I understand that sometimes due to ambiguity, the tax laws can be open to multiple interpretations, however, in the case of TATA Motors DVR, i believe there is no ambiguity, and the views expressed by the Host in this video is misleading and most probably wrong for the following reasons.

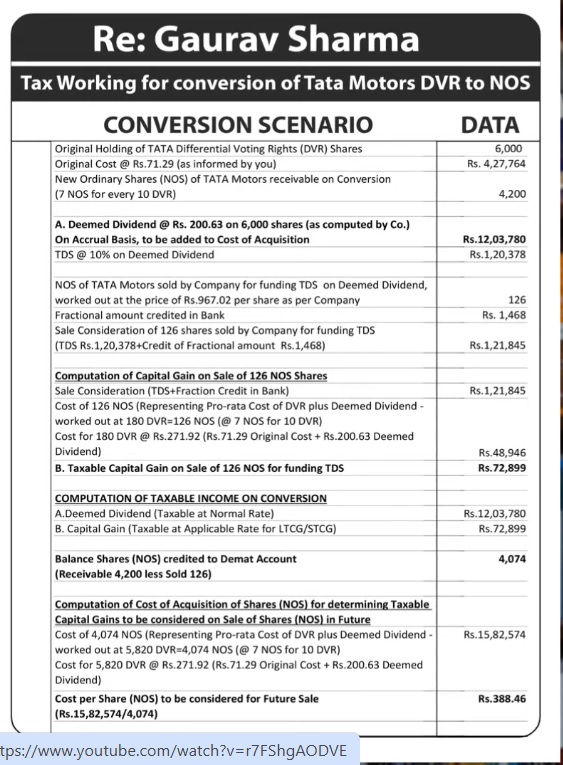

I believe this  was the conclusive notes that you were referring to.

was the conclusive notes that you were referring to.

