Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- The cost of Building Your Dreams, Part I

- How India’s Defence Exports Took Off

The cost of Building Your Dreams, Part I

Every morning, the Markets team sits to discuss the news cycle. One global company is almost a constant in each of these meetings: BYD. If you search them on Google now, you’re bound to come across a variety of wild headlines, all happening simultaneously.

Their Shenzhen factory caught a blazing fire. They’re in the middle of a huge controversy in Brazil for their working conditions. They just built the world’s fastest road-legal car. They’re ferociously expanding globally. Most importantly, they’re at the center of a bloody price war in their home market, China. That’s certainly a very colorful set of headlines for arguably the world’s most important automaker today.

But what’s even more bewildering is that 2 decades ago, BYD was nowhere close to being a competitive carmaker, much less being the center of all news media. If anything, Chinese consumers looked at their cars with skepticism. How did a company that often struggled to survive, eventually became the poster child for China’s industrial success?

We rarely do stories on individual companies. However, BYD’s story is as much the story of China’s economy as it is that of entrepreneurship. And understanding their history could help us inform how they got here.

We’ll be writing this story in two parts, owing to how extensive it is. This part starts from three decades ago.

A gamble on the future

In the 1990s, when China had just liberalized, mobile phones had become all the rage, which created demand for rechargeable batteries. Many entrepreneurs saw an opportunity to use China’s cheap labor to make those batteries by hand. So, they set up their own companies in Shenzhen, which was being promoted as the country’s premier business hub.

A chemistry expert named Wang Chuanfu also jumped at this opportunity, and in 1995, he set up his own firm in Shenzhen. His team would reverse-engineer batteries made by leading Japanese firms like Sony and Sanyo, and then re-assemble them using the BYD name. The approach of growing business by copying global products first was all too common in China then.

By 2003, BYD had become one of the largest rechargeable battery manufacturers in the world. Revenue had grown for nine consecutive years. The company had just listed on the Hong Kong Stock Exchange.

But then, Chuanfu did something that confused almost everyone. He bought a car company without really disclosing in the prospectus that the IPO funds raised would be used for this.

Qinchuan Automobile was a struggling state-linked manufacturer that made a very small car that nobody really wanted. It came with a small factory and a set of production licenses. BYD acquired a 77% stake in it, effectively making its entry into a brutal, capital-intensive industry that it had no expertise in.

You see, most cars back then ran on oil, where the engine, not the battery, was the focal point of every car. You had no charging points that would make EV adoption possible, either. The electrification of cars was still a very far-fetched story.

What’s more, China’s auto industry was dominated by state-owned enterprises, who often formed joint ventures with foreign automakers like Ford. And in the middle of that entered a company with no conventional supply chain relationships and no car-making capability.

Almost delusionally, though, BYD envisioned that battery technology would transform how cars are made — even when very few people in the world were seriously commercialising EVs. The belief came from Chuanfu’s expertise in battery chemistry.

Additionally, China faced three problems at the time. One, it was almost wholly dependent on imports for its oil needs. Secondly, its cities were choking on exhaust from cars and factories. And lastly, while China did have an auto industry, it wasn’t as competitive as, say, Japan, or the US. EVs seemed to offer a way out on all three fronts: energy security, environment, and industrial excellence.

That, perhaps, is why in 2001, China prioritized EVs in their State High-Tech Development Plan , under which R&D spend would be directed into certain unproven sectors.

Made in China

But BYD’s road would hardly be easy. It had to learn how to make a standard, petrol-driven car first, that too entirely from scratch.

In 2004, their first full year in the automotive industry, BYD built a new prototype. It was a completely independent design, separate from the inherited Qinchuan model. Expectations seemed to be pretty high for the battery-maker’s entry into cars.

But car dealerships did not seem to like the model. It simply wasn’t good enough in design or execution. So Wang Chuanfu himself personally smashed the prototype. The investment in the model had been quite substantial, and now all of it was sunk. But releasing it would have been worse than releasing nothing at all.

A year later, BYD launched their first commercial internal combustion vehicle, the F3.

The F3 was not a masterwork of original design. Many noticed that it suspiciously resembled the Toyota Corolla, which was one of the most popular cars in the world at the time. That wasn’t by accident, though. The F3 followed the same reverse-engineering, labor-intensive playbook as BYD’s battery business.

