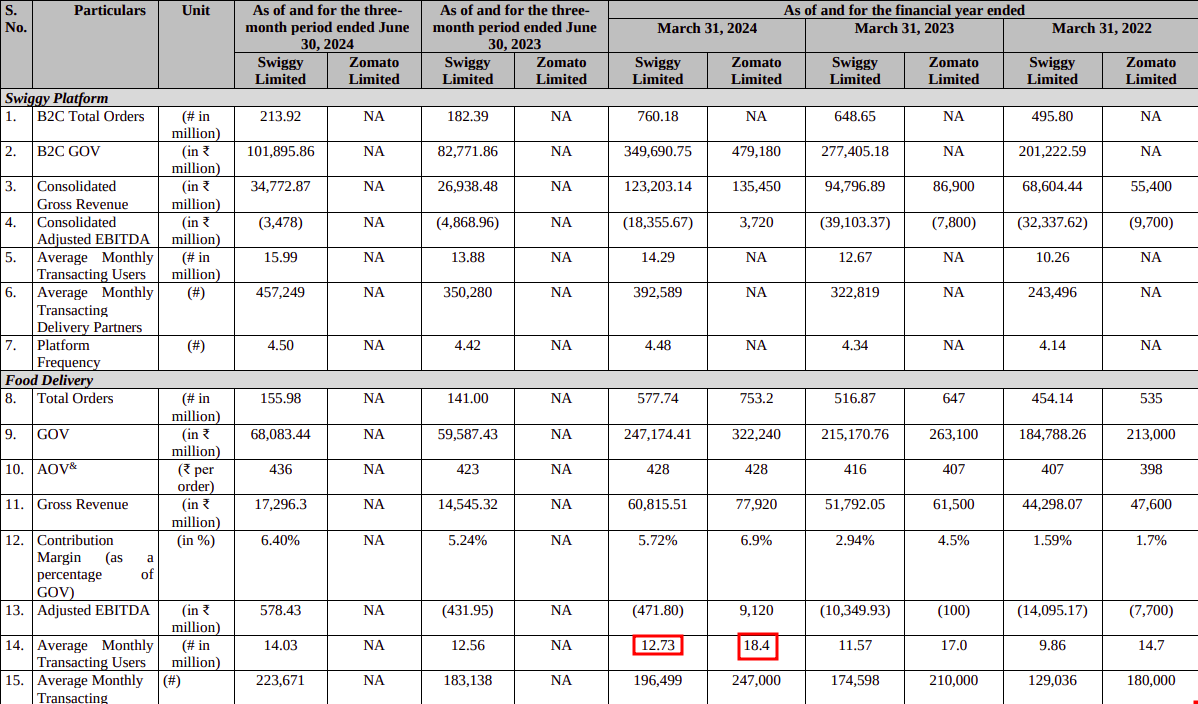

Food Delivery : This is still the main focus for both. In Q1 FY25, Swiggy’s food delivery gross order value (GOV) hit ₹10,189 crore, growing 23%. But Zomato outpaced them, growing 53% to ₹15,455 crore. Zomato is leading here, with 18 million monthly active users compared to Swiggy’s 12 million.

Quick Commerce : This is where things heat up. Instamart saw revenues of ₹403 crore, a strong 90% increase. But Blinkit more than doubled that, with ₹942 crore in revenue, growing 145%. The take rates—basically, how much they earn from each order—also tell a similar story: Blinkit’s take rate is 19.1%, while Instamart’s is 14.8%. Despite Swiggy’s early start, Zomato has jumped ahead in this space.

B2B Supply Chain : Swiggy’s B2B services, including warehousing and logistics, brought in ₹1,268 crore in Q1 FY25, making it their second-largest revenue stream. Zomato’s equivalent, Hyperpure, is growing but still smaller in comparison.

One of Zomato’s biggest strengths is profitability. In Q1 FY25, Zomato posted a net profit of ₹253 crore, while Swiggy reported losses of ₹611 crore. Even Blinkit’s losses are smaller compared to Instamart’s, giving Zomato a slight edge in terms of efficiency.

Both Swiggy and Zomato dominate India’s food delivery market, but Zomato is currently leading in both food delivery and quick commerce. Blinkit’s aggressive growth and better efficiency have helped it pull ahead of Instamart. Although Swiggy has 557 dark stores for Instamart, the fight for market share is still on, especially in Tier 2 and Tier 3 cities, where the next big growth is expected.

