The banking crisis, starting with Silicon Valley Bank and Credit Suisse, has raised concerns about the safety of keeping people’s hard-earned money in banks. Everyone is now concerned about whether they will be able to access their savings if there is another crisis in the future. Everyone is reducing their funds from banks and looking for safe investment options as a solution.

G-secs and T-bills, which are government-backed and issued by the RBI, are one such safe option. These are considered risk-free because they are backed by the government, and G-Secs with a maturity period of less than one year are known as T-Bills (Treasury bills), while those with maturity periods greater than one year are known as Bonds.

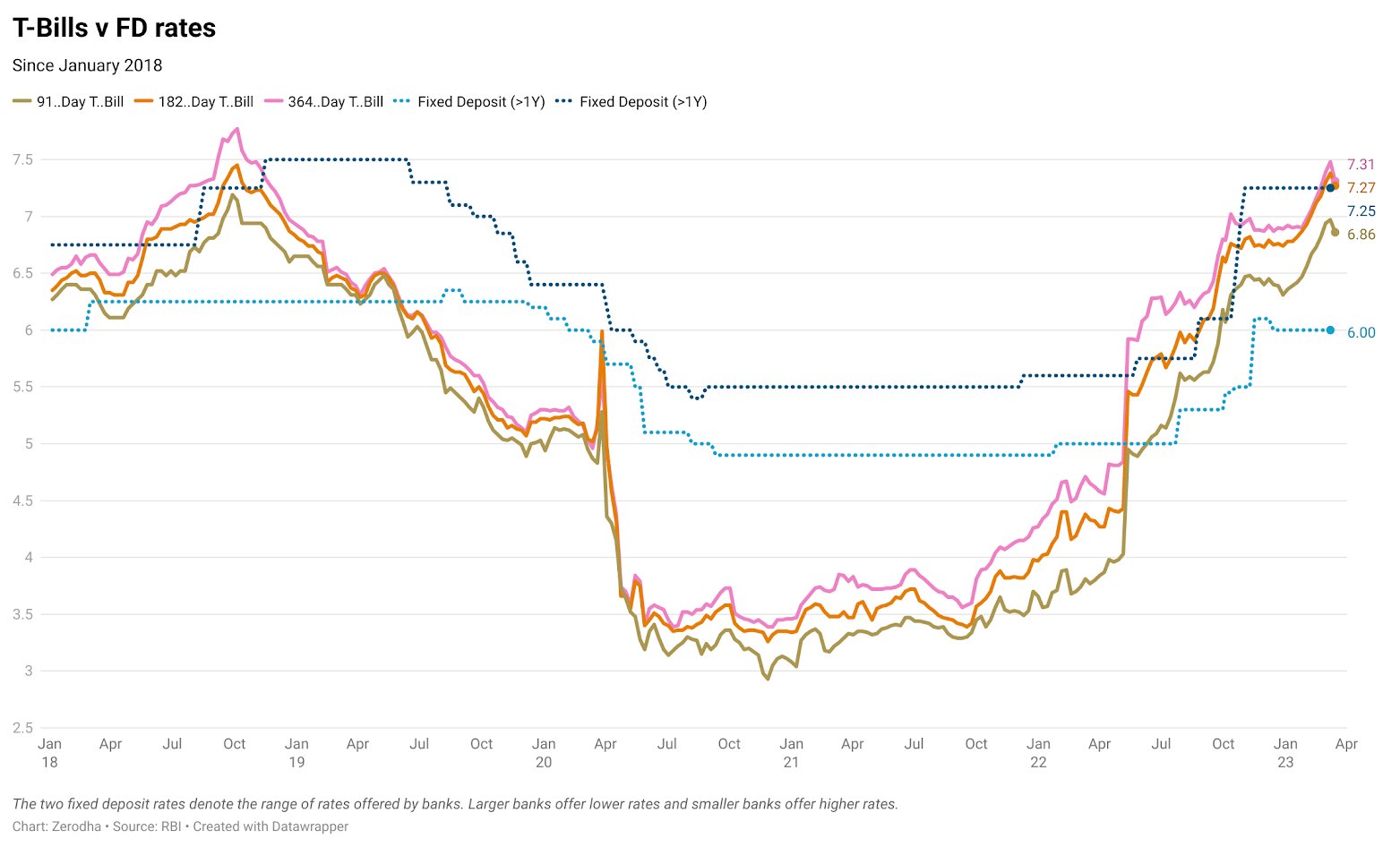

Here is a historical rate comparison of T-bills and FDs from Nithin’s tweet.

I don’t think that is correct, as banks may take a while to adjust their interest rates, but bank FDs will give more interest than government bonds. As it is obvious that when there is sovereign guarantee payout bounds to be less, and as banks are in lending business, they need funds so they give more to their depositors than the prevailing government bonds’ rates. And private banks give a bit more. And there is senior citizen advantage, if the investor is of that age.

So the interest rates in this sense are dynamic, as there is lag, don’t truly present picture.

I am an investor in FDs from PSBs and I have the experience of buying T-Bills from Zerodha.

I don’t know if we can sell T-Bills in the middle of the tenure, I never did. Can this be done, does such market exists as with other government bonds, because T-Bills have less than 1 year maturity and come in different tenures.

[quote=“nithin_kumrr, post:1, topic:144768”]

Everyone is now concerned about whether they will be able to access their savings if there is another crisis in the future. Everyone is reducing their funds from banks and looking for safe investment options as a solution.

Really, I thought people were only moving money from smaller banks to bigger banks.

I thought your article should have stressed how equity investors in these banks have lost substantially whilst Depositors money was safeguarded. AT1 Bond, I am told lost almost 17 billion in one of the article from the credit suisse saga.

How come you have not mentioned this. You been stressing that Everyone is concerned. Not sure who is concerned and who has moved money from banks and keep cash at home.

With regard to credit suisse, their central bank has given a line of 70 billion plus so that people who want to move the money can do. How come this was not stressed upon.

Quote

Swiss authorities, taxpayers

Finma became the first regulator to watch a bank deemed systemically important have to be rescued since the financial crisis. The Swiss government had to step in an provide billions of francs in guarantees to UBS and the central bank was forced to provide extensive liquidity backstops to facilitate the rescue, putting taxpayers at risk 15 years after they bailed out UBS. Swiss Finance Minister Karin Keller-Sutter acknowledged it was the only way to stabilize international financial markets. Lots of Swiss money is being put up to help absorb any shocks from the deal, from a 9 billion franc guarantee on possible losses to huge credit lines from the Swiss central bank.

Unquote.

Going by your post, why would the central bank do anything at all.

U can sell in open NSE markets. but liquidity is non-existent. So better go to the Auction market where u can bid with bigger players for reasonable price. that is outside Zerodha and step into RBIRetail website.

While the idea of making profit exists with a lot of products, liquidity is also important, so as to not get stuck with the investment if there are no sellers, when the product was bought to sell soon.