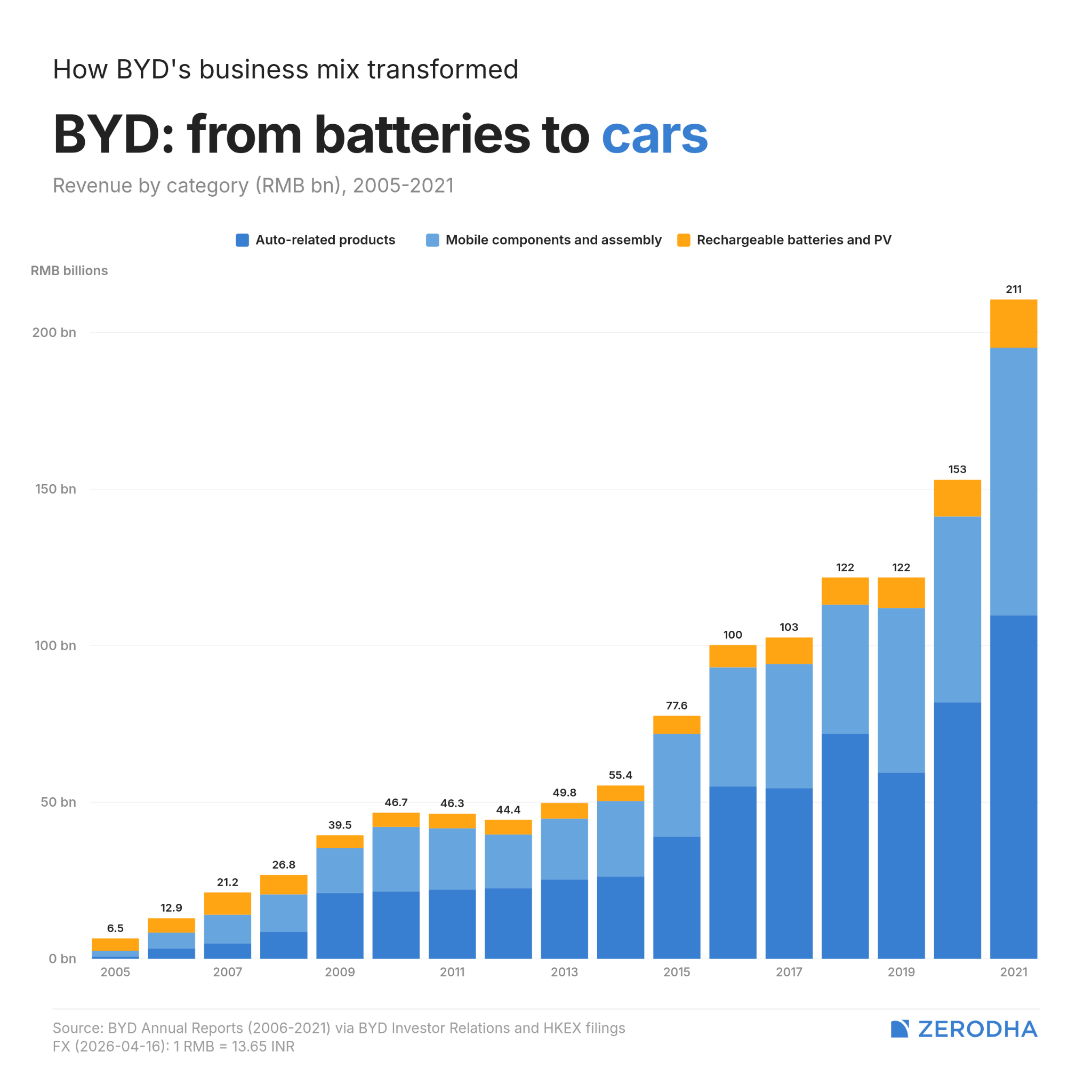

But it was affordable, reliable enough, and arrived when China’s middle class was booming. In the next year, the F3 sold over 30,000 units, becoming a runaway success. Within three years, it became China’s top-selling sedan, beating both the Volkswagen Jetta and the Toyota Corolla. Between 2005-2008, automobiles would grow from being just 5% of BYD’s total revenues to 32%, and then over half by 2009 itself.

All the cars BYD would release in that decade would follow a similar pattern. They would resemble popular models of firms like Mercedes-Benz or Toyota, and they were made by employing masses of cheap labor at the assembly line. In fact, because they were perceived to just be copycat products, car service shops would actually offer consumers to swap out the BYD logo with the logo of the original car (like Toyota).