Swiggy’s quick-commerce journey goes back even further. Remember Scootsy? Swiggy bought the premium food delivery service in 2018 to focus on high-end restaurants. While Scootsy didn’t change the game, it did help Swiggy expand its offerings, especially in Mumbai, before it was eventually merged into Swiggy’s main platform.

So, what’s next for Swiggy?

As Swiggy gears up for its IPO, it’s got a strong growth story to share. With a mix of revenue streams, an early start in quick commerce, and a solid user base, Swiggy has a lot going for it. However, Zomato’s lead in both food delivery and quick commerce means Swiggy still has some catching up to do.

The next few years will be crucial. Both companies will continue to battle, especially in quick commerce, where growth in India’s smaller cities could make a big difference. How Swiggy handles these challenges will be key to whether its IPO meets the hype.

Are India’s semiconductor dreams becoming a reality?

Now let’s dive into Tata’s big bet on semiconductors and why it could be a game-changer for India’s tech future.

Right now, India’s chip-making industry is still pretty underdeveloped. We’ve made some strides in assembling, testing, and packaging chips, but the actual manufacturing part? We’re not quite there yet. But Tata is looking to change that and is making some bold moves.

But before we dive into that, if you’re wondering what the heck a semiconductor chip is and why it’s such a hot topic, here’s a quick 10-second explainer:

Think of semiconductor chips as the “brains” behind all your electronic devices. They process information, store data, and control how our devices work. From your smartphone, computer, and car, to even your washing machine—semiconductor chips are what make these devices “smart” and able to handle complex tasks.

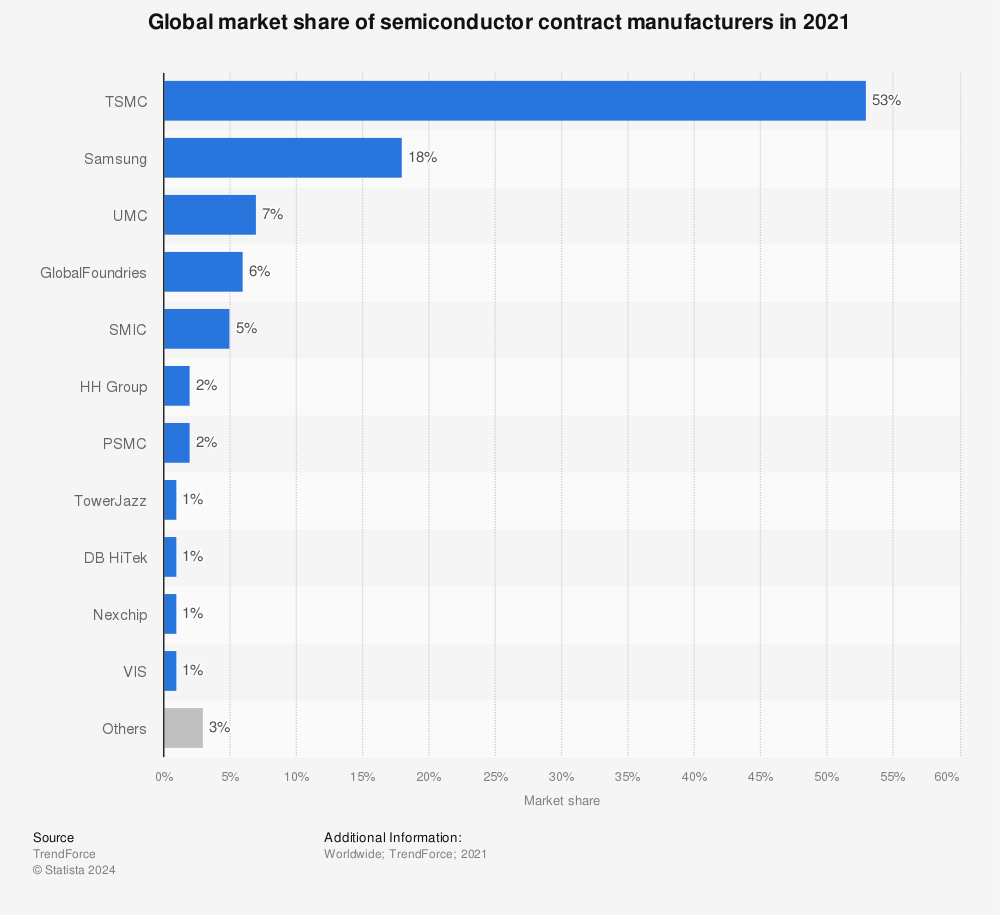

Now, back to Tata. They’ve recently teamed up with Powerchip Semiconductor Manufacturing Corporation (PSMC), one of the world’s top chip makers, to build India’s first semiconductor fabrication plant, or fab, in Dholera, Gujarat.