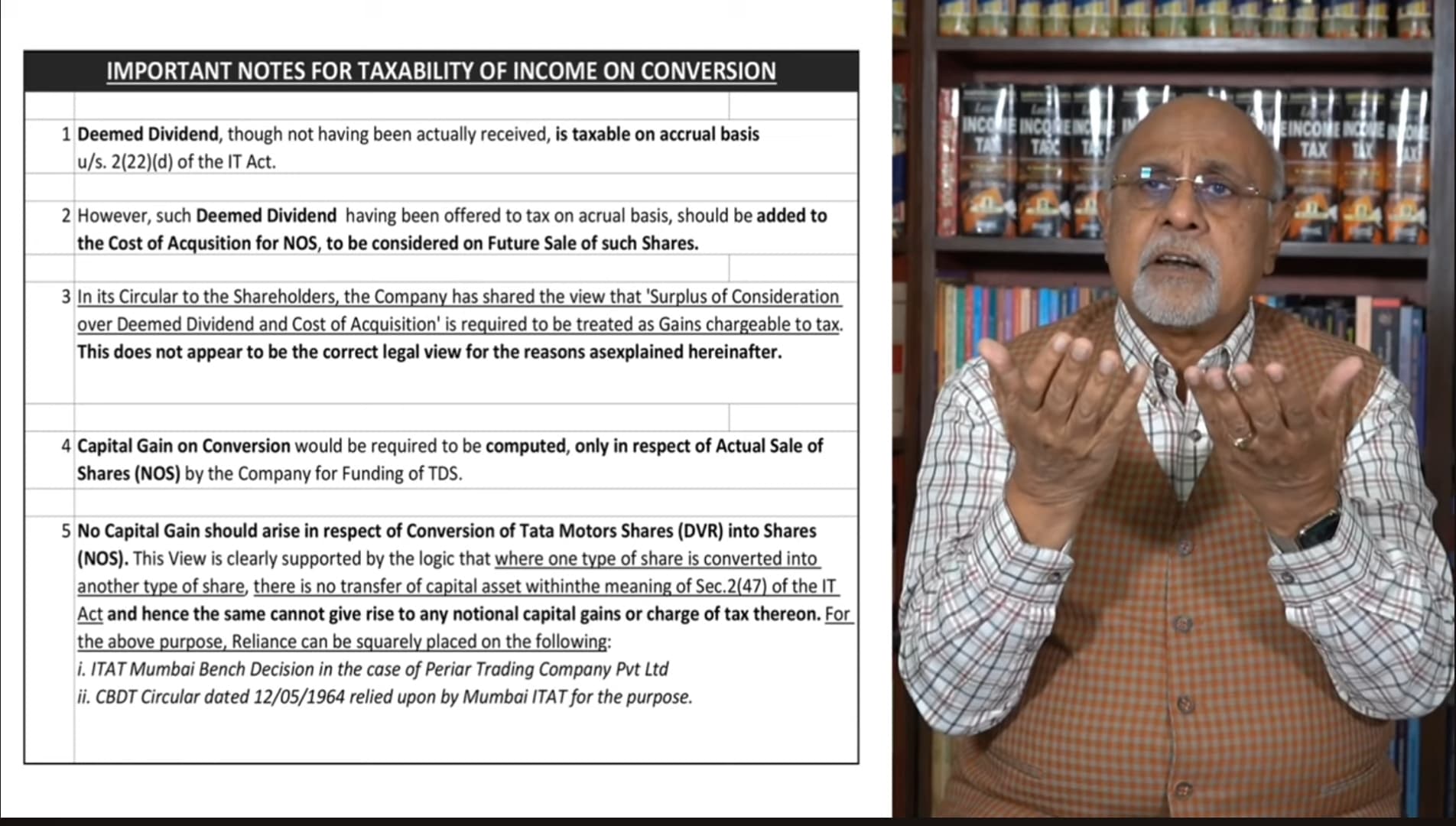

As you can see in Note 3) in the video, the host, seems to disagree with the circular issued by TATA motors to its shareholders regarding the tax implications of cancellation of the DVR shares.

He seems to contest with the capital gains taxation part of the circular, stating that the views expressed by TATA Motors doesn’t appear to be legally correct

And supports that by Note 5) saying that this is merely a conversion of DVR into NOS and therefore there is no transfer of shares and so, the capital gains will arise only at the time when the NOS shares are sold.

IMHO, the above argument is absolutely wrong

- He is indirectly implying that the legal team of TATA Motors were wrong in interpreting the tax laws and has mislead the shareholders by stating incorrect facts. Do you really believe that a company as big as TATA Motors would not have hired professional CA/consultants before issuing such circulars ?

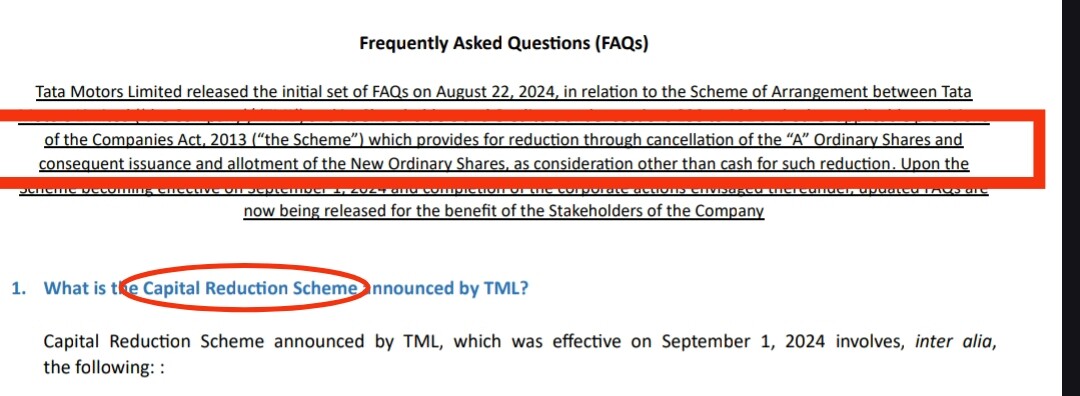

Here’s the official video issued by TATA Motors explaining the tax implications of cancellation of DVR shares.

-

The scheme is called capital reduction,not conversion, the key word here is capital reduction and cancellation of DVR shares through consideration other than cash

-

Capital reduction is generally considered a “transfer” under the Income-tax Act, 1961, specifically within the meaning of section 2(47). This is because the reduction of share capital, whether through a reduction in face value or by paying off a portion of the share capital, results in the extinguishment of the shareholder’s rights to that extent

-

Extinguishment of Rights:

When a company reduces its share capital, it essentially cancels out some of the shareholder’s rights associated with those shares. This can include the right to dividend payments, the right to share in the company’s assets upon liquidation, and potentially the right to vote.

Transfer under Section 2(47):

Section 2(47) of the Income-tax Act defines “transfer” in relation to a capital asset. It includes not only sale, exchange, or relinquishment, but also the extinguishment of any rights in the

The cancellation of Tata Motors DVR (Differential Voting Rights) shares and their conversion into ordinary shares involves the extinguishment of certain shareholder rights. Specifically, the DVR shares, which had lower voting rights and a different dividend structure compared to ordinary shares, are being canceled and replaced with ordinary shares. This means the unique rights associated with the DVR shares, primarily related to voting and dividends, are being eliminated.

The expression ‘extinguishment of any right therein’ is of wide import. It covers every possible transaction which results in the destruction, annihilation, extinction, termination, cessation or cancellation, by satisfaction or otherwise, of all or any of the bundle of rights, qualitative or quantitative, which the assessee has in a capital asset, whether such asset is corporeal or incorporeal.

So, in conclusion, the views expressed the host in that video is misleading and contradicts not only with the circular issued by TATA Motors, but also with the Income tax act, when it comes to the taxation of the capital gains of DVR shares upon cancellation.

TL;DR

Irrespective of whether the new ordinary shares are

sold or not, we are required to report the capital gain/loss on cancellation of DVR shares, as all DVR shares held on 1/Sep/2024 are assumed to be transferred on that day.