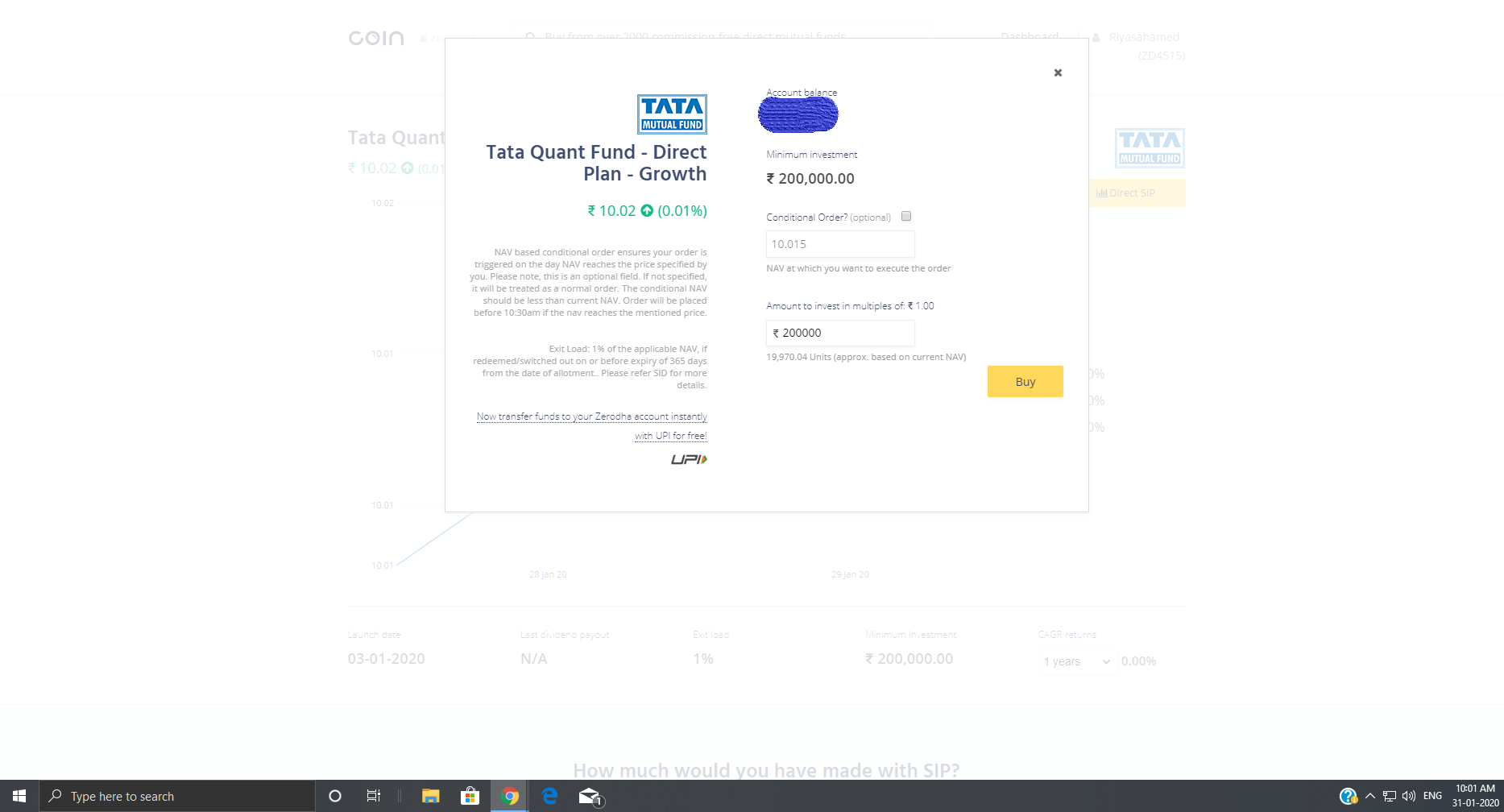

Tata Mutual Fund launched its Artificial Intelligence & Machine Learning driven Mutual Fund - Tata Quant Fund on 3rd January 2020.

NFO Period : 3rd January 2020 to 17th January 2020

Fund Manager : Mr. Sailesh Jain

Let us know more about the fund!

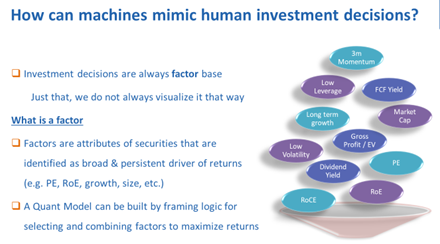

Predictive Power of Machines

As we know, prediction is at the core of investments. Investing is predicting. Machine driven predictive models are increasingly bringing artificial intelligence closer to our day to day lives. A fairly dated example of AI based prediction was that of Deep-blue, an IBM developed system that beat the reigning world chess champion during 90’s.

Fund management requires complex set of predictions. Fund managers along with research analysts process diverse and voluminous information for making investment decisions. Actively managed funds benefit from human intelligence that learn, comprehend, break down problems and respond in a complex manner. Passively managed funds, on the other hand, are rule based and they minimize human judgement. Their strength lies in increased objectivity and in elimination of human biases or errors. However, they can be prone to oversimplification and lack instinct or innovation. There’s no right or wrong amongst either styles. They have contrasting pros and cons.

Artificial intelligence can add a third dimension to these contrasting styles. It can mimic human judgement to a good extent while retaining the benefits of disciplined passive investing. For mimicking human judgement, an AI system must process large data sets, build predictive models and then choose best available option for generating future returns. A fund or scheme constructed in these lines can broadly be called a Quant Fund.