But, however crude, BYD’s approach helped them maintain serious cost discipline and help them scale any product quickly. What they saved through this was funneled into what BYD had always aimed to do: make EVs. By 2008, BYD’s battery work had begun to be tied with its auto business as they launched their first plug-in hybrid (or PHEV), the F3DM. This car used both internal combustion as well as battery technology.

Wonderful company, fair price, great subsidies

It was also in 2008 that BYD’s success caught the eye of Warren Buffett.

Charlie Munger, the vice-chairman of Berkshire Hathaway, had been paying close attention to BYD. He was particularly enamored by Chuanfu’s tenacity to be just as technical as he was good at manufacturing at scale.

The timing looked awkward. BYD’s 2008 profits had fallen to RMB 1.02 billion (around ₹650 crore back then), down from RMB 1.61 billion the year before, as competition in the conventional car market intensified. The company was spending heavily to develop EV capabilities, and the returns were not yet visible.

But Berkshire didn’t fully see BYD as a standard internal combustion carmaker. It was sold on BYD’s battery vision. BYD’s convincing methods were, perhaps, quite unusual: in front of Berkshire executives, Wang Chuanfu drank his own battery fluid to prove that his technology was safe to use in cars.

Wang Chuanfu, Charlie Munger, and Warren Buffett

So, Berkshire made what Munger would call his most important investment at Berkshire, staking $270 million for 10% equity in BYD. A high-status international shareholder like Buffett would instantly lend BYD reputational collateral. The Berkshire name changed the way local governments, banks, and suppliers thought about the company. And it gave BYD more runway to spend on R&D related to EVs.

But the biggest tailwind in BYD sails would come just a year later.

In 2009, Beijing launched the “Ten Cities, Thousand Vehicles “ programme. Basically, across China’s largest cities, the program provided subsidies for EV adoption in fleets of public buses and taxis. This program would be monitored by the local governments of those cities or provinces. And in China, local governments play a massive role in pushing economic growth — they’re given growth targets to chase by the centre. So, they’re often involved in providing funding to firms.

This was China’s first large-scale industrial policy dedicated solely to electric vehicles. And while this wasn’t a consumer subsidy, it was still a huge sign of the support that EVs would eventually receive.

Fleeting moments of success

The “Ten Cities ” policy was one of the fundamental causes of BYD’s first taste of success in commercial EVs.

See, BYD’s path to EV credibility ran through bus depots and taxi ranks, not showrooms. In that vein, it launched two products: the e6 electric saloon designed for the taxi market, and the K9 electric bus designed for city transit. Both of them were pure EVs , not hybrids.

By the end of 2011, BYD reported around 300 e6 taxis operating in Shenzhen alone. The K9 had begun operations in Shenzhen and Changsha simultaneously, with 200 units being bought in 2011. That same year, at a sporting event in Shenzhen, BYD supplied 200 K9s and 250 e6 taxis to ferry athletes around the city.

BYD also received plenty of local government support during this period. Shenzhen alone had provided RMB 864 million (around ₹530 crore back then) in automotive R&D grants in 2008, with Changsha and Huizhou adding further tranches. The local governments were effectively functioning as buyers of BYD’s buses and co-investors.

BYD’s progress soon spilled over to the consumer market. In 2013, BYD released the Qin, another plug-in hybrid EV. And it topped China’s new electric vehicle (or NEV) sales. By 2015, sales of new energy vehicles, which included battery vehicles and PHEVs, had surged 208% year on year to 58,000 units, and BYD was claiming the top position in global NEV sales.

Around the same time, the industrial policy tailwinds had begun even stronger. In 2012, China released the NEV Development Plan , which targeted cumulative sales of 5 million pure-play and hybrid EVs by 2020. And from 2015 onwards, the central government launched a new subsidy policy targeted at leading EV players in China, meant to be phased out gradually. This bolstered China’s global market share in EVs to over 50% by 2015.

![]()

When the tap runs dry

But, this dream run would come to an existential standstill in a few years due to a shift in policy priorities.