By the way, don’t mix up PSMC with TSMC—they’re both Taiwanese chip companies, but TSMC is the largest in the world, while PSMC ranks 7th. Tata’s partnership is with PSMC.

So, why is this partnership such a big deal? PSMC will help Tata with everything from design to transferring key technologies to India. This fab will produce up to 50,000 wafers per month—those are thin slices of semiconductor material that eventually become the chips powering our devices.

Tata is pouring a massive ₹91,000 crores into this project. But it’s not just about building one factory; they’re setting up an entire ecosystem for semiconductor manufacturing in India, potentially creating 20,000 skilled jobs initially, with plans to scale up even more.

But why should we care?

Semiconductors power almost every piece of tech we use, and right now, India relies heavily on imports. Tata’s fab will make logic chips, which are super important for tech like AI and high-performance computing. With the global chip shortage, Tata’s move could position India as a key player in the global semiconductor market in the long run.

But it’s not going to be a walk in the park. Companies like TSMC and Samsung have spent decades perfecting their manufacturing, and even they still face challenges. That’s why Tata’s partnership with PSMC is so crucial—it’s the boost they need to get this off the ground in India.

Looking ahead, Tata plans to build multiple fabs in Dholera, which could create over 100,000 jobs. However, there’s a catch—India has always faced a shortage of skilled workers, especially in high-tech fields. The good news? Tata is tackling this head-on by investing in workforce development as part of the project! They’re planning hands-on training for Indian engineers at PSMC’s facilities in Taiwan to ensure they have the skills to operate these complex fabs.

In short, Tata’s big semiconductor push could be a major leap towards India becoming a key player in the global chip supply chain. As the demand for chips keeps growing, this could set India up as an essential alternative supplier in the future.

Will our groceries become expensive?

Motilal Oswal recently released a report on commodity prices, pointing out some trends that investors should keep an eye on. Here’s a quick rundown of what’s happening.

First up, agricultural commodities are getting pricier. Wheat prices are up 11% compared to last year, and barley has jumped by 15%. This isn’t great news for companies like United Breweries and Nestlé, which depend heavily on these ingredients. Coffee prices are also rising, up 14%, which could mean higher costs for brands like Nestlé and Hindustan Unilever.

So, what does this mean for us? It’s likely these rising costs will eventually be passed on to us as consumers, meaning our grocery bills could go up soon.

Next, let’s talk about the edible oil market. Import duties on oils like palm, soybean, and sunflower have risen from 0% to 20%, and refined oil duties are now at 32.5%. While this move is designed to support local producers, it’s putting pressure on FMCG companies like Britannia, Dabur, and Marico, which use these oils. As a result, we might start seeing price hikes on items like biscuits and cooking oils.

But it’s not all bad news. Prices of non-agricultural commodities, especially crude oil, are cooling off—they’re down 7% from last year, mainly due to China’s economic slowdown. This is good for companies like Asian Paints and Pidilite, which could see better margins thanks to lower raw material costs.

However, inflation is still a challenge for FMCG companies. Key inputs like wheat, sugar, and milk are up about 4% from last year, putting pressure on giants like Hindustan Unilever and Britannia. To protect their margins, we might see more price increases on everyday products in the coming months.

So, while some sectors might catch a break, inflation is still hitting the food and FMCG space hard. We should brace ourselves for more price hikes on household goods soon.

Tidbits

- ChrysCapital is set to buy Theobroma Foods and Belgian Waffle Co for a combined ₹3,200-3,500 crore. They’re looking to build a consumer brand investment platform, tapping into India’s growing food market, which is projected to reach ₹7.76 lakh crore by FY28.

- Appario Retail, once Amazon India’s top seller, has gone to court to challenge the CCI’s antitrust investigation, which accuses Amazon and Flipkart of favoring select sellers. This could set a trend for other companies fighting regulatory actions.

- OpenAI is restructuring into a benefit corporation to attract investors and potentially hit a $100 billion valuation. This comes after some leadership changes and aims to balance AI growth with ethical considerations.

- India announced a small wage hike for informal sector workers starting October 1, to keep up with rising living costs, with adjustments linked to inflation trends.

- Accenture reported Q4 2024 revenue of $16.41 billion, driven by demand for generative AI solutions, and announced a $4 billion share buyback, showing strong confidence from investors.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()

If you have any feedback, do let us know in the comments