Quant modelling at Tata Asset Management Company Ltd:

Passive funds along with quants are rapidly gaining popularity in advanced markets like the US and Europe.

The structures and strategies employed in these funds have evolved significantly over time with many notable contributions. In view of these and also the increasing adoption of AI solutions in India, last financial year, Tata Asset Management Limited had decided to put together a team specializing in data science to venture into quant models. This team started work by extensively studying passive investment strategies that can be adopted to Indian equity mutual fund markets. The study comprehensively tested multiple widely used factor strategies.

These tests showed promising results. Some of these strategies gave out-performance when back tested over longer time-frames.

However, the analysis also showed that no single factor or combination gave consistent outperformance.

Outperforming factor combinations changes over time. This corroborates with the common view amongst fund managers that relative significance of factors on equity returns change with changing market conditions.

The team therefore set out to develop a machine learning system that can predict the best factor combination for portfolio creation at any given point in time. Some interesting set of algorithms have been developed and comprehensively tested. A model that employs two proprietary ML algorithms for choosing appropriate factor strategy with monthly rebalancing have given promising results. The quant model’s stock selection and allocation capabilities have also been appreciated by the company’s Fund Management team. With SEBI approvals in place, Tata Asset Management is launching its first pure quant-based MF scheme.

Tata Quant Fund

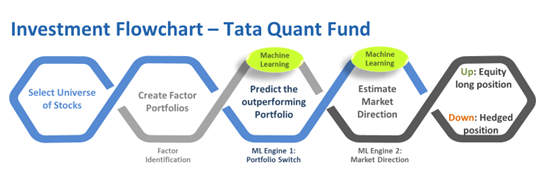

Tata quant fund is a multi-factor systematic mutual fund scheme with embedded AI modules that dynamically choose strategies basis prevailing conditions. For portfolio creation the fund will select from a fixed universe of stocks comprising of BSE 200 and those in the derivatives list.

The quant framework employs machine learning algorithms to choose a strategy from an identified list of factor strategies. The list of factor strategies has been built using popular factor models that include Value, Quality, Momentum and Size Each of these strategies employ scoring to select list of stocks and their portfolio allocation.

The framework uses 2 machine learning algorithms. The first algorithm predicts which amongst the list of factor strategies will outperform others during the next 30 days.

The second machine learning algorithm predicts the absolute direction, positive or negative return, from the factor strategies during the next 30 days.

Both the predictive models use data pertaining to (a) absolute and relative momentum of each underlying factor strategy portfolios, and (b) macroeconomic parameters pertaining both to domestic as well as international markets.

The overall investment strategy combines outputs of the two predictive models to achieve the following:

-

Consistently achieve higher returns as compared to the benchmark index

-

Avoid absolute negative returns

The overall strategy aligns to the above objective by

-

going long on selected factor strategy portfolio for the next 30 days. This is done only when the second predictive engine indicates a positive return

-

take a hedged or neutral position using derivatives when the second predictive engine indicates a negative return

The portfolio creation logic also has checks and balances in place to avoid stock selection basis very high scores only on a single factor but very low scores in others.

Machine Learning and model recalibration:

The machine learning algorithms developed for this strategy uses data starting from 2007 and uses hidden correlation and patterns for predictions. We have observed that models developed using historical data start showing drops in predictive accuracy over time. This is because relations between market parameters changes over time. In order to address this challenge, the algorithms take in incremental market data and re-calibrates and self-adjusts itself by combining new incremental data to historic data sets.

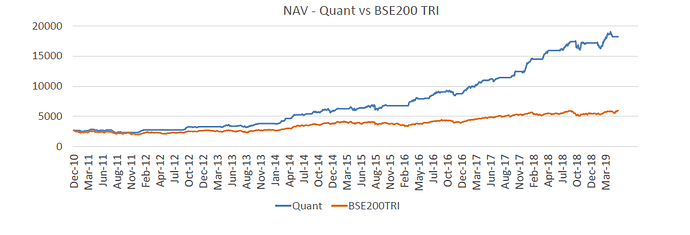

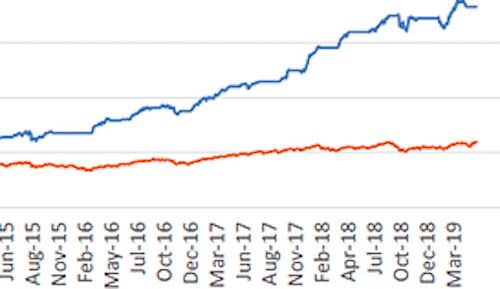

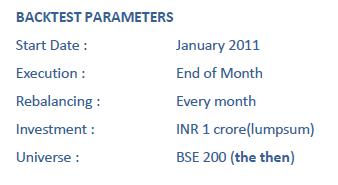

Back-testing

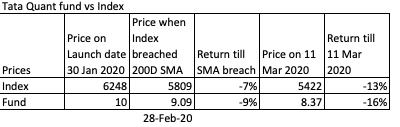

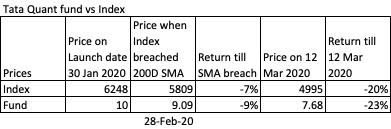

The model was back tested for 8 years and the result vis-a-vis the BSE 200 TRI is as below:

Risk Factor: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

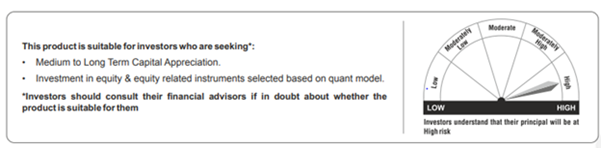

Type of Scheme: An open- ended equity scheme following quant based investing theme

Risk-o-Meter