See, China’s NEV subsidy regime had created an unintended effect. The combination of generous central payments and weak verification had produced an ecosystem of fraud. When the Ministry of Finance audited major NEV producers, inspectors found worrying patterns. Vehicles were registered to claim subsidies but never actually sold, and companies optimised for eligibility criteria rather than for product quality. Beijing was spending on cars that, in many cases, existed only on paper.

So, in 2019, the subsidy regime itself was suddenly overhauled not just in scale, but in design. Beyond subsidies being cut, technical thresholds like minimum battery energy density, battery range, and maximum energy consumption rose sharply, primarily to ensure higher product quality. Additionally, China also started to allow the entry of foreign competitors like Tesla, which would force domestic players to be on their toes.

All of this hurt BYD significantly. The new technical thresholds favored pure-play EVs over plug-in hybrids. Compared to competitors, BYD’s portfolio and R&D expenditure were much more geared towards the latter than the former. PHEVs were more complex and costlier to produce — which made them especially dependent on subsidies to remain competitive. In fact, in 2019, BYD’s own pure EVs grew in sales while plug-in hybrid sales fell.

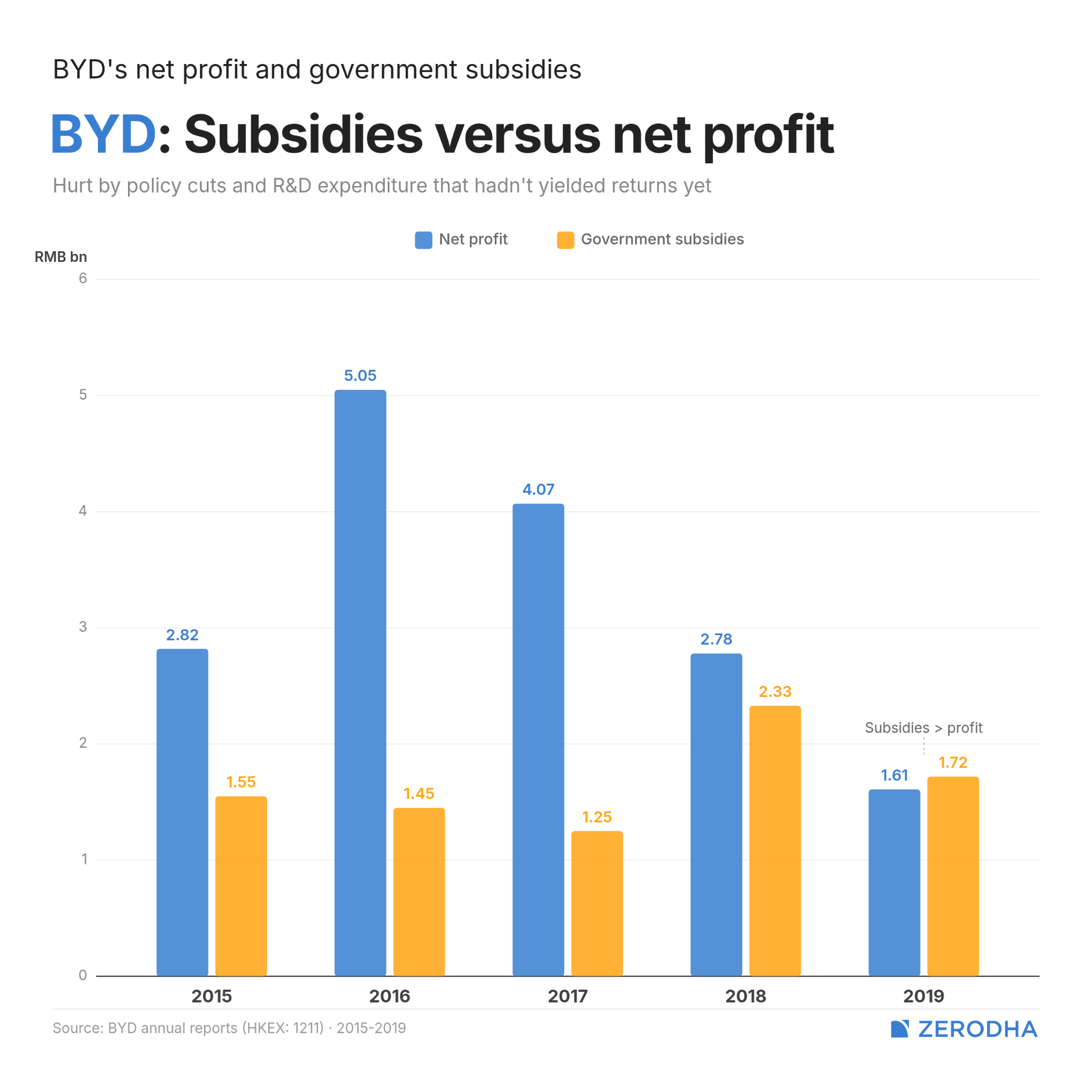

Much of its profits in those years were made up by government subsidies. For instance, in 2018, BYD made a net profit of RMB 2.78 billion (~₹2,800 crore), of which 83% was government grants. The companies that had survived China’s EV decade purely on subsidy capture did not make it through this transition.

