Embassy Office Parks REIT declared a dividend of Rs 4.55 per share. I own 400 shares but I received only Rs 1759 as a dividend. And I have bought another 200 shares after the dividend date. So, I own 600 shares now.

I should have received Rs 1820

Also, is there any tax on the REIT dividends? Does it get included on my tax slab?

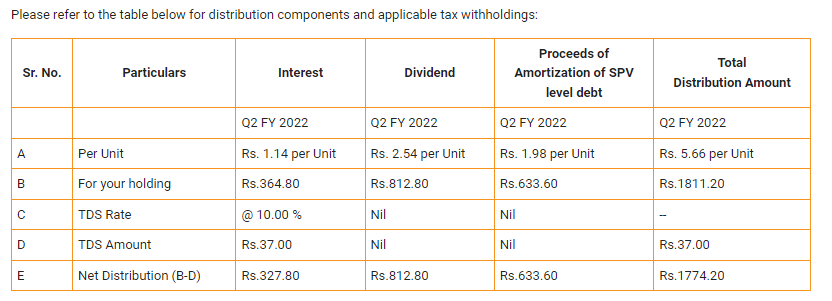

Declared distribution of Rs. 4,312.92 million / Rs. 4.55 per Unit for the quarter ended December 31, 2020. The distribution comprises Rs. 1,924.22 million / Rs. 2.03 per Unit in the form of interest, less applicable taxes, if any, Rs. 18.96 million / Rs. 0.02 per Unit in the form of dividend and Rs. 2,369.73 million/Rs. 2.50 per Unit in the form of proceeds of amortization of SPV level debt.

It appears that TDS of 7.5% was withheld on the interest portion of the dividend (of 2.03), hence interest portion dividend got reduced to 1.87775 (2.03 - 2.03 * 0.075). And due to that the total dividend per share got reduced to 4.39775 (2.5+0.02+1.87775). For 400 shares, the dividend now comes out to be 4.39775 * 400 = 1759.1

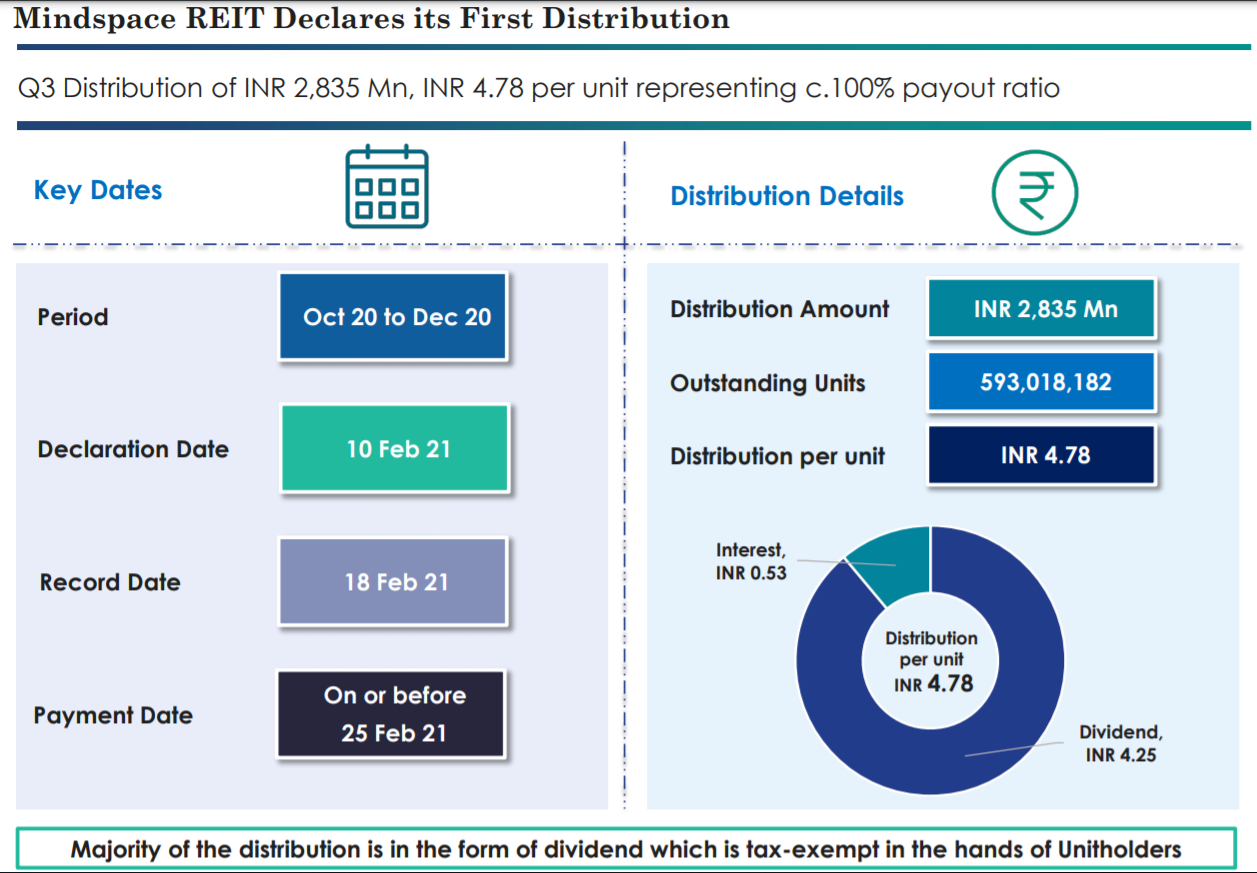

The dividend declared by them is 4.78 but I got an effective rate of 4.74 in my account, I know that Mindspace SPV is set up according to older rules where they already deduct the tax as DDT and then declared dividends so why is there this discrepancy of 0.8% there ? My brother and I both have units of this REIT and the number of units are different but effective rate comes out to be same, the only thing I can think of is some bank charges that they are deducting or is it some tax thing, can you shed some light if you have some idea ?

