Yes, 2020 has been treacherous for most investment portfolios. And yes, external factors that were beyond your control are mainly to blame. But what if we tell you that there was something you could have done better too. Don’t fret. They say it’s okay to make mistakes as long as you learn from them. And turns out that the biggest financial lesson from the current crisis is also the simplest: always diversify your investments. Here’s why.

If you had an all-equity portfolio worth Rs 1,00,000 at the start of 2020, you’re probably down a painful 28% to 72k as of March-end, which means you’ll need a whopping 39% gain to recover from the recent carnage. And based on how unpredictable and bearish things are at the moment, you’d agree that those kinds of spectacular gains are pretty far out in the future. On the flip side, if your portfolio at the start of 2020 was divided between equities, debt, and gold in 40:40:20 ratio, the current value would stand at 92k requiring a much lesser 8.7% gain to be whole again. Pretty good, right? (here, Equity represents Sensex returns, Debt represents 10-year G-sec return, Gold represents domestic gold spot price returns as on 31st March 2020) .

So how exactly does this diversification work? Let’s take an ordinary day to day example to understand. Have you ever noticed that street vendors often sell seemingly unrelated products - such as umbrellas and sunglasses? Initially, that may seem odd. After all, when would a person buy both items at the same time? Probably never - and that’s the point. Street vendors know that when it’s raining, it’s easier to sell umbrellas but harder to sell sunglasses. And when it’s sunny, the reverse is true. By selling both items- in other words, by diversifying the product line - the vendor can reduce the risk of losing money on any given day. If that makes sense, you’ve got a great start on understanding asset allocation and diversification.

Now, unfortunately unlike the vendor who knows that monsoons always follow summers and summers always follow monsoons, investors don’t deal with predictable economic cycles. Economies go through ups and downs and these more often than not are unforeseeable. Assets in our portfolio, due to their differing risk and return characteristics, respond differently to these ups and downs, You’d agree that equities run-up when the economy is doing well; and gold tends to shine when the economy is down in the dumps

In essence, because it is difficult to predict the future of the economy, it is also difficult to determine the resulting best-performing asset class. That’s where asset allocation and diversification come handy

Asset allocation is a time-tested approach to portfolio management. It means spreading your investments among multiple asset classes such as stocks and bonds.

By including asset categories with investment returns that move up and down differently under different market conditions within a portfolio, an investor can limit significant losses. Market conditions that cause one asset category to do well often cause another asset category to have average or poor returns. By investing in more than one asset category, you’ll reduce the risk that you’ll lose money and your portfolio’s overall investment returns will have a smoother ride. If one asset category’s investment return falls, you’ll be in a position to counteract your losses in that asset category with better investment returns in another asset category. The concluding point is that diversification, whilst offering no guarantees of portfolio performance or complete protection against risk, increases the possibility of an investor’s portfolio withstanding the elements in a financial atmosphere experiencing both man-made and natural disasters on an almost daily basis.

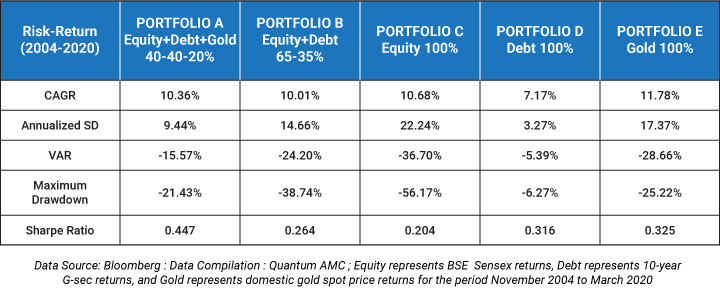

We did some number crunching to substantiate our point.

Please note that the above table is for illustrative purpose only to explain/understand the concept of Diversification / Asset Allocation”. Past performance may or may not be sustained in future.

Over the last 15 years, through the Global Financial Crisis of 2008 and the current pandemic, Portfolio A could have increased the odds of having a portion of your assets “in the right place at the right time. Not only did portfolio A with 40% equity, 40% debt, and 20% gold allocation, yield returns at par with portfolio C, a pure equity strategy, but also experienced the lowest quantum of drawdowns. Just like the vendor, portfolio A covered all bases and was prepared for any economic ups and downs. Effectively, the portfolio did not lose much money in times of crisis and also made money in the good times. Win-win