Between 2017-2019, BYD’s profits tumbled consecutively, and the decline was mainly attributable to subsidy cuts, a slowing auto market, and its product mix. It was, in Wang Chuanfu’s words, BYD’s “darkest hour”.

But, as they say, the night is only darkest before dawn. And BYD’s biggest breakthroughs were yet to come. That, we’ll cover in Part II.

How India’s Defence Exports Took Off

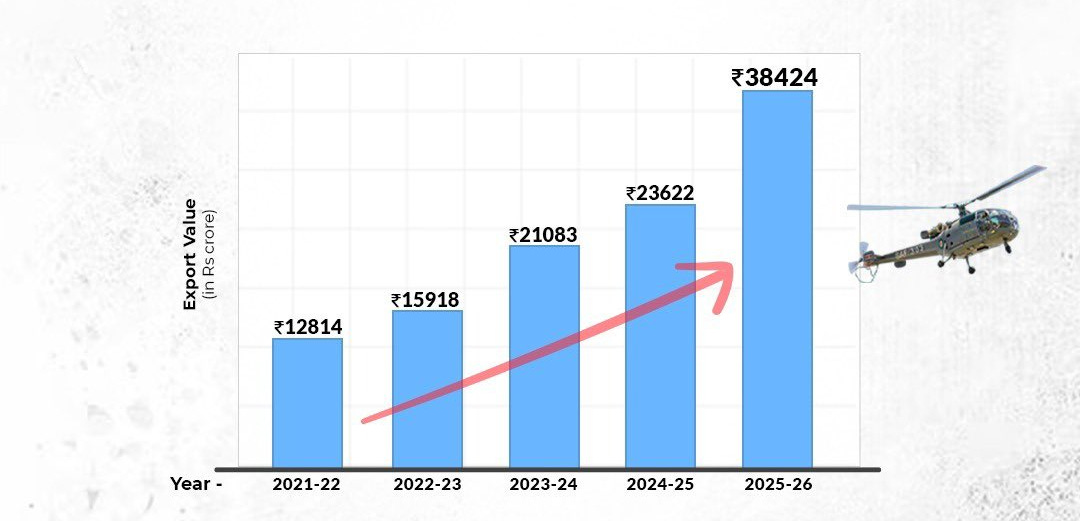

Earlier this month, India’s defence exports had hit a record ₹38,424 crore in FY26, up 62.66 percent from the previous year. A few days later, ahead of Q4 FY26 results, brokerage previews said listed defence names had a strong order books and a healthy pipeline.

That is a striking place for India to be. Ten years ago, defence was not really a private-market story in the way it is now. India still had a large defence establishment, of course, but the domestic industrial ecosystem was narrow, state-heavy, and deeply dependent on imports in many important categories.

Even now, it would be wrong to pretend the dependence has vanished. MP-IDSA noted last year, drawing on SIPRI data, that India was still the world’s largest arms importer in 2019 to 2023, with ~9.8% of global imports. The shift, while real, is still not complete.

Still, something important has changed. Data shows defence production has risen from ₹46,429 crore in 2014-15 to ₹1.50 lakh crore in 2024-25. In FY25 alone, the Ministry of Defence signed 193 contracts worth ₹2.09 lakh crore, of which ₹1.69 lakh crore went to domestic industry.

Image sourced from Twitter handle of Rajnath Singh, Defence Minister of India.

How did a country that spent years worrying about basic defence shortages reach a point where exports keep hitting records and private companies are part of the market conversation?

To answer that, you have to go back to a less flattering starting point.