Thanks

As per their Investor Presentation (Page 8), it appears, similar to Embassy REITs dividend, TDS of 7.5% was withheld on the interest component of that dividend (0.53 of the 4.78), hence the interest portion dividend got reduced to 0.49025 (0.53 - 0.53 * 0.075). And due to that, the total dividend per share got reduced to 4.74025 (4.25+0.49025).

No TDS shall be deducted on distribution in the form of dividend as none of the Special Purpose Vehicles of MREIT have opted for the beneficial tax regime under section 115BAA of the Act. However, TDS shall be deducted on distribution in the form of interest as per the provisions of section 194LBA of the Act.

As per their Tax related FAQs (Page 4), an income declaration (format available on Page 7 of the same document) for non-resident Unitholders can be submitted to the following e-mail address - [email protected].

For Indian residents, Form 15G / 15H doesn’t seem to be applicable for REITs dividends. A document on Mindspace REITs website (Page 2) explains about this briefly -

Form 15G/15H

As per section 197A read with Rule 29C, Form 15G and 15H declaration is applicable interalia when tax is deductible under section 194A (Interest other than interest on securities). Since the tax is deductible under section 194LBA of the Act, Form 15G and 15H is not applicable. Unitholders are requested NOT to furnish 15G/15H in respect of any distribution by MREIT.

i. Interest income - Taxable in the hands of the Unitholders at the applicable rates.

ii. Dividend income where the SPV has not opted for the lower tax regime [under section

115BAA of the Act] – Exempt in the hands of the Unitholders.

It will be relevant to note that all EMBASSY REIT SPV’s have not opted for the beneficial

tax regime and hence all dividends received by the Unitholders from the EMBASSY REIT

will be exempt from tax in the hands of the Unitholders.

iii. Dividend income where the SPV has opted for the lower tax regime [under section 115BAA

of the Act] - Taxable in the hands of the Unitholders at the applicable rates [not applicable

for the EMBASSY REIT Unitholders].

iv. Rental income – Taxable in the hands of the Unitholders at the applicable rates.

v. Balance distributions would be exempt from tax.

So, Embassy REIT’s Interest and Dividend are only taxed at slab rate. But the “Amortization of SPV level debt” is tax-exempt? Where do I have to mention this SPV amount on the tax filling?

7. What will be the taxes deductible for different categories of investors in case the distribution is in the form of amortization of debt received by the EMBASSY REIT from the Special Purpose Vehicles?

No tax is deductible on amortisation of debt paid by the EMBASSY REIT to the Unitholders.

From what I am able to understand, the interest portion would be mentioned via the Income from Other sources section of the ITR -

But for the other two portions of the dividend - Dividend Income and Amortization of SPV level debt - those should be likely be mentioned in some kind of exempted income category of the tax filing. Maybe @San78 and @Quicko might be able to better guide you about this matter.

Income distributed by business trust to its unit holders shall be treated of the same nature. Unit-holders receiving any income distributed by trusts such as interest or dividend shall be treated as income of the unit-holder for that previous year and will be taxed as per the applicable tax rates.

It is to be noted that the FM in this budget 2021 has proposed that advance tax liability on dividend income shall arise only after the declaration/payment of dividend.

With effect from April 1, 2020, dividend received by equity shareholders became taxable. Therefore the treatment of dividend received by unitholders and equity shareholders is similar.

Erstwhile Section 10(23FD) of the Income-tax Act provided that any distributed income, received by a unitholder from the business trust, other than interest income or rental income (i.e. rental income earned directly by a REIT) would be exempt from the total income of the unitholder. The Bill had proposed that in addition to interest income and rental income, dividend income distributed by the business trust to the unitholders, would also be subject to taxation in the hands of the unitholders with effect from April 1, 2020. Accordingly, interest and dividend income distributed to unitholders were proposed to be taxed at the tax rates applicable to each of the unitholders.

The Bill also proposed that dividend income received by residents and non-resident unitholders would be subject to withholding tax at the rate of 10%. However, in case of non-residents, any lower rate as may be provided in the DTAA between India and the country of residence of the non-resident unitholder may be applicable, provided such non-resident is eligible for the benefits available in the DTAA provisions.

This tax on dividend in hands of unitholders is seen to be as a less favourable tax treatment under the new tax regime for dividend, as compared to the DDT regime. However, the Finance Act has provided some concessions. Now the amended the Income-tax Act provides that dividend distributed by a business trust shall be exempt in the hands of the unitholders, provided the SPV distributing the dividends has not exercised the option to pay corporate tax under the 22% corporate tax regime available in terms of, and subject to compliance with, Section 115BAA of the Income-tax Act. The corresponding withholding tax provisions have also been amended.

These amendments will take effect from April 1, 2020.

From what I am able to understand, certain parts of the REITs dividend (aka Dividend Income and Amortization of SPV level debt) at the unitholder level will still remain exempt from taxes as long as the SPVs don’t opt for the lower tax regime (which EMBASSY and MINDSPACE REITs haven’t opted for).