@PK123 Valid points.

However, i still see no issues with the way EPF is structured currently,

when seen within the overall context.

Here’s the additional context i have in mind -

1. Choice exists

The usual method to go about this is to talk to one’s employer and negotiate a lower basic-pay (of which PF contributions are 12% of). Generally employers will be happy to oblige as this reduces their matching contribution as well.

2. Not the average Joe here

IMHO, not even close.

Based on how EPF contributions are typically structured,

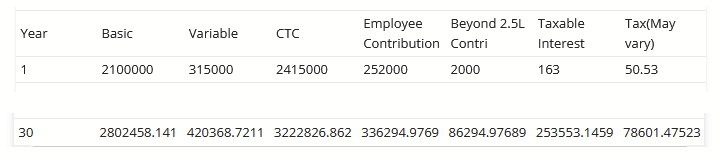

i.e. 12% of Basic-Salary, which itself is often a fraction of one’s complete salary,

to start breaching this limit, one would need to start in the top 10% (and reach top1%).

Remember that this is tax-free on redemption/withdrawal.

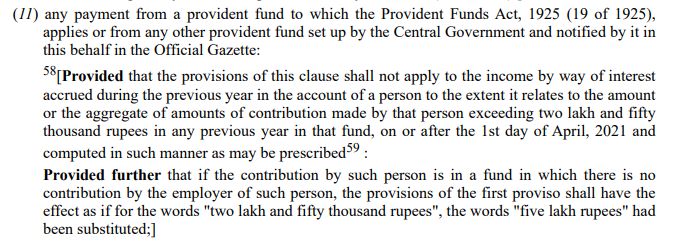

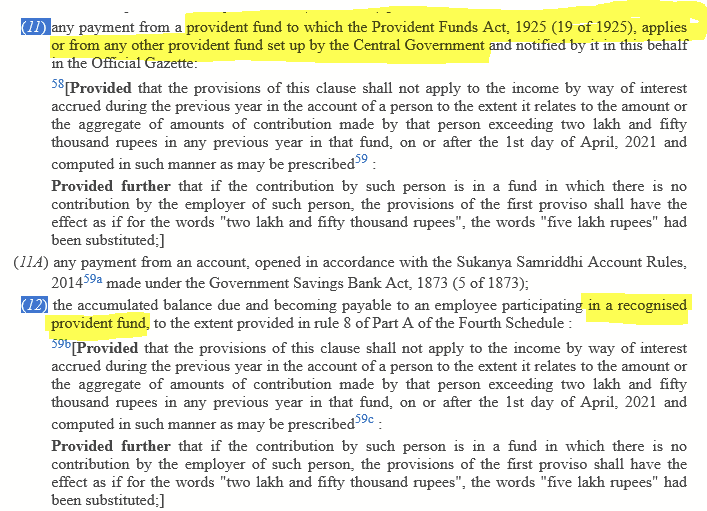

Also, remember that this will be the second risk-free return.

The first risk-free return (upto 2.5L contributed each year) providing entire tax-free investment at EPF rates.

[Source]

3. Luxury comes at price.

(a.k.a. Free lunches? sure. But, no free gourmet dinners.)

Congratulations! You are achieving a level of financial maturity that is not common.

There are no free lunches.

There are no risk-free pensions to free-load on.

There are no inflation-beating returns to be had without taking risk.

EPF enables one with a sold foundation on which to survive on.

Thrive? Well right now one is free to pursue other endeavors

- with one’s time/life

- and the majority of the capital one earns,

adopting necessary risky propositions as per one’s risk-appetite

- to fulfill any luxury one may have in mind right away

- or amass additional capital over the long-term.

3. Risk-free* returns

*as close to zero risk

The biggest point to remember is that

what EPF provides is a risk-free rate of return

very similar to sovereign govt. bonds.

Note that even sovereign govt. bonds have been providing around 7-8% returns with the interest income being taxed (unlike EPF so far). So, in that sense, any contribution to EPF above 2.5L in a year is like (not exactly, but very similar to) being guided to purchase a sovereign govt bond and pay taxes on the interest.

One aspect where EPF excels GSECs is that - contrbutions to EPF are using pre-tax income.

One can purchase GSECs using what is leftover from one’s income AFTER paying taxes.

Someone who is bothered by the lower returns of EPF contribution above 2.5L

and is really interested to invest more of their capital into riskier ventures,

can simply reduce their govt. debt securities (GSECs, TBills) investment by the same amount.

Oh, but you are NOT into GSECs/TBills at all you say.

Then maybe consider reducing the next low-risk investments you have.

Purely from a risk perspective,

here’s a handy list i like to use personally.

A list of investments in increasing order of risk

(based on personal risk assessment)

- 80C

- PF

- FD

- GSECs

- Gold

- Indian Large-cap ETF

- Indian Mid-cap/Small-cap MF

- Equity via individual stocks

- Real estate

- P2P lending

- Other speculations

What’s your list?

Now that you know that there is tax on the interest on EPF contributions > 2.5L,

How do you plan to tweak you other investments to adjust for risk/returns?