The weakness underneath

In July 2017, a CAG report on the Army and ordnance factories laid out how thin India’s ammunition reserves really were. At the time, 55% of ammunition types were below the Minimum Acceptable Risk Level (MARL), and 40% were at a critical level with less than ten days of stocks. The same reporting said the Army was meant to plan around forty days of war reserve in case at any point the country gets into an armed conflict. This is called the War Wastage reserve .

You see, ammunition is not like a tank or a radar. It is a consumable. If a war turns intense, shells, rockets, tank rounds and propellants are burned through very quickly. That is why militaries keep reserve benchmarks in the first place. MARL is the floor, while the wastage reserve is the cushion. If you are below both, you end up sitting empty handed as enemies come knocking.

A shortage like that does not appear overnight, though. It happened because of the supply chain underneath which had been weak for a long time.

For most of independent India’s history, there was only one domestic source of ammunition: the Ordnance Factory Board (or OFB), a large state-run network of factories inherited from the British era. The OFB had a monopoly, and private firms were effectively shut out of ammunition production.

The CAG found repeated shortfalls across a large share of the ammunition types the OFB was supposed to supply. In some cases, the system had even lowered its own targets and still failed to meet them. The auditor had been raising alarms since 2015, but very little had changed.

The second source of ammunition was imports, mainly from Russia. But that came with its own trap. India’s deals with Russia were supposed to include technology transfer so that we could learn to make the ammunition at home. But the deals seemed to have only marginally improved production capability. The technology transfer did not hand over the deepest design know-how, or critical sub-systems.

This was the defense and ammunition procurement model India had built for itself over decades: a weak domestic monopoly, an unreliable external supplier, and a forty-day reserve requirement it was meeting for barely half its weapons.

Geopolitical arithmetic

However, things changed with Russia’s invasion of Ukraine in 2022.

Ukraine’s pre-war stockpiles, built partly on Soviet-era reserves, were depleted much faster than expected. NATO countries began drawing down their own inventories to resupply Kiev.

By late 2023, the chair of the NATO Military Committee said that “the bottom of the barrel is now visible. ” The US, which had been producing ~14,000 155mm artillery shells a month before the war, suddenly had to think in multiples of that. Europe discovered that years of lower defence spending had also eroded its manufacturing base.

The lesson was simple. Modern war consumes ammunition at a pace that peacetime systems are rarely built for. A country can have good weapons, capable soldiers and sound strategy. But if it runs out of shells, all of that starts to matter less.

For India, this was uncomfortable in a very specific way. Its defence planning has long assumed the possibility of a two-front conflict with China on one end and Pakistan on the other. That is the kind of scenario that demands deep ammunition reserves. By the Army’s own auditor’s account, India did not have them. In some of its most important categories, stocks would not have lasted even ten days.

The state changes the system

In October 2021, even before the Ukraine war, the government broke up the Ordnance Factory Board into seven separate corporate entities. The ammunition business went into a new company, Munitions India Limited, or MIL. The logic was that a corporate structure would create more accountability than an old bureaucracy had. MIL would now have a balance sheet, a management team, and performance targets it could not quietly revise.

But the more important shift was outside the old state system. The private sector was finally brought in properly.

That mattered because ammunition is not an industry companies enter lightly. It needs capital, land, compliance, safety systems, specialist chemistry, and confidence that demand will continue for years. No private company will spend hundreds of crores building a plant if it has no idea whether the Army will place another order next year.

So the government changed the economics. It began issuing longer-term supply contracts to private firms. They could now build capacity knowing demand would not vanish after one procurement cycle.

By the end of 2024, the government said the Indian Army’s ammunition procurement by Indian industry for a ten-year requirement was in progress to establish at least one indigenous source for all types of ammunition, and that 154 out of 175 ammunition variants had already been indigenised. The arms and ammunition sector was also being opened up further for private industry, with easier licensing and capacity-expansion rules.

The Indian Army’s ammunition budget is around ₹ 20,000 crore a year. Until a few years ago, 35%-40% of that was still being spent on imports. By 2024, that share had fallen below 10%. Over a three-year period, the Army placed ammunition supply orders worth nearly ₹ 26,000 crore on domestic manufacturers.

Capacity changed the economics

Once a country builds serious ammunition capacity for security reasons, a new question appears. What happens to that capacity in peacetime? A plant built to improve wartime resilience does not stop needing orders when there is no war. The lines still need to run, workers still need to be retained, and fixed costs still need to be absorbed.

That excess capacity can now find a useful avenue in exports. That is how the US has long handled parts of its own defence industrial base. Export demand helps sustain capacity between moments of crisis. India seems to have arrived at the same logic, but from the other direction. It seems that we built capacity not because we wanted to be export-ready, but out of fear.

MIL, now operating at greater scale, began receiving large export orders for artillery shells. Indian-made ammunition started reaching European buyers. As per Reuters, Indian-made shells were reaching Ukraine through European intermediaries, including Italian and Czech companies. India did not sell directly to Ukraine, and said it was monitoring the matter, but it also did not officially announce a move to shut the trade down.

Estonia’s defence minister also spoke publicly about Indian companies setting up ammunition manufacturing lines in his country. Indian firms building shell capacity inside a NATO member state was likely not even a plausible conversation before the breakup of the OFB.

That is a much bigger shift than a headline export number might suggest. It means India is not just buying less from abroad in some categories. It is starting to matter as a supplier in a market that has become tight, urgent and global.

Why markets care now

The export record from earlier this month is one reason defence is back in focus ahead of Q4 FY26 results. The bigger point is that the sector now has the things markets care about in this stage of a story. It has large order books, a visible procurement pipeline, and a state that is still directing serious capital toward domestic suppliers.

For instance, in February 2025, Solar Industries disclosed a ₹6,084 crore Ministry of Defence order for Pinaka rockets. By its most recent earnings call, the company said its defence order book had reached about ₹18,000 crore and that quarterly defence revenue had crossed ₹700 crore. On its FY25 results call, it had guided for ~₹3,000 crore of defence revenue in FY26.

Bharat Forge works on the weapons-platform side of the same rearmament cycle. In March 2025, the Ministry of Defence signed contracts worth about ₹6,900 crore for the Advanced Towed Artillery Gun System, or ATAGS, and its towing vehicles, with Bharat Forge as one of the key suppliers. A few months later, the company also figured in the ₹2,770 crore contract for more than 4.25 lakh close-quarter battle carbines for the Army and Navy. This shift in India’s defence sector is also driving ammunition indigenisation, there is demand for the guns, vehicles and infantry systems that sit around it.

The industrial story is broader than the listed one. A meaningful share of India’s ammunition capacity still sits with public-sector and unlisted players, which means the market offers a window into the theme, but not the whole picture.

So what is next?

None of this means the story should be romanticised. India still imports a lot of defence equipment. Procurement in defence remains state-led and can be lumpy. Export flows can be politically sensitive. And strong order books do not automatically translate into clean execution.

But the broad change is hard to miss. A decade ago, ammunition was mostly a readiness problem and an institutional embarrassment for India. Today, it is also an industrial category. It has policy support, private capacity, export relevance, and listed companies with enough exposure for markets to care. The next phase will depend on whether India can move beyond licensed production and import substitution into deeper design control, stronger technology ownership, and repeatable export capability.

Tidbits

-

Wipro announces Rs 15,000 crore share buyback offer at 19% premium.

IT services giant Wipro announced a significant Rs 15,000 crore share buyback at Rs 250 per share, a 19% premium over the last closing price. This marks the company’s first buyback in over three years, involving up to 60 crore shares, representing 5.7% of its paid-up capital. Promoters have indicated their intention to participate in the tender route buyback.

Source: Economic Times -

India’s Wholesale inflation rose to a 38-month high of 3.88 percent in March, up from 2.13 percent in the previous month, driven by a surge in crude and energy prices as well as firmer manufactured products, government data released on April 15 shows.

Source: Moneycontrol -

India’s agriculture sector may face a challenging year ahead amid concerns over weak monsoon, possible El Nino conditions, and fertilizer supply risks linked to the West Asia conflict, according to a report by ICRA.

Source: HinduBusinessLine

- This edition of the newsletter was written by Manie and Aakanksha.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by Zerodha{kind=link}

Deepak Shenoy on what’s happening with the rupee

Over the past few weeks, the rupee has been moving in ways that aren’t easy to explain. While higher oil prices and rising dollar demand tell part of the story, there’s a more technical layer beneath it. We spoke to Deepak Shenoy to break it down—especially the role of the offshore NDF market. It’s a conversation about arbitrage, RBI intervention, and why the rupee has been so erratic lately. More importantly, it raises a bigger question: are these fixes solving anything at